/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

For much of the artificial-intelligence (AI)-driven semiconductor rally, Micron Technology (MU) has been one of Wall Street’s hottest trades, fueled by explosive demand for high-bandwidth memory chips and tightening DRAM supply. But while bullish investors continue to chase the AI narrative, short sellers are quietly building a sizable bet that the rally may be nearing exhaustion.

Short interest in Micron has climbed to roughly 37.3 million shares, near the highest levels seen in years, after rising steadily through 2026. This represents 3.32% of the public float. The latest data shows bearish positions increased another 2.6% in late April following a 15.9% jump earlier in the month.

The growing wave of bearish positioning comes despite Micron’s massive gains from the AI boom. Some investors might be betting against the stock with the belief that expectations have become too aggressive after Micron’s meteoric surge, with concerns centered on valuation, cyclical memory pricing risks, and the possibility that today’s AI-driven supply shortages eventually turn into oversupply. Plus, Micron’s rapidly expanding capital spending plans are looked at as a potential warning sign.

That has created a growing tug-of-war between momentum investors betting the AI cycle is still in its early stages and short sellers wagering that semiconductor enthusiasm has simply gone too far, too fast. What should be your next move?

About Micron Technology Stock

Micron Technology is a semiconductor company that designs, develops, manufactures and sells memory and storage products globally, including DRAM, NAND flash memory, HBM, solid-state drives (SSDs) and other memory modules. Headquartered in Boise, Idaho, Micron operates multiple business units serving cloud and data center, mobile and client, automotive and embedded, and enterprise segments worldwide. Micron’s market cap stands at $859.4 billion, putting it among the largest and most valuable players in the global semiconductor industry.

