July corn (ZCN26) futures on Friday rose 1 cent to $4.63 1/4 and for the week were up 7 1/2 cents. July soybeans (ZSN26) rose 2 1/4 cents to $11.96 ½ and for the week were up 19 1/2 cents. July soft red winter (SRW) wheat (ZWN26) futures on Friday fell 1 1/4 cents to $6.46 1/4 and for the week were up 10 1/2 cents. July HRW wheat (KEN26) futures lost 5 cents to $6.82, hit a two-week low, and for the week were down 6 cents. Grain market bulls had a decent week last week after prices in mid-May tanked following a disappointing summit meeting between President Donald Trump and Chinese leader Xi Jinping.

Corn in Middle of Choppy Trading Range

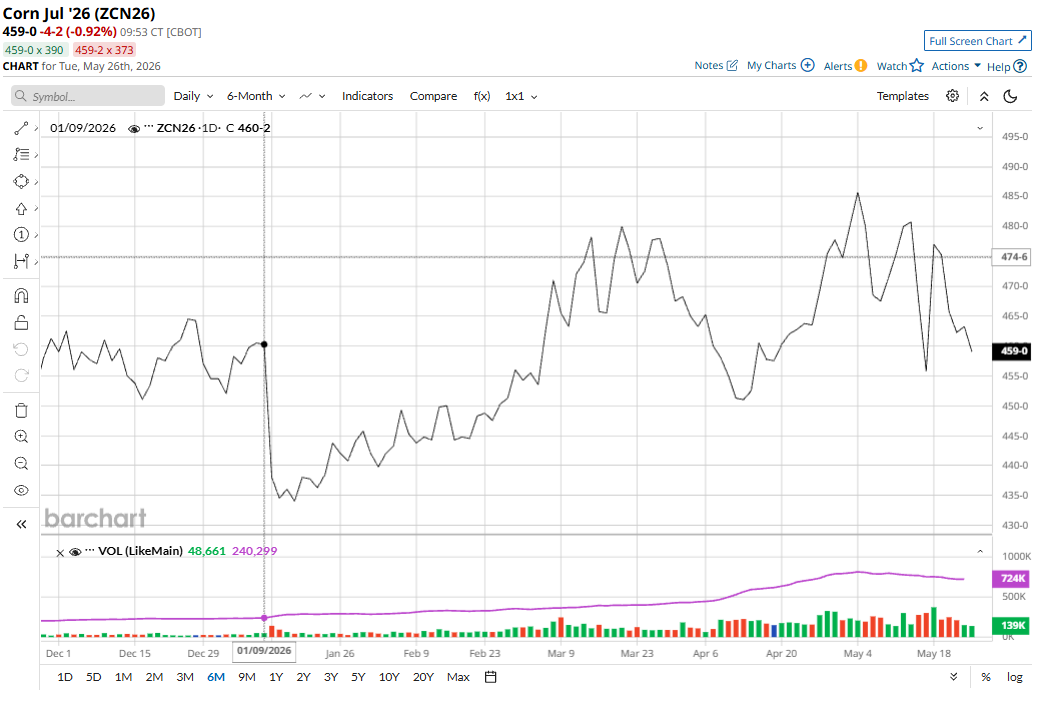

July corn futures are presently trapped right in the middle of a choppy trading range on the daily bar chart. Key for the bulls during this holiday-shortened trading week will be keeping July futures prices above technical support at the May low of $4.55. Hefty sell stop orders are likely to reside just below that level.

Traders will keep watching the weekly USDA crop progress reports. This week’s reports will likely show that most of the U.S. corn crop has been planted.

Weather conditions in the Midwest lean mostly price-bearish for the corn futures market. Regular rounds of rain will occur in much of the lower Midwest into Thursday. However, a much drier weather pattern will occur after that.

