(GCM26) (GLD) (SIK26) (SLV) (ZSK26) (SOYB) (KCK26) (CCK26) (SBK26) (CANE) (CLK26) (UNG) (USO) (BNO) (DBO)

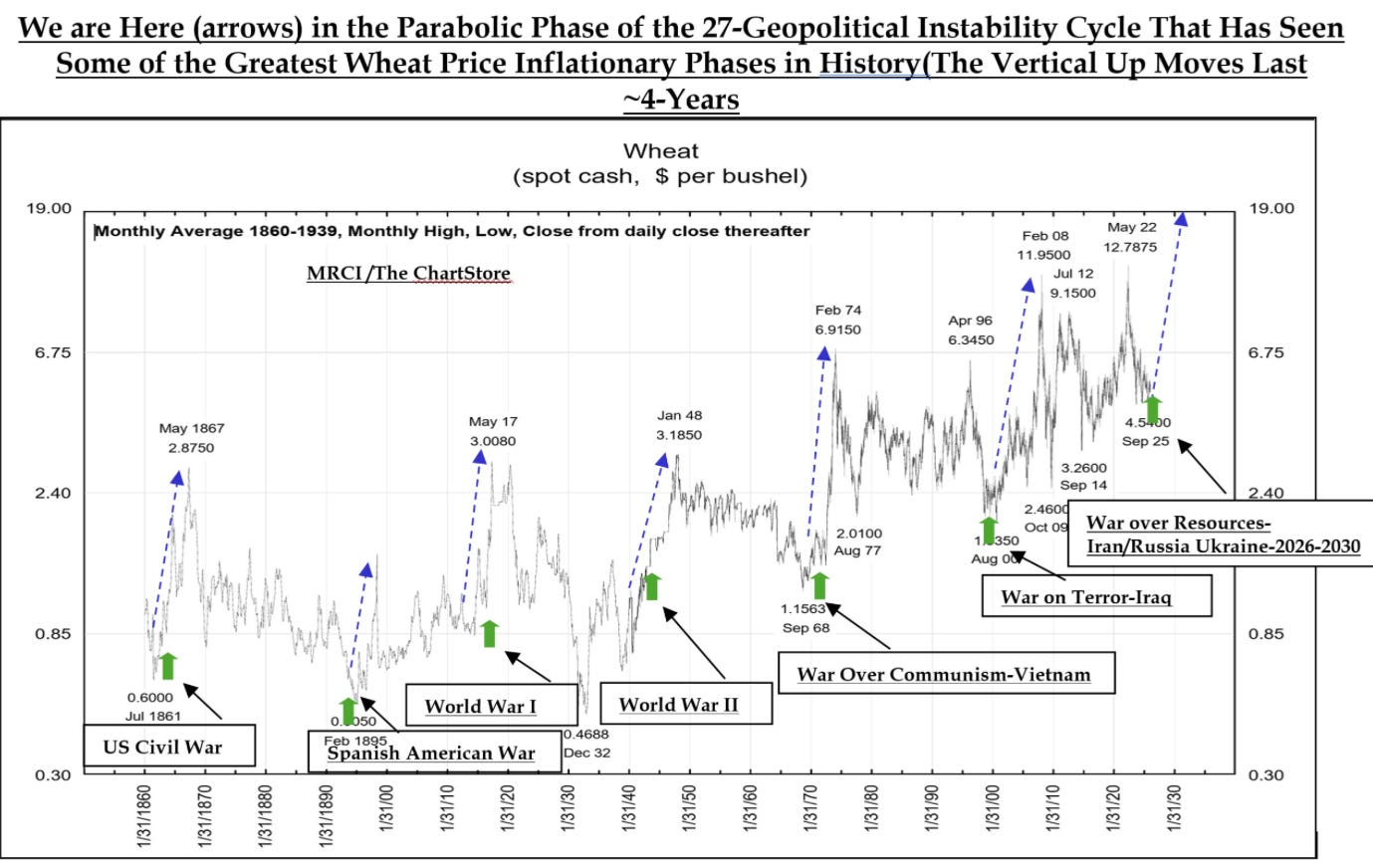

“War is now a Commodity with an Uncertain Future”

