/Tesla%20car%20with%20symbol%20by%20Michael%20Fortsch%20via%20Unsplash.jpg)

When I see a stock chart like Tesla’s (TSLA), I instantly consider three different paths. I can try to make money on a continued price decline. I can collar it, so I can grab the rebound but be protected if this is just another leg down. Or I can do nothing. Since the third choice would not make for much of an article, let’s examine the other two.

This daily view is at best weak, and at worst the start of something deeper. I marked those lines on this chart a while ago, using a great Barchart feature that allows them to stay there until I remove them. I drew the top when it traded there for the second time in 12 months, late last year, and started to dip. That’s usually a sign the bears are in charge.

With a volatile “story stock” like this one, the chart sometimes doesn’t do it justice. For instance, the lower boundary at $367 is 7% below Monday’s close. That’s a lot to me! So the next shelf level below, at $220, makes me not want to take much risk below perhaps $360 or so.

Why Is TSLA Stock Down?

The narrative has shifted from a pure electric vehicle story to a high-stakes bet on autonomous AI, creating a stark divide between those who see a trillion-dollar robotics future and those who see a car company with a crumbling foundation.

The bull case centers on Tesla’s successful transition into a physical AI and energy powerhouse. Analysts point to the massive growth in the energy storage segment, where Megapack deployments have created a multi-year backlog and a high-margin revenue stream that is decoupled from car sales. Furthermore, bulls argue that Tesla’s valuation should be compared to Nvidia (NVDA) or Microsoft (MSFT) rather than Ford (F) or Toyota (TM).

The belief is that Tesla is building a software-as-a-service model for transportation that will eventually generate the majority of its profits. From this perspective, the current price slide is merely a healthy consolidation before a late-2026 surge toward a $2 trillion market cap.

The bear case is grounded in deteriorating automotive fundamentals and a growing regulatory storm. For the first time in its history, Tesla saw a slight annual revenue contraction in 2025, and Q1 2026 delivery estimates are tracking below 350,000 units, a figure that suggests the EV market has hit a saturation point.

Bears argue that the aging Model 3 and Model Y designs are losing ground to fresh competition from BYD (BYDDY) and legacy automakers who have pivoted to hybrids.

The slide in the stock price reflects a market that is no longer willing to trade on Elon Musk’s promises alone. It is instead now demanding tangible execution. With over $20 billion in planned AI capital expenditure for 2026, the company is spending heavily to secure its future, but this is compressing margins in the near term.

Collaring TSLA with Room to Vroom

In the above example, I used that $360 level for a put option out to August. And with a stock like this, which can catch a bull wave at any time given its fervent fan base, I targeted upside all the way at $500. TSLA is typically a solid collar stock, and it did not disappoint here. Nearly 2:1 up/down ratio, and a modest 2.3% net cost of the options.

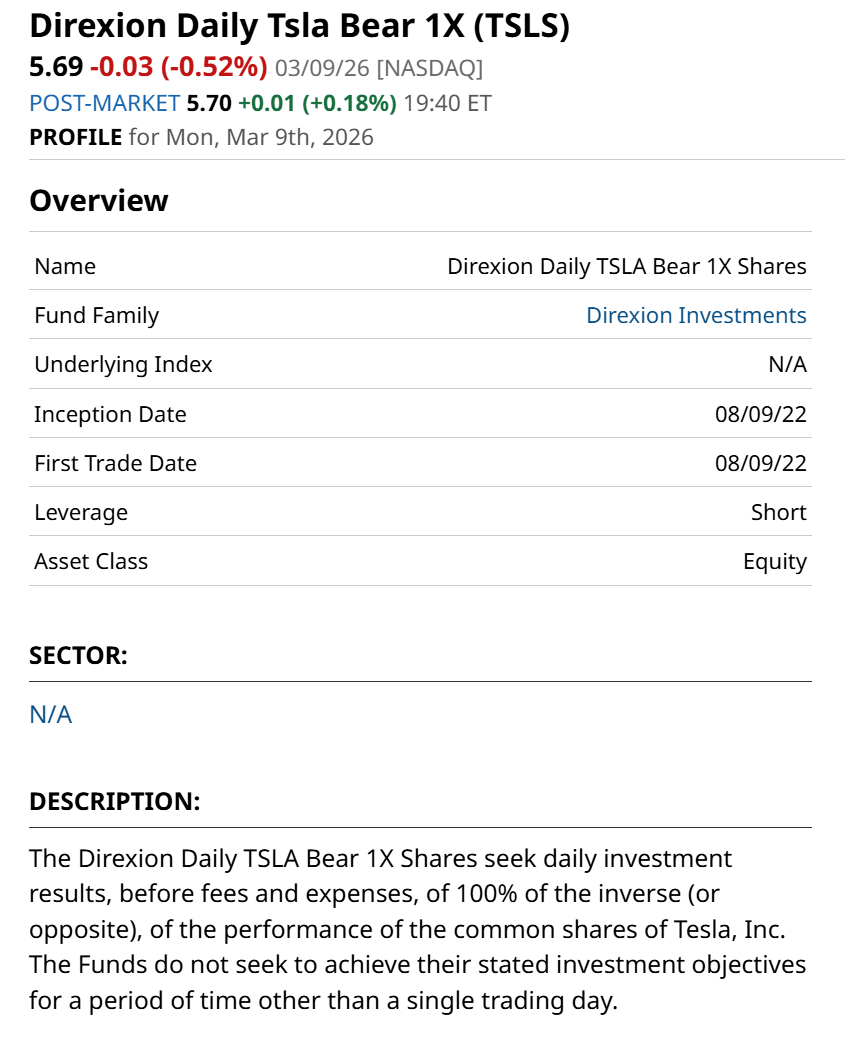

The Direxion Daily TSLA Bear 1X ETF (TSLS) would be the straight bearish way to play TSLA. As shown here, this $80 million ETF, now more than 2 years old, simply moves in the opposite direction of the stock.

Whether the stock finds its footing or continues to slide will likely depend on the outcome of the NHTSA report and whether the robotaxi pilot can prove its safety and scalability to a skeptical public.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)