Don’t be surprised to see some degree of a weather market scare pop up rapidly in corn and/or soybeans in the coming months. More years than not, one occurs. They develop quickly and can then fizzle out just as fast. The key growing period for most of the U.S. corn crop occurs during the first half of July. Hot weather during the key pollination period for the corn crop can quickly sap yield potential — especially if it remains very warm at night.

Soybeans Fade from May Highs

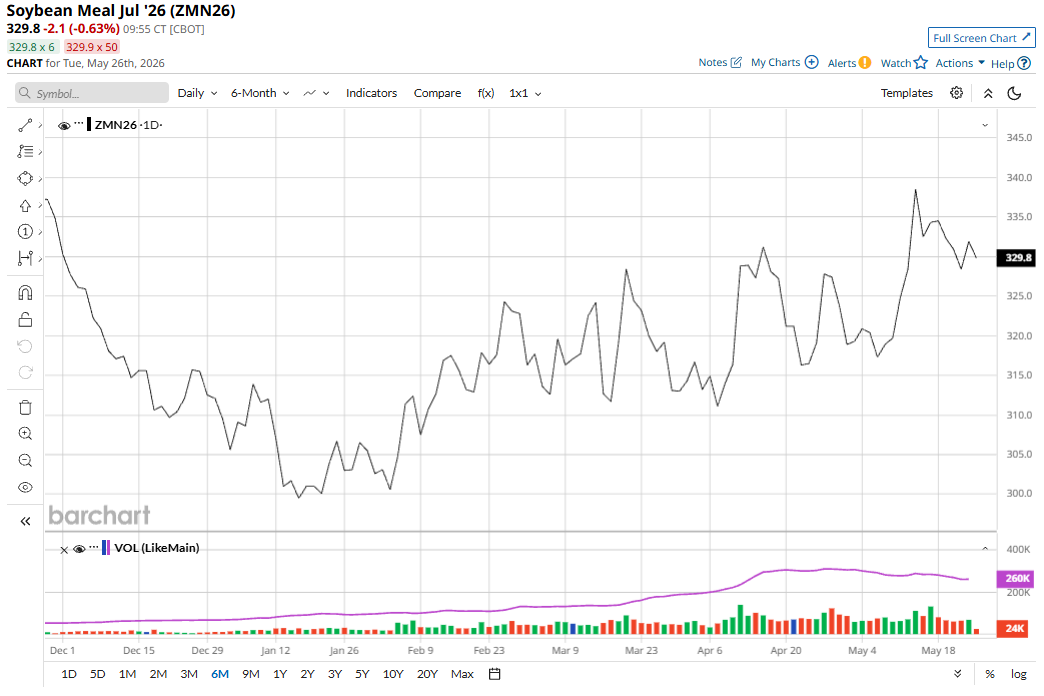

The soybean market started last week very strong but faded as the week progressed. Lingering concerns that China will not be adding to U.S. soybean purchases continue to hang over the soybean and meal (ZMN26) markets after the recent Trump-Xi meeting.

The USDA on Friday reported daily sales of 252,00 MT of U.S. soymeal for delivery to unknown destinations, which worked to lift soybean meal prices.

Tuesday’s weekly USDA crop progress data will be closely scrutinized by soybean complex traders as planting is expected to be progressing well.

U.S. soybean-growing weather also leans price-bearish. A favorable mix of weather is expected to prevail in northern production areas through next week.

The late-June USDA plantings update will be an important early summer price point for the grain futures.