Tighten Your Seatbelts: It's Going to be a Bumpy Ride

March 11, 2026

by Jim Roemer - Meteorologist - Commodity Trading Advisor - Principal, Best Weather Inc. - Co-Founder, Climate Predict LLC - Publisher, Weather Wealth Newsletter

Scott Mathews, Editor-in-Chief

First, let’s “mellow out” for a moment … Please watch the Video (link below the pictures)

I want to start off with a song. Those of you who have been around for long enough to remember the Vietnam war (or remember hearing your parents talk about it), know that today’s war definitely takes us down an ominous path.

Here is an image association test: What does this AI-generated image mean to you?

Would you like to know more?

That image conjures up a line from Woodstock (Joni Mitchell’s 1969 tune, written for Crosby, Stills & Nash (Neil Young had not yet joined the group): “I dreamed I saw the bombers riding shotgun in the sky, turn into butterflies above our nation.”

Here is a YouTube video of Joni singing this number in 1970: https://youtu.be/3aOGnVKWbwc

The following narrative is our story about the war of today, and how it impacts our commodity markets.

Commodity ETFs: How the worsening Middle East War is causing surging grain & energy prices

Mid-late week, I will have a report with a Weather Spider summary. However, due to time constraints and the ongoing war in the Middle East, I may or may not have my global wheat study next weekend before I go on vacation. Otherwise, I will have it by late March, for sure.

In This Report:

A Beautiful Song: peace, ending war & getting back to who we are (The Garden)

Summary of markets affected by the war and some weather

Energy Market ETFs

Metals ETFs

Grain and Soft Commodity ETFs

Introduction:

I will quickly get to the point: I do not like advising in markets when trading is all GEOPOLITICAL and when weather is mostly taking a back seat. Look for the stock market to collapse, at least for now.

However, again, shorting coffee on rallies probably remains my highest confidence trade. If the drought remains in the Plains, buying wheat. However, probably NOT on this rally if you did not see my reports last week (I became bullish again) before the price explosion. There may be a sell in natural gas at some point, otherwise, I would leave it alone. A bit late to buy soybeans or corn now until we get into the spring and summer weather markets. I have no idea about cocoa and sugar(too many factors). But first…Here is something interesting about cocoa:

Rotting Cocoa Beans Force West African Farmers to Change Vocations

Image Source: “Photo” rendered by Scott Mathews, via Perplexity AI

Cocoa Situation in West Africa

A sharp crash in cocoa prices after last year’s record highs is devastating small farmers in Ghana and Ivory Coast, pushing some to abandon cocoa for illegal gold and sand mining while governments cut farmgate prices to move unsold, rotting beans. After cocoa futures spiked above about 12,000 dollars per metric ton in 2024, prices collapsed to roughly 4,000 dollars as supply caught up, leaving traders unwilling to buy West African beans without taking heavy losses. Because Ghana and Ivory Coast set fixed prices for farmers each season, state buyers accumulated large stocks of cocoa they could not resell profitably, so beans have been left decaying in warehouses and many farmers have waited months for payment.

Impact on farmers

Many farmers report that their harvests have declined over time, partly from climate change, plant disease, and erratic rainfall, which had already squeezed incomes even before the price crash. A typical smallholder now sees cocoa land as more of a burden than an asset, explaining that after years of poor yields and price shocks, staying in cocoa no longer seems like a viable path out of poverty for their family.

Shift to mining and other uses

Some farmers are leasing parts of their farms to illegal gold or sand miners, attracted by quick cash but leaving land degraded or unusable for future agriculture. Farmer representatives say many do not want to support illegal activities but feel compelled to feed their families, and some growers even obtain mining licenses to reduce the risk of legal trouble.