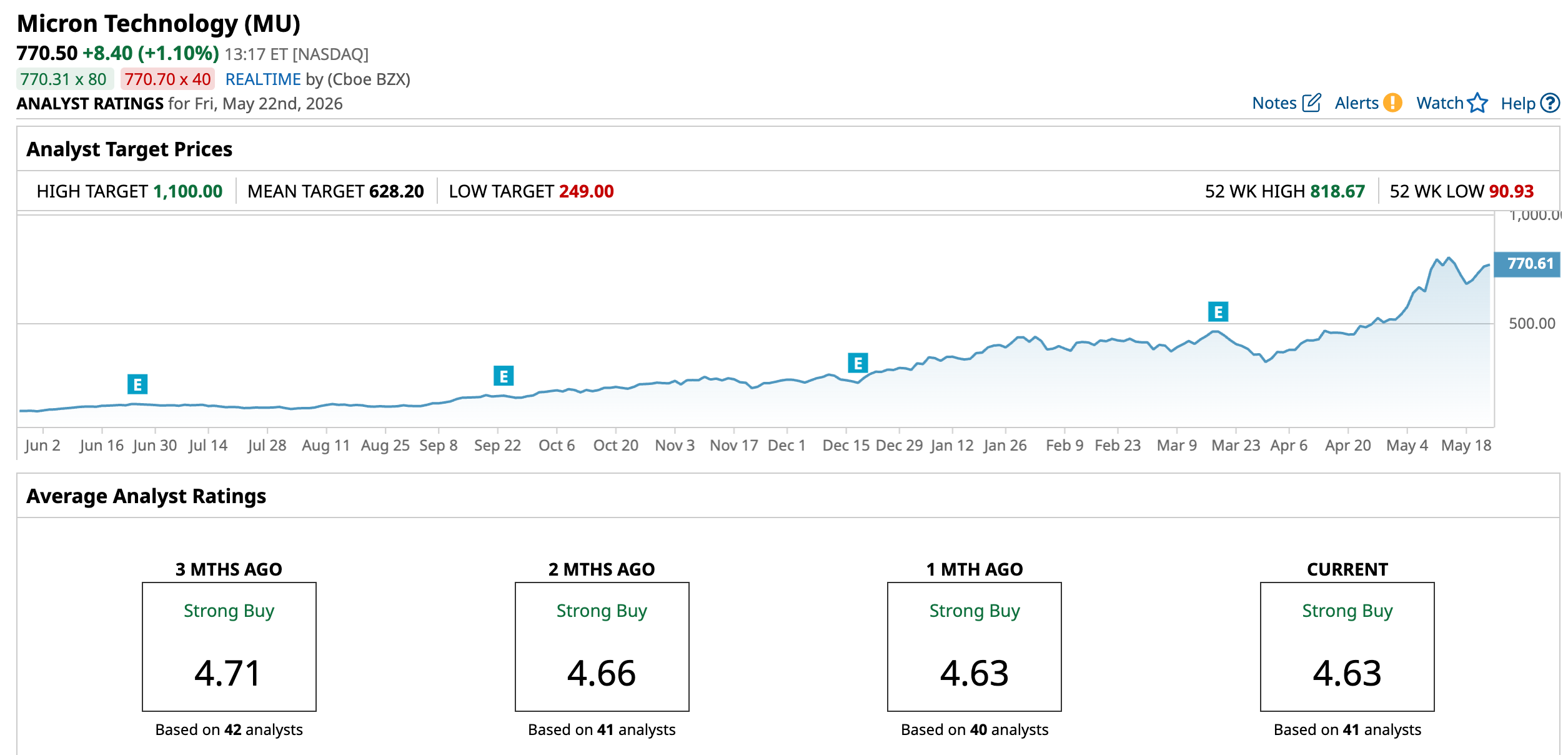

Micron has been one of the best-performing semiconductor stocks of the AI era, delivering enormous gains as investors rushed into companies tied to high-bandwidth memory and AI data center demand. The stock recently climbed to a new 52-week high of $818.67 on May 11 and remains up 168.3% year-to-date (YTD), dramatically outperforming most large-cap technology peers.

Over the past 12 months, shares have surged 707.4% as tightening DRAM and NAND supply, booming AI infrastructure spending, and aggressive pricing gains transformed Micron into one of the market’s strongest momentum trades. The rally has accelerated further in recent weeks, with Micron gaining 57.1% over the past month alone.

Yet despite the extraordinary momentum, bearish investors continue increasing their bets against the company.

However, the stock still seems to be trading at a discount compared to industry peers at 12.66 times forward earnings.

Better-than-Expected Q2 Performance

Micron reported its fiscal second quarter 2026 (ended Feb. 26, 2026) results on March 18, delivering one of the strongest quarters in its history, driven by unprecedented demand for AI-related memory products.

The company posted revenue of $23.9 billion, representing a massive year-over-year (YOY) increase of 196.4%. This surge reflects a sharp recovery in DRAM and NAND pricing alongside explosive demand for HBM used in AI data centers.

Profitability expanded even more dramatically. Micron reported adjusted earnings-per-share of $12.20, up roughly 682.1% YOY from about $1.56 in fiscal Q2 2025 and exceeding expectations.

At the segment level, the Cloud Memory Business Unit generated $7.8 billion in revenue, representing an increase of roughly 163% YOY, while gross margins improved to 74% from 55%.

The Core Data Center Business Unit delivered one of the strongest growth trajectories, with revenue rising to $5.7 billion from $1.8 billion, with margins also expanding meaningfully as gross margin improved to 74% from 47%.

In the Mobile and Client Business Unit, revenue reached $7.7 billion, marking a sharp 244.9% YOY increase. This segment’s gross margin rose dramatically to 79% from just 15%.

The Automotive and Embedded Business Unit also posted strong growth, with revenue climbing to $2.7 billion from $1 billion.

Management further issued exceptionally strong guidance for fiscal Q3 2026, signaling continued momentum. The company expects revenue of around $33.5 billion (plus or minus $750 million) and EPS of $19.15 (plus or minus $0.40).

Also, the consensus EPS estimate of $57.82 for fiscal 2026 reflects an increase of 652.9%, while the EPS estimate of $99.23 for fiscal 2027 indicates a 71.6% rise YOY.

What Do Analysts Expect for Micron Stock?