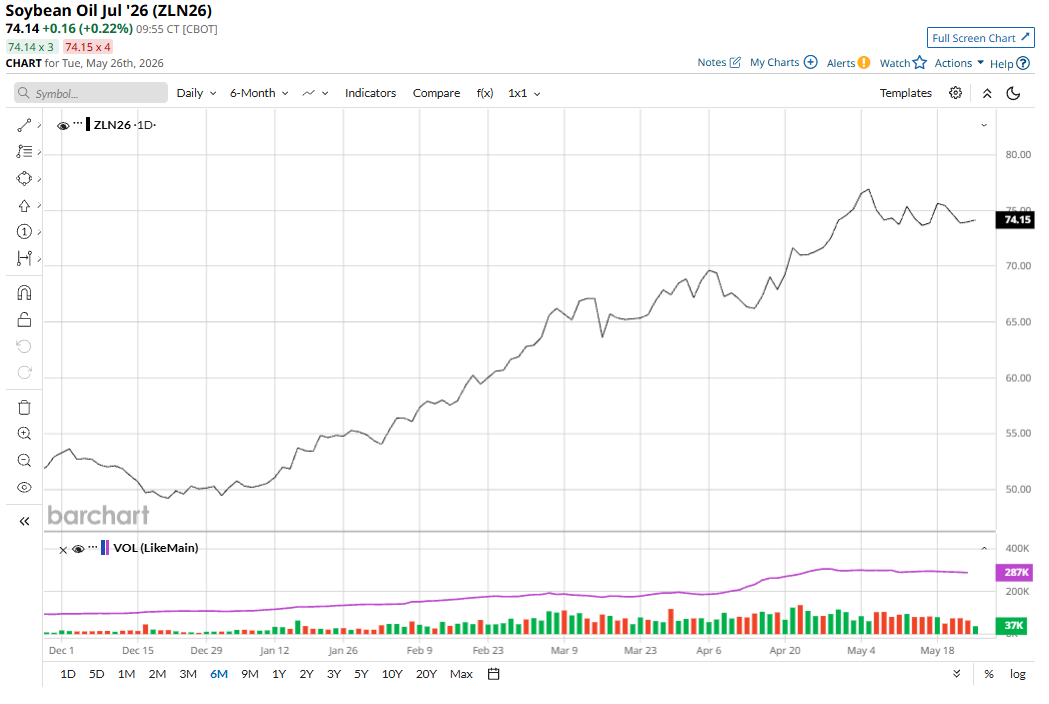

Nymex crude oil (CLN26) futures pushed back below the key $100-per-barrel mark last week, on hopes of a U.S. peace deal with Iran, which in turn pressured price action in soybean oil futures. However, longer-term demand for biodiesel fuel remains firm as inflation impacts are likely to linger from the steep rise in oil prices relative to year ago levels as governments around the globe look for ways to lower energy costs.

The soybean harvest in Brazil is now nearly complete and cheaper bean supplies in South America are likely to limit any major purchases of U.S. beans from China in the coming months.