Government responses

Ghana has cut its fixed cocoa price by about 28 percent, to just under 3,900 dollars per metric ton, to make beans cheaper for buyers; Ivory Coast has also slashed what it pays farmers by more than half for the 2026 season. Farmers argue these cuts leave almost no profit once production costs are included, with some fearing that accepting the new prices will force them to pull children out of school or give up on long-term plans.

Broader stakes

Cocoa exports provide around 40 percent of total export earnings for Ivory Coast and nearly 15 percent for Ghana, so the crash threatens national revenues as well as rural livelihoods. While producers in South America and Asia are expanding output, West Africa still dominates global supply, and the crisis is prompting questions about whether younger generations will continue cocoa farming at all.

AND NOW…BACK to our “WAR STORY”

Last Thursday, before the explosion in crude oil prices, wheat, and a bit in soybeans, I specifically mentioned my more bullish attitude.

Hence, read between the lines if you want to trade this stuff. Crude oil bull spreads have soared, wheat rocketed on a combination of the war and some new weather problems in the U.S. Plains and India. The South American soybean crop is coming down a bit from weather concerns in recent weeks, while soaring crude oil prices have helped the soybean oil market.

This report today discusses which ETFs have rallied on the war. A bit late now to get in? Patience is key as we head into the Northern Hemisphere’s growing season for many agricultural commodities.

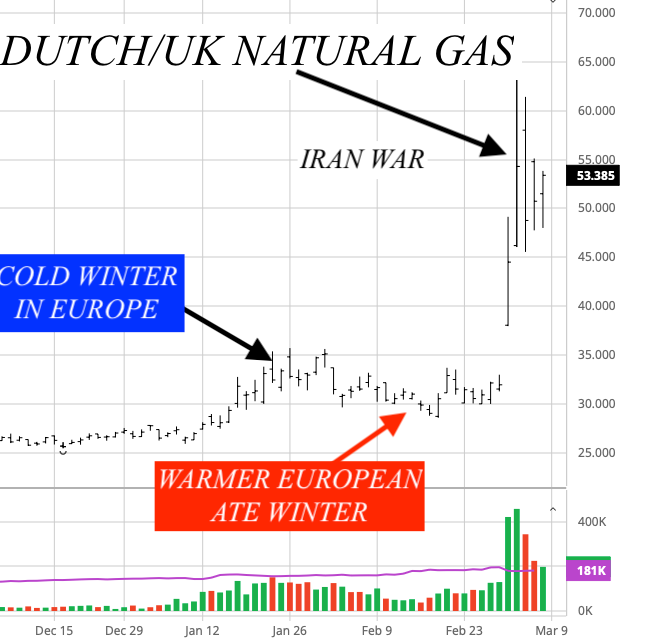

As far as natural gas prices are concerned, we soared mainly due to the European markets. While I see one big cold snap for the Midwest and East in about 8-10 days, it will likely not last. This may (?) set up a selling opportunity in natural gas on further price rallies. Otherwise, as I said a few weeks ago: “leave it alone.”

Chart Source: barchart.com Added comments by BestWeather Inc.

Correction -("Ate Winter" should read “Late Winter” SM, editor)

I will have an update mid-late week regarding some more trading ideas and my Weather Spider summary. Then, next weekend, before I go on vacation, skiing, I will present a spring weather forecast for the wheat market.

Summary of markets affected by the war and some weather

(this section was written Sunday before markets opened)

Crude oil spreads (April vs September-October) should continue to soar. I mentioned this last Thursday and crude has rallied more than $18 and the spread more than $10. Crude oil could top a $100 a barrel. Too late to buy on such a rally and of course, no weather. This market could come crashing down if there are any changes in the war.

