/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Micron Technology (MU) has become one of the biggest beneficiaries of the artificial intelligence (AI) boom, and its latest earnings report made that clearer than ever. The memory chipmaker delivered blockbuster quarterly results, issued guidance that easily topped Wall Street’s expectations, and showed that demand for its high-bandwidth memory and advanced storage products remains exceptionally strong. Unsurprisingly, investors cheered the report, sending MU stock sharply higher.

Still, the most important takeaway from Micron’s report may not have been the earnings beat itself. Instead, it was the company’s progress in securing long-term supply agreements with major customers. These deals gave management enough visibility to project that supply shortages will extend beyond 2027, marking a notable shift from the company’s previous outlook, which focused only on the current calendar year.

The key question for investors is whether the company’s long-term agreements can turn this current upcycle into something more durable—and whether MU stock still has room to run after its massive year-to-date (YTD) rally. With that, let’s take a closer look.

About Micron Technology Stock

Micron Technology is a leading semiconductor company that designs, manufactures, and markets memory and storage products. Its portfolio includes DRAM, NAND flash, and other advanced memory solutions used across data centers, smartphones, PCs, automobiles, industrial applications, and consumer electronics. As AI workloads drive demand for faster and higher-capacity memory, Micron has become a key supplier to hyperscale cloud providers and AI infrastructure companies, positioning it as one of the primary beneficiaries of the ongoing AI boom. Its market cap currently stands at $1.28 trillion.

Shares of the memory chipmaker have rallied 262% on a YTD basis, driven by surging demand for high-bandwidth memory and advanced DRAM used in AI servers.

MU Stock Soars After Blockbuster Earnings

Last Thursday, MU stock jumped over 15% after the largest U.S. maker of computer memory chips posted upbeat FQ3 results, issued FQ4 guidance that far exceeded Wall Street estimates, and said the chip shortage would extend beyond 2027.

The memory chipmaker reported fiscal third-quarter revenue of $41.46 billion, more than four times higher than a year earlier. Unsurprisingly, that explosive growth was fueled by the company’s two data center segments, which now make up 61% of total sales. The top-line figure also smashed Wall Street’s expectations of $35.9 billion.

Micron’s closely watched adjusted gross margin more than doubled to 85% last quarter, also exceeding Wall Street’s expectations. That improvement was driven by a roughly 260% year-over-year (YoY) increase in average selling prices for DRAM products and an approximately 310% rise in average selling prices for NAND products. Even compared with the previous quarter, average selling prices for DRAM and NAND products climbed about 60% and 80%, respectively, underscoring severe supply shortages driven by the ongoing AI infrastructure buildout. Moreover, Micron expects prices to rise further as it guided for its gross margin to rise to 86% in the current quarter.

Surging revenue and rapidly expanding margins caused Micron’s profit to soar. The company posted a third-quarter adjusted profit of $28.86 billion, or $25.11 a share, compared with a profit of $2.18 billion, or $1.91 a share, in the same period a year earlier.

In addition, Micron issued upbeat guidance for the current quarter. The company said it expects fiscal fourth-quarter revenue of $49 billion to $51 billion and adjusted earnings of $30 to $32 per share. Both figures smashed analysts’ estimates, signaling that the company’s AI-fueled growth momentum remains strong.

Micron’s Long-Term Supply Deals Could Change Its Valuation Story

Beyond blowout quarterly results and guidance, Micron’s earnings report featured another particularly encouraging development for investors: strategic customer agreements (SCAs).

The company said it signed long-term supply agreements with 15 new customers, up from just one such agreement reported in the previous quarter. These deals include upfront cash deposits, predefined pricing ranges, and minimum purchase commitments. With that, Micron now has 16 SCAs, averaging three years in duration and representing approximately $100 billion in committed revenue. The deals gave management enough visibility to project that the supply shortage will extend beyond 2027, whereas they had previously limited their commentary on industry conditions to the current calendar year.

Micron’s shift toward long-term customer agreements could help the company mitigate the boom-and-bust cycles that have long plagued the memory chip industry. And this is particularly important because memory companies like Micron have historically traded at very low P/E multiples due to investors’ lack of long-term conviction. Over the past decade, Micron’s median forward P/E ratio has been roughly half that of the S&P 500 Index. Even after MU stock’s massive rally since the start of the year, it currently trades at just 7.61 times projected FY27 adjusted earnings, compared with a forward multiple of 22.06 for the S&P 500 Index ($SPX).

I expect Micron to sign more long-term deals in the coming quarters for two simple reasons. First, its customers, particularly hyperscalers, may be compelled to enter into these agreements to secure access to memory and storage chips, given their critical role in AI servers and other products. This is supported by the fact that the AI infrastructure buildout is not expected to slow anytime soon, with hyperscalers and Tier 2 cloud providers projected to invest more than $3.5 trillion in AI-related capital expenditures through 2030, according to Bloomberg Intelligence. Second, companies can hedge against future increases in memory prices by entering into long-term agreements that include pricing floors and ceilings. Memory prices are likely to continue surging over the coming years, as supply is not expected to catch up with demand until around 2029. With that, more long-term agreements should support a more stable earnings profile for Micron and could lead to a valuation re-rating, potentially bringing its multiple closer to that of the S&P 500. Such a re-rating would mean further upside for the stock, even without any increase in expected earnings.

