/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

The S&P 500 ($SPX) has delivered a solid performance so far this year, but a small group of stocks has left the broader market far behind. Only 14 companies in the benchmark index have posted year-to-date (YTD) gains of more than 100%, highlighting just how concentrated this year’s biggest winners have been. Unsurprisingly, many of these top performers are tied to semiconductors, data storage, and other areas benefiting directly from the continued expansion of artificial intelligence (AI) infrastructure.

However, a triple-digit rally does not necessarily mean a stock’s best days are behind it. The more important question for investors is whether the fundamental catalysts behind those gains remain intact—and which of these high-growth names still offers the most attractive upside through the remainder of the year. After reviewing the names on the list, Micron Technology (MU) stands out as my favorite.

With that, let’s take a closer look at why Micron has been one of the S&P 500’s biggest winners in 2026—and why I believe it could remain among the index’s strongest performers for the rest of the year.

About Micron Technology Stock

Micron Technology, Inc. is a leading semiconductor company that designs, manufactures, and markets memory and storage products. Its portfolio includes DRAM, NAND flash, and other advanced memory solutions used across data centers, smartphones, PCs, automobiles, industrial applications, and consumer electronics. As AI workloads drive demand for faster and higher-capacity memory, Micron has become a key supplier to hyperscale cloud providers and AI infrastructure companies, positioning it as one of the primary beneficiaries of the ongoing AI boom. It has a market cap of $1.11 trillion.

Shares of the memory chipmaker have rallied 205% YTD, fueled by soaring demand for high-bandwidth memory and advanced DRAM used in AI servers. However, the stock has retreated from its late-June peak above $1,200 amid growing investor concerns that the AI boom has become overextended.

Micron Ranks Among the S&P 500’s Best Performers in 2026

Micron Technology ranks as the third-best-performing stock in the S&P 500 YTD, far outpacing the benchmark’s solid 10.6% gain over the same period. Only Sandisk (SNDK) and Dell Technologies (DELL) have outperformed Micron in the S&P 500 this year, posting respective YTD gains of 575.2% and 224.9%.

Meanwhile, only a handful of stocks in the benchmark index have delivered triple-digit gains so far this year. Besides the trio mentioned above, the list includes Seagate (STX), Western Digital (WDC), Intel (INTC), Advanced Micro Devices (AMD), Marvell (MRVL), Moderna (MRNA), Applied Materials (AMAT), Flex (FLEX), Fortinet (FTNT), DaVita (DVA), and Lumentum (LITE). With that, the companies that have had the greatest impact on the S&P 500’s performance are concentrated in the semiconductor, data storage, and broader technology sectors, reflecting strong investor enthusiasm for the AI trade.

That brings us to the logical question: Will they continue to do so in the second half of the year? And more importantly, if they do, which high-growth name on the list will deliver the strongest returns—or at least rank among the top performers? Well, as you may have already guessed, my top pick is Micron, and in the following paragraphs, I’ll explain why.

Big Tech Spending and Memory Shortages Create a Powerful Setup for Micron

When adding a company either to my watchlist or portfolio, I always look for an underlying fundamental catalyst that will drive its stock higher. And in Micron’s case, it is obvious: hyperscalers’ capital spending. The biggest U.S. tech firms are pouring massive amounts of money into building the infrastructure needed to power AI, which translates directly into enormous revenue for makers of graphics processing units, memory chips, and central processing units.

The so-called AI hyperscalers—Alphabet (GOOG) (GOOGL), Microsoft (MSFT), Amazon.com (AMZN), and Meta Platforms (META)—are expected to spend more than $700 billion on capex this year. In fact, that figure could be even higher, as Meta alone has recently committed an additional $40 billion to its massive data center campus in Louisiana. With Big Tech earnings kicking off next week, we will get the latest update on AI spending, and it is expected to be even higher. This would undoubtedly be excellent news for Micron and other chip and AI infrastructure companies.

More importantly, analysts expect Big Tech’s AI spending to continue climbing in the years ahead. For example, BofA Global Research analyst Vivek Arya expects Big Tech companies to spend about $1.5 trillion on global cloud and AI infrastructure in 2027. And memory components are set to account for roughly 35% to 40% of that spending.

Another key point is that demand for memory and other AI hardware is significantly outstripping supply, sending memory chip prices soaring. With supply not expected to catch up with demand anytime soon, memory chip prices are expected to keep climbing. KeyBanc analyst John Vinh expects DRAM prices to rise 15% to 20% quarter-over-quarter in the third quarter, followed by another 15% increase in the fourth quarter. He also forecasts that NAND flash memory prices will climb 30% to 40% in the third quarter, followed by another 15% increase in the fourth quarter. Meanwhile, high-bandwidth memory, a key component for AI servers and a major driver of profit growth, is expected to more than double in price next year.

Surging memory prices have been a boon for Micron. First, they provide the company with unprecedented pricing power, allowing it to expand margins and drive explosive profit growth. Micron reported an adjusted gross margin of 84.9% in its most recent quarter, making it one of the most profitable companies in the technology sector. Second, they push Micron’s customers to enter into long-term supply agreements.

Micron’s Long-Term Supply Deals Could Be a Game Changer

As I argued in my previous article on Micron, long-term supply agreements could be a game-changer for the company. These deals include upfront cash deposits, predefined pricing ranges, and minimum purchase commitments. With that, these agreements allow Micron to lock in higher prices for its memory chips well into the future, effectively transforming its business model.