Gasoline prices will continue to rally

Natural gas could rally due to tightness in global LNG supplies due to the war and a possible big eastern U.S. cold wave this weekend and possibly snow next week. However, though a week of colder weather is likely in the Midwest and East, the next two EIAs may be bearish due to recent warm weather. I have mentioned not trading natural gas during the last few weeks, due to very volatile U.S. weather, and now the war.

Wheat prices could continue to rally. Here too, last Thursday I mentioned a more bullish outlook. If drought expands in the Plains in April and May, wheat could rally more than $1 more.

Soybean prices could rally further due to higher crude oil prices that are causing inflation fears, biodiesel demand. In addition, there continues to be a couple crop issues in South America.

Sugar has rallied a bit due to higher crude oil prices, plus a lower crop in India. A global surplus is bearish, however… (mixed signals).

Last week, coffee prices rallied as the market was oversold. We already had a huge break on improved weather for Vietnam and Brazil, which I forecasted months ago. Worries about tight nearby supplies (prior to Brazil’s harvest) and logistical issues of exporting Robusta coffee out of Asia (due to the war) have helped prices. I remain bearish longer-term on further rallies with high confidence, later.

Energy Market ETFs

United States Oil Fund (USO) – tracks front‑month WTI; up over 6–12% on the Middle East supply shock as traders price in Strait of Hormuz disruption risk. This market will continue to soar, but any chance in war talk or easing of sanctions against Russia, etc. would result in a major price correction south.

United States Brent Oil Fund (BNO) – tracks Brent; up more than 7–9% in response to the jump in seaborne crude prices tied to the war premium on exports out of the Gulf.

Invesco DB Oil Fund (DBO) – futures‑based crude basket that has jumped around 4–5% on the U.S.–Israel strikes on Iran and subsequent escalation, reflecting the tighter crude balance.

Natural Gas (UNG)–-Soared due to LNG production being shut down in parts of Europe, which caused a supply squeeze. Qatar, the top LNG exporter, suspended shipments amid attacks near facilities, stranding cargoes and forcing Europe/Asia to bid up spot prices from U.S./Australian alternatives. If this had been the beginning of winter (not the end), there would have been even a bigger bullish reaction.