Most recently, Mizuho raised its price target on Micron Technology to $800 from $740 while maintaining an “Outperform” rating, citing strong DRAM and NAND pricing expectations through 2026 and 2027.

Also, BofA Securities raised its price target on Micron Technology to $950 from $500 while maintaining a “Buy” rating, citing continued AI-driven memory demand and tight industry supply conditions.

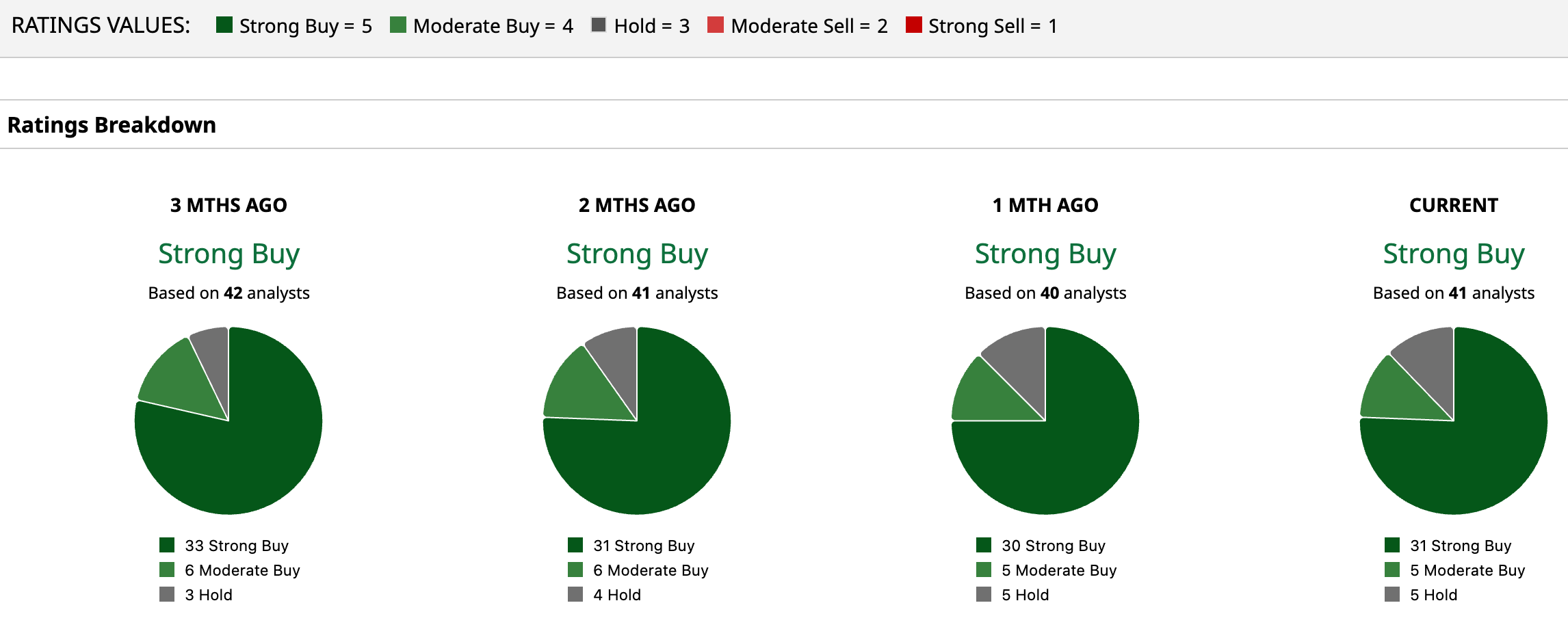

Overall, MU has a consensus “Strong Buy” rating. Of the 41 analysts covering the stock, 31 advise a “Strong Buy,” five suggest a “Moderate Buy,” and five analysts are on the sidelines, giving it a “Hold” rating.

While the stock has surged past the average analyst price target of $628.20, the Street-high target price of $1,100 suggests that the stock could rally as much as 42.76%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)