Historically, the memory chip industry has been defined by severe, 4- to 7-quarter cycles of shortages followed by brutal gluts. And because investors lacked long-term conviction, memory companies like Micron have historically traded at very low P/E multiples. Currently, Micron trades at just 6.53x projected FY27 adjusted earnings, compared with a forward multiple of 21.22x for the S&P 500 Index.

If the company signs more long-term agreements in the coming quarters—and I expect it will (see my previous Micron article to learn why)—it should help create a more stable earnings profile. And a more stable earnings profile should help Micron move beyond its traditional boom-and-bust cycle, which could trigger a valuation re-rating, potentially bringing its multiple closer to that of the S&P 500. Such a re-rating would create additional upside for the stock, even without any increase in expected earnings.

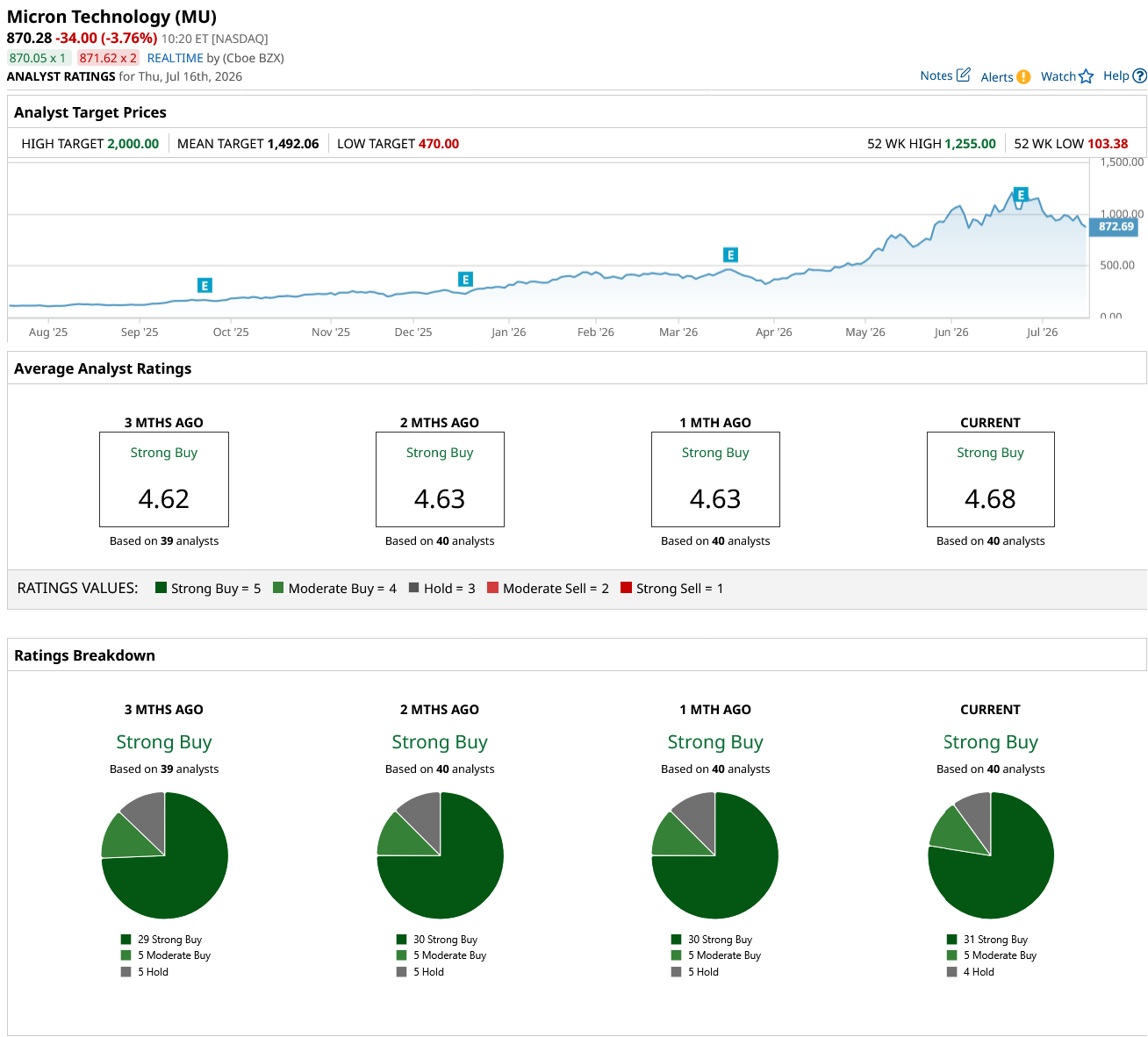

What Do Analysts Expect for MU Stock?

Wall Street analysts remain highly bullish on MU stock, as evidenced by its consensus “Strong Buy” rating. Among the 40 analysts covering the stock, 31 rate it a “Strong Buy,” five assign a “Moderate Buy” rating, and four recommend holding. The average price target for MU stock is $1,492.06, implying upside potential of 71% from current levels.

Putting it all together, I believe MU stock could deliver double- to triple-digit returns over the next 12 to 18 months as the company’s fundamentals remain exceptionally strong. Soaring memory chip prices should continue driving explosive profit growth for Micron while encouraging its customers to sign long-term supply agreements. The latter could trigger a valuation re-rating and create even greater upside. I view the recent pullback in MU stock as a buying opportunity, giving investors the chance to add shares at a more favorable risk-reward ratio. I expect the next leg higher in MU stock to begin with the start of Big Tech earnings season, when hyperscalers will likely provide higher capital expenditure guidance.

On the date of publication, Oleksandr Pylypenko had a position in: GOOGL, MSFT, AMZN, META. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)