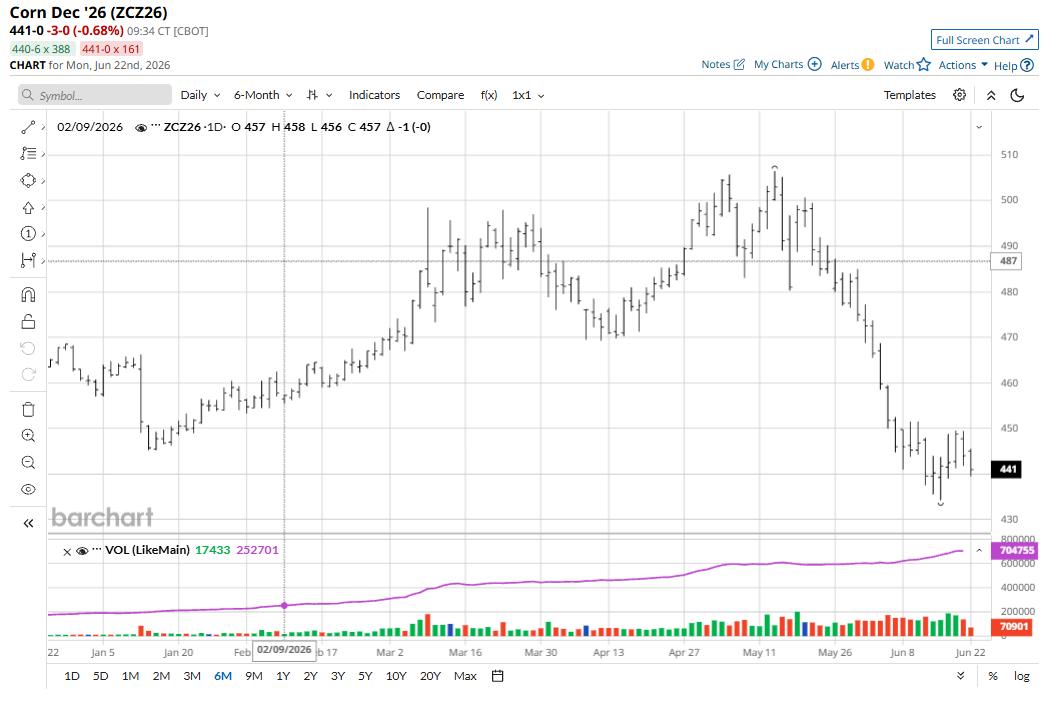

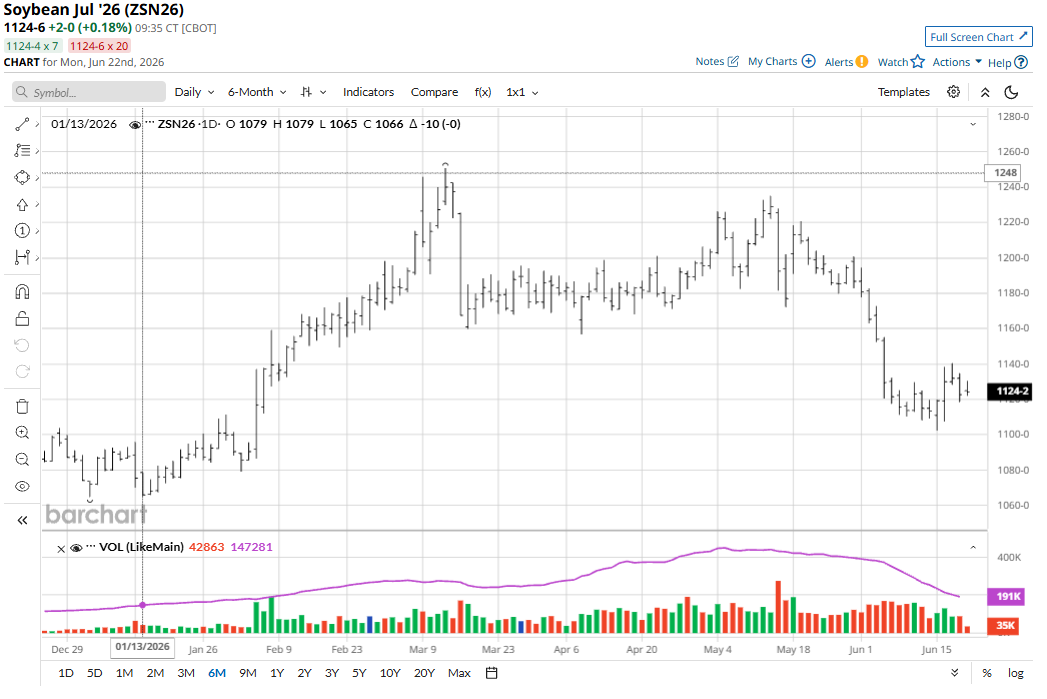

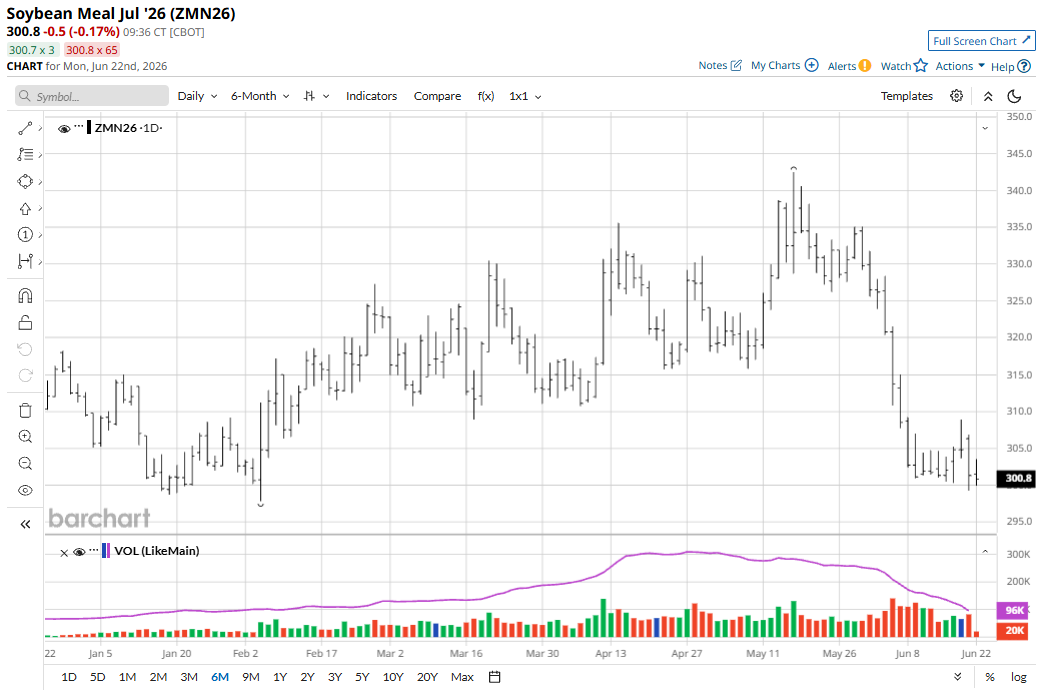

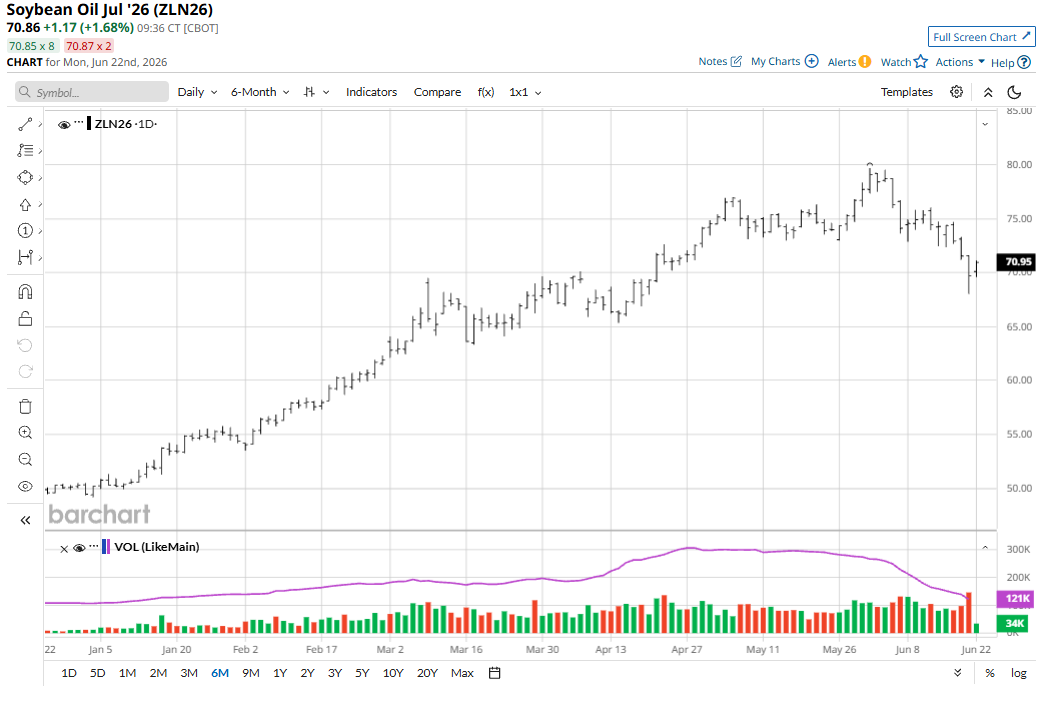

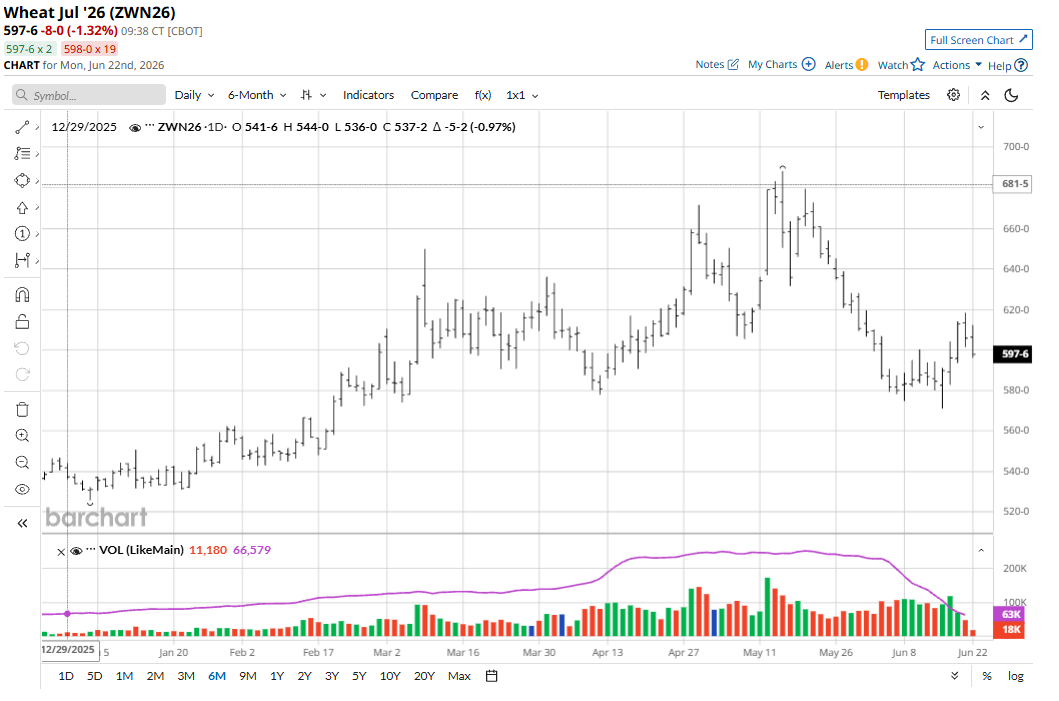

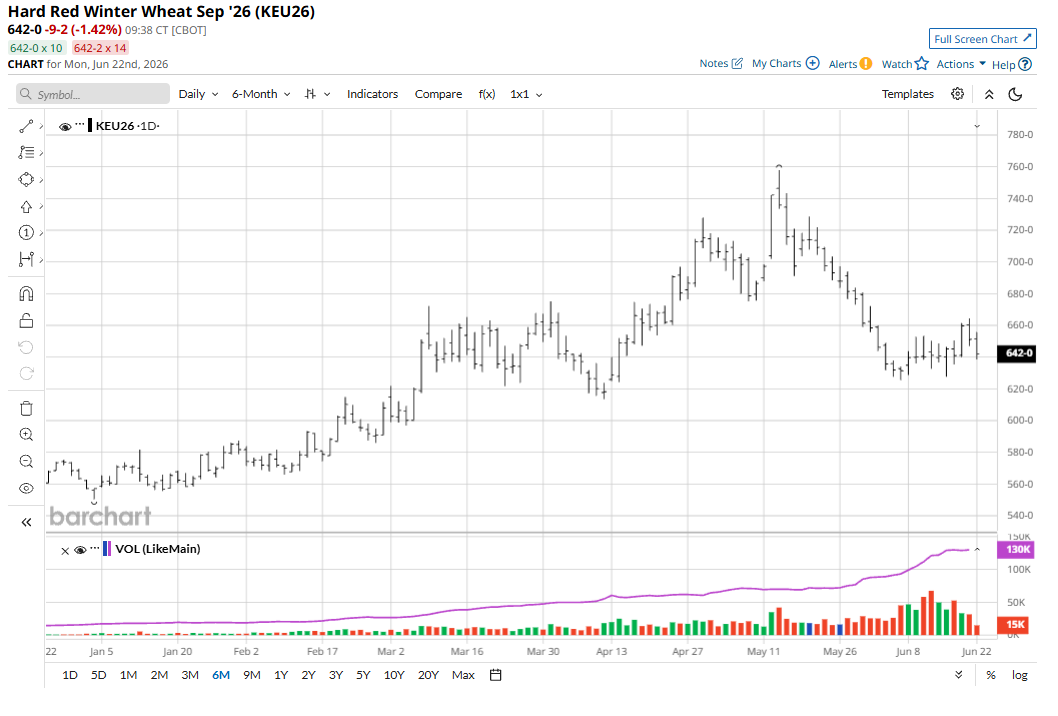

July corn (ZCN26) last Thursday fell 3 1/2 cents to $4.17 1/2 and for the week was up 4 3/4 cents. July soybeans (ZSN26) fell 9 1/4 cents to $11.22 3/4 and for the week were up 9 1/4 cents. July soybean meal (ZMN26) futures lost $3.50 to $301.30, hit a 4.5-month low, and for the week were unchanged from the previous Friday’s close. July bean oil (ZLN26) futures fell 185 points to 69.69 cents, hit a two-month low, and for the week were down 459 points. July soft red winter (SRW) wheat (ZWN26) futures on Thursday fell 7 cents to $6.05 3/4 and for the week were up 21 1/4 cents. July hard red winter (HRW) wheat (KEN26) futures lost 8 1/2 cents to $6.44 but for the week were up 9 1/2 cents.