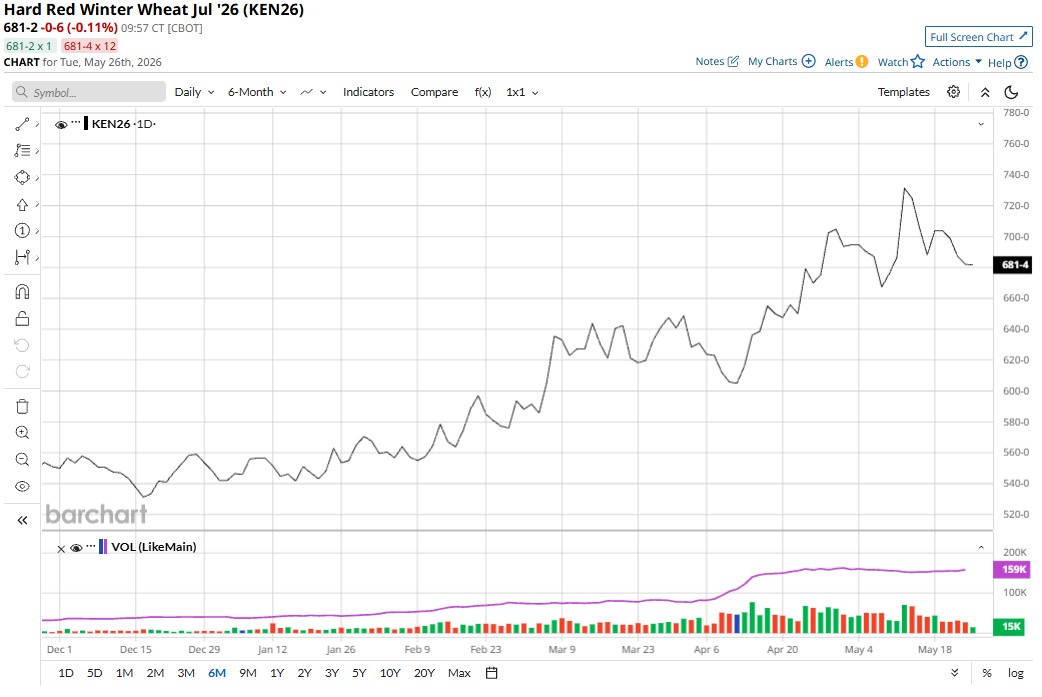

Winter Wheat Bulls Also Losing Steam

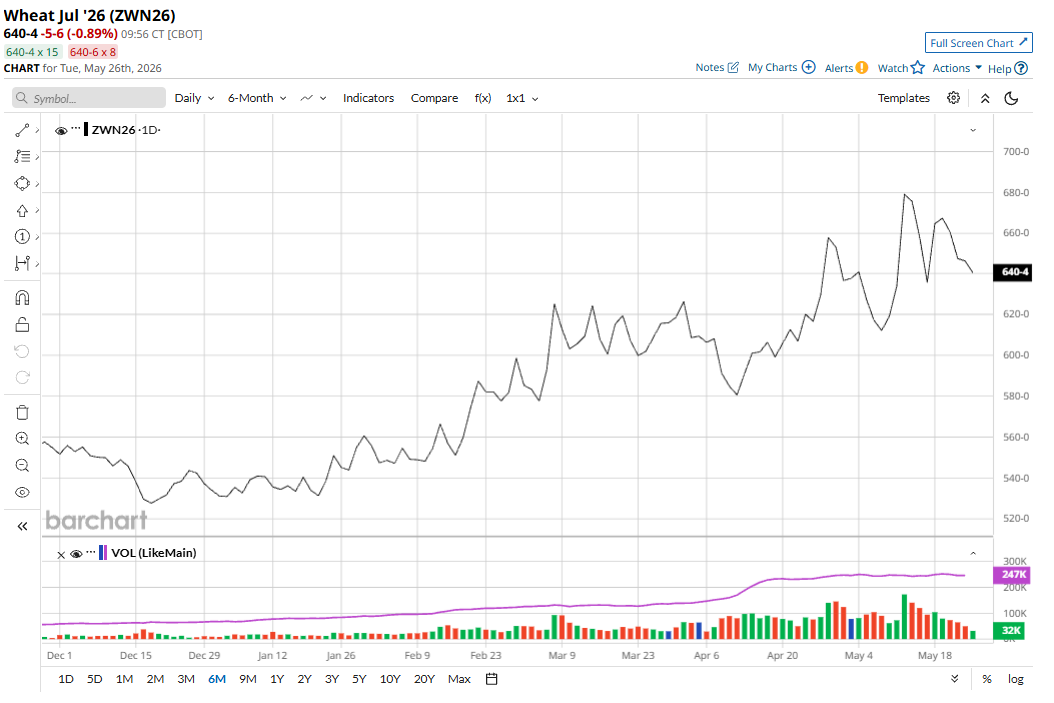

The winter wheat futures markets bulls came out of the gate strong last Monday but then faded after that. Profit-taking pressure and weak long liquidation were featured last week. Friday’s technically bearish weekly low closes in July SRW and HRW futures suggest there could be some more follow-through selling early this week.

However, there are still bullish fundamentals in the wheat market that are likely to come back to the fore, including a deteriorating U.S. hard red winter wheat crop. Tuesday afternoon’s weekly USDA crop progress reports and the U.S. winter wheat condition ratings will be closely scrutinized by wheat traders.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)