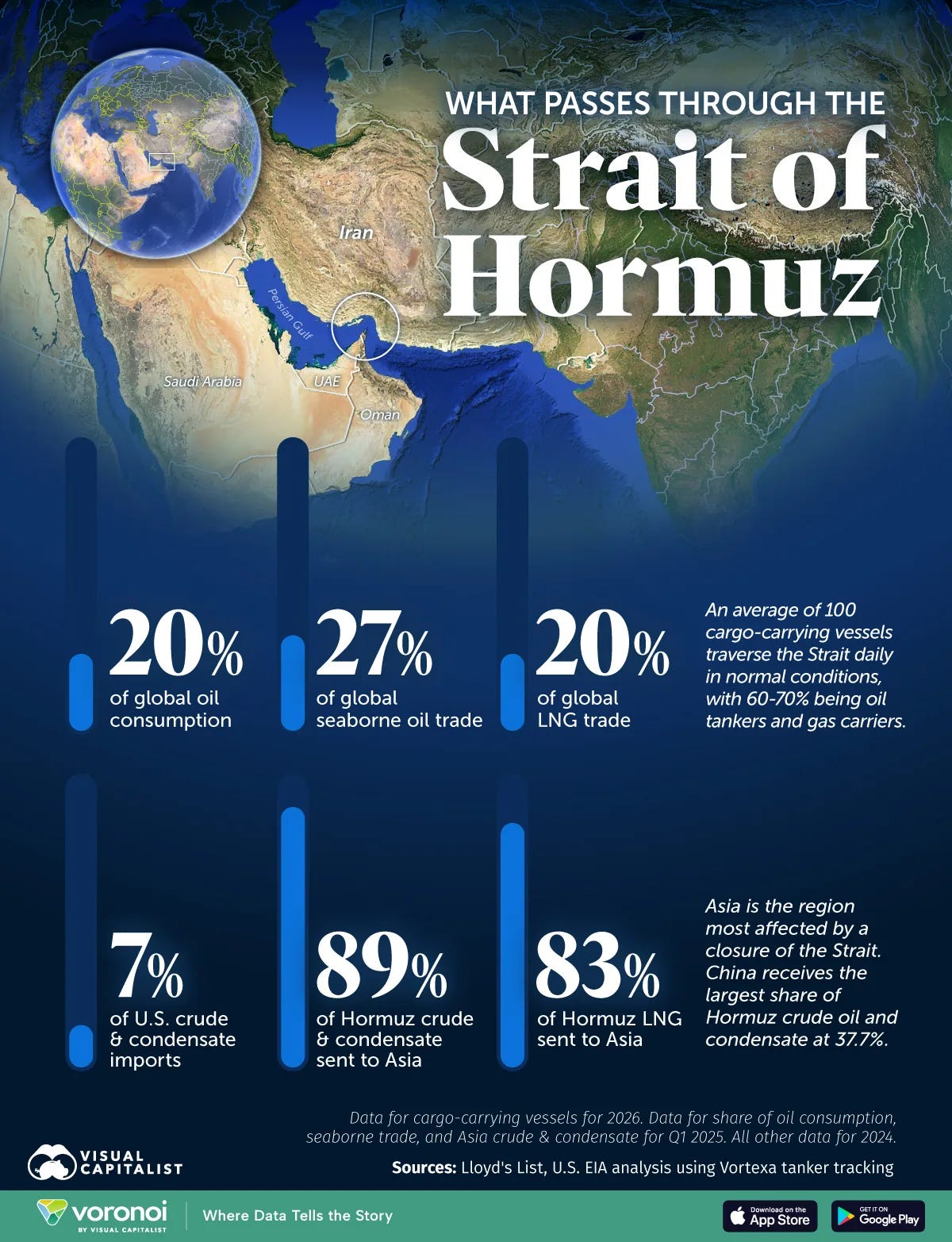

The Strait of Hormuz, which normally carries roughly a fifth of the world’s crude and gas flows, was effectively shut or severely restricted as the conflict escalated, stranding tankers and cutting export routes from Gulf producers.

Image by Our Friends at Visual Capitalist

Qatar and other Gulf exporters are key suppliers of liquefied natural gas, so missile and drone attacks near gas facilities and shipping lanes immediately boosted global gas benchmarks, especially in Europe and Asia.

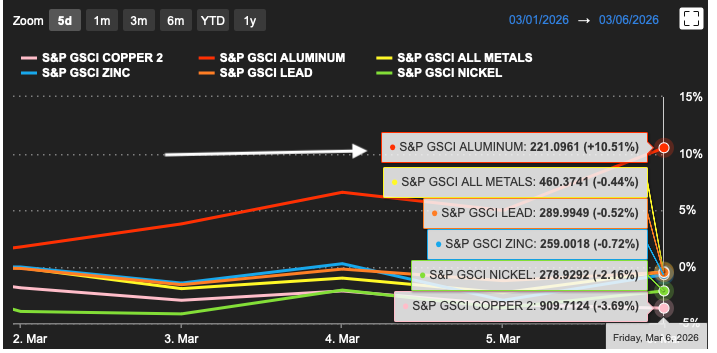

Metals ETFs

Chart Source: marketscreener.com

With respect to metals, while gold (GLD) is normally a safe haven during times of war, we have already had a massive rally in both gold and silver (SLV) prices over the last year. Following my big bullish trade in silver last year, the war could actually be bearish on worries over slowing industrial production. In actuality… it is NOT really a safe haven anymore (for now).

Worries about industrial production being slowed hit base metals such as copper, and those that trade on the LME, last week. On the other hand, aluminum (ALUM) prices surged during the Iran war due to direct supply disruptions in the Middle East, where the Strait of Hormuz serves as a critical shipping chokepoint for the metal.