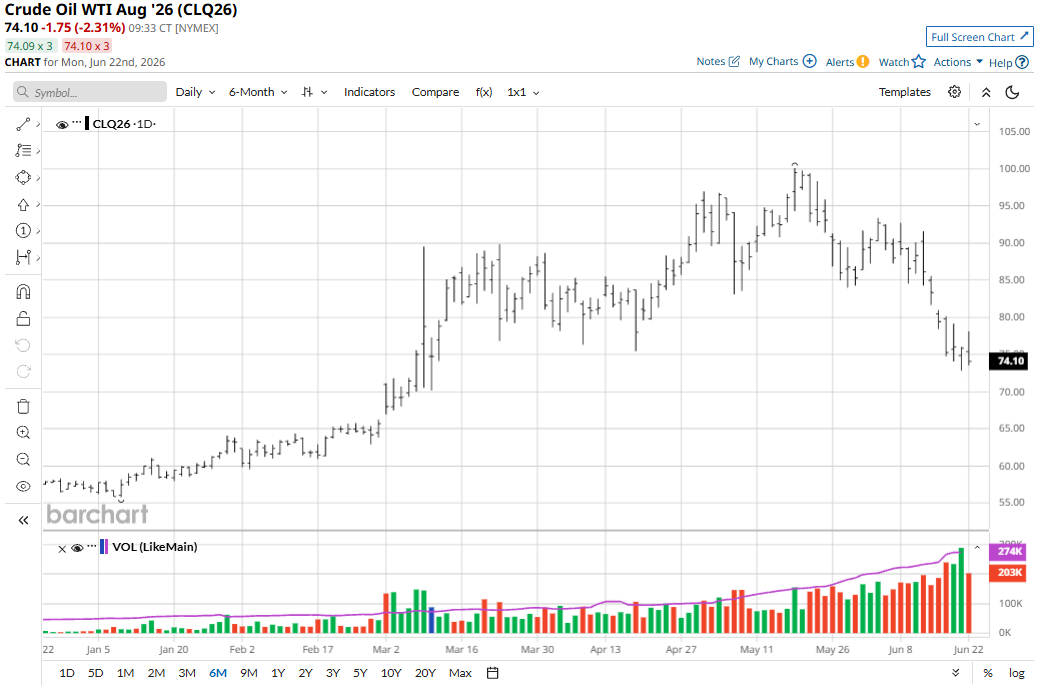

One of the biggest negatives for grain prices lately has been the big downdraft in crude oil (CBQ26) (CLQ26) prices. Crude is arguably the leader of the raw commodity sector. However, it’s my bias that oil prices, if they keep falling, will no longer play a significantly bearish role for the grain futures markets.

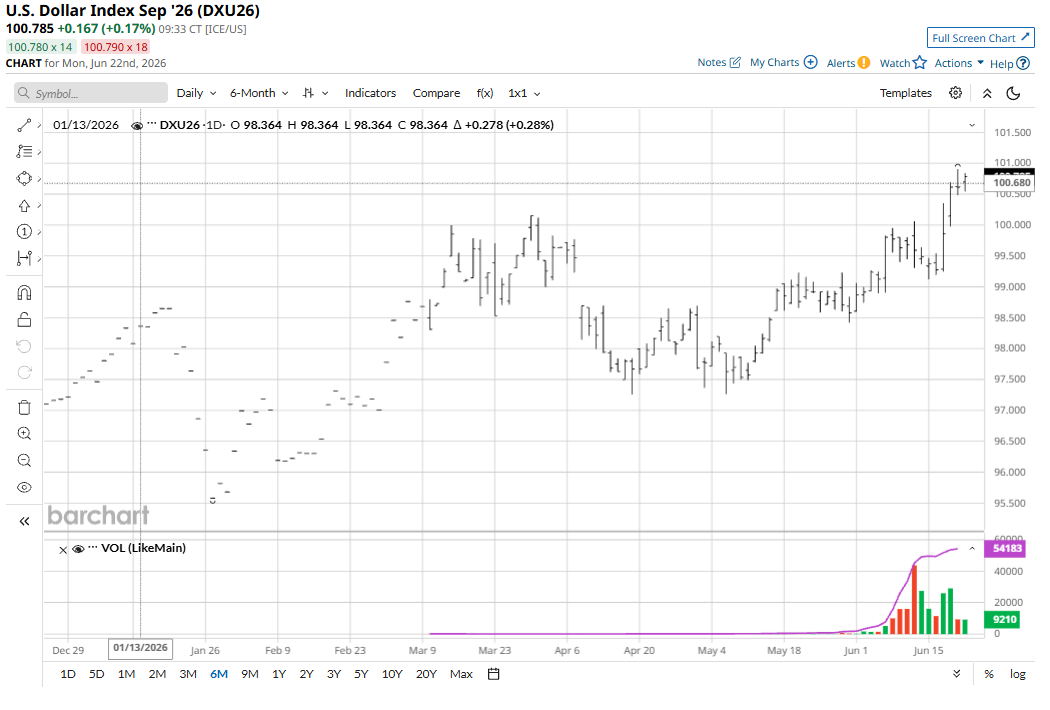

A rally in the U.S. dollar index ($DXY) over the past two months has also been a bearish element for the U.S. grain markets. A stronger greenback makes U.S. grains more expensive to purchase with non-U.S. currency on the world trade markets.

Corn Prices Still Trapped in a Near-Term Downtrend

Last week’s holiday-shortened trading week ended with the corn market bulls again frustrated. Very good growing conditions over most of the Corn Belt are squelching the bulls. Extended weather forecasts for the Corn Belt are reaching out into early July with no significant perils seen for the U.S. corn crop.

Traders will keep watching the weekly USDA crop progress reports on Monday afternoons, specifically the good to excellent condition ratings for the U.S. corn crop.

The most critical growing month of the season for U.S. corn lies just ahead. Weather in the Corn Belt still leans price-bearish. Weather forecasters say most of the U.S. Midwest will get enough rain over the next two weeks to maintain good crop conditions. There are still some dry areas in South Dakota, Nebraska, Minnesota, and northwestern Iowa, however.

The late-June USDA planted acreage updates are starting to draw trader attention and speculation on what the agency will report. There are growing notions that U.S. planted corn acres won’t be reduced much. The key corn pollination window falls between late June to early July for most of the Midwest corn crop.

Global and domestic demand for corn still favors the bullish camp. Weekly U.S. corn export inspections remain above the five-year average, supported by the value-buying in corn.

The closely followed annual Pro Farmer crop tour in late August will be a main late-growing-season market factor for corn and soybeans.

Soybean Futures Don’t Get Much Traction from Fresh China Demand for U.S. Beans

The selloffs in soybean meal and bean oil futures markets last Thursday helped to sink soybeans, despite new U.S. soybean export business to China. The USDA reported daily sales of 132,000 MT of U.S. soybeans to China and 120,000 MT to unknown destinations during 2026-27. In the meantime, the agency reported weekly U.S. soybean sales totaled 424,900 MT during the week ended June 11, up noticeably from the previous week and four-week average.

Weather in the Midwest also leans price-bearish for soybeans. Yield potential remains high as rain is in the forecast for the next two weeks amid mild temperatures through at least most of this week. Good soil moisture will support good plant development at least into early July for most of the U.S. soybean crop.

August is arguably the most important growing month for most of the U.S. soybean crop. That means there is still plenty of time for a weather-market scare to pop up in soybeans.

Wheat May Have to Lead Corn, Soybeans Out of Their Price Slumps

The winter wheat futures markets on Thursday ended a fairly good holiday-shortened trading week on a down note. However, the SRW and HRW bulls have started working on price uptrends on the daily bar charts, although they have more heavy lifting ahead of them, amid sickly corn and soybean markets. It could well be that the improved technical postures in winter wheat markets will be the impetus for corn and soybean futures markets to end their near-term price downtrends. Don’t be surprised if winter wheat futures turn out to be the grains complex leaders on daily price moves over the next week or so.

Monday afternoon’s weekly USDA crop progress reports and the U.S. winter wheat condition ratings will be closely scrutinized by wheat traders.

The U.S. winter wheat harvest is now in full swing and will move north in the coming weeks. Harvest in HRW country is well underway, with Texas at 75% complete and Kansas at 28%. Abandonment rates are likely to trend higher this year as harsh drought and freezes hit fields hard. Early reports provided to the Kansas Wheat Commission show protein quality near average in harvested fields.

Tell me what you think. I read every one of your emails. My email address is jim@jimwyckoff.com. I enjoy getting feedback from all of you, my valued Barchart readers.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)