Middle East smelters faced gas shortages and raw material import delays via the same route, with Aluminum Bahrain halting sales and others warning of output cuts. This exposed the West’s vulnerability to the region, which supplies a significant share of globally traded aluminum.

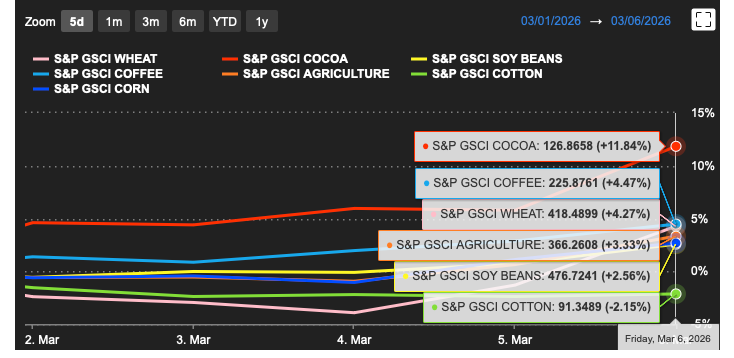

Grain and Soft Commodity ETFs

Wheat and soybeans, which had already been rallying, pushed to new short‑term highs in the first week of March, as funds added long positions tied to the broader commodity and inflation trade.

Chart Source: marketscreener.com

Wheat ETF (WEAT)

The Teucrium Wheat Fund (WEAT) is up roughly mid‑single to high‑single digits over the past week as front‑month wheat futures spiked to fresh short‑term highs in the first week of March.

Notice the chart I sent out early Friday morning about war and wheat prices. This, combined with hot weather in India and a developing drought in the Southern Plains, helped prices go nuts late last week.

Source: Hackett Financial Advisors (used by permission)

Soybean ETF (SOYB)

The Teucrium Soybean Fund (SOYB) rallied about 3% last week. Soybean prices rallied during the Iran war due to higher energy costs boosting soybean oil demand, fertilizer price spikes threatening planting margins, and a broader commodity risk premium from Strait of Hormuz disruptions. In addition, Soybean oil futures surged alongside crude, as refiners eyed vegetable oils for biofuel blending amid pricier petroleum.

Also, as per my comments two weeks ago, I raised my concerns regarding wet weather in Mato Grosso affecting the end of Brazil’s soybean harvest and it being too dry in the south. Not a disaster, but the South American soybean crop will come in at least 3-4 MMT lower than earlier USDA estimates.

The Gulf region and the Strait of Hormuz are key hubs for nitrogen/ammonia fertilizer, so the conflict quickly pushed nitrogen prices higher at U.S. import points like New Orleans.

The rallies in cocoa, sugar, and coffee are only knee-jerk reactions to higher crude prices and inflation fears. Selling coffee on rallies or remaining short July coffee calls is still one of my highest confidence trades.

Please Feel Free to Request a 2-Week Free Trial to WeatherWealth by Clicking Here

OR… To Read Some FREE Reports, Subscribe To WeatherWealth Lite On Substack Via This Link

Remember, when trading commodities, always apply risk management, such as stop-loss orders and position sizing, and consider using spreads to isolate the seasonal component of a particular market move.

Mr. Roemer owns Best Weather Inc., offering weather-related blogs for commodity traders and farmers. He is also a co-founder of Climate Predict, a detailed long-range global weather forecast tool. As one of the first meteorologists to become an NFA-registered Commodity Trading Advisor, he has worked with major hedge funds, Midwest farmers, and individual traders for over 35 years. With a special emphasis on interpreting market psychology, coupled with his short and long-term trend forecasting in grains, softs, and the energy markets, he commands a unique standing among advisors in the commodity risk management industry.

/Boston%20Scientific%20Corp_%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock.jpg)