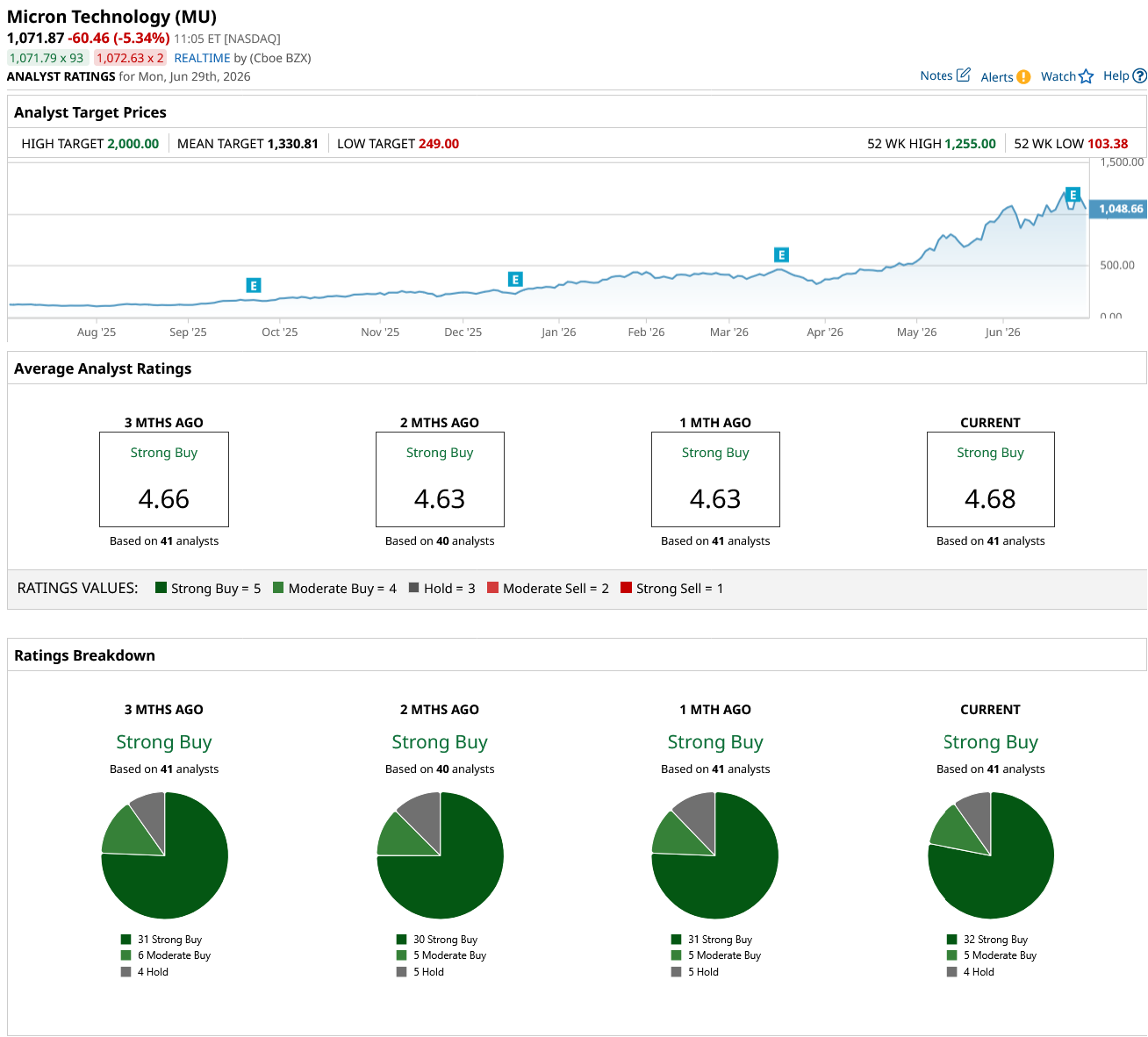

What Do Analysts Expect For MU Stock?

Wall Street analysts are highly bullish on MU stock, as reflected in its consensus “Strong Buy” rating. Of the 41 analysts covering the stock, 32 rate it a “Strong Buy,” five recommend “Moderate Buy,” and four have “Hold” ratings. The mean price target for MU stands at $1,330.81, suggesting there is still solid upside potential despite its strong YTD rally.

Following Micron’s blockbuster earnings report, multiple analysts sharply raised their price targets on MU stock. DA Davidson analyst Gil Luria said, “We posit that Micron has entered an era where it has some of the semi industry’s best visibility, a far cry from its historical role in the semi market,” while raising his price target on the stock to $2,000 from $1,500. Melius Research was even more aggressive, doubling its price target on MU stock to $2,200 from $1,100.

Meanwhile, 35 of the 42 analysts tracked by FactSet sharply raised their earnings forecasts for Micron following its blowout results, essentially confirming that the stock’s rally is rooted in improving fundamentals. The consensus EPS estimate for the next fiscal year beginning in September 2026 now stands at $148.79, up from $101.74 just one month ago.

Conclusion

Putting it all together, I think MU stock has more room to run, particularly if the company continues to strike long-term supply agreements, which could ultimately lead to a valuation re-rating. With that, I believe investors who already own MU should continue holding it, at least through the remainder of the year. At the same time, I acknowledge that the stock could face near-term volatility, as investors have become increasingly sensitive to AI-related headlines. Late last week, the chip sector came under pressure after price hikes across products from Apple (AAPL) and Microsoft (MSFT) fueled concerns that higher costs could weaken future demand for chips and eventually slow the chip rally.

The upcoming second-quarter earnings season should provide some answers, but based on Micron’s blowout results, I don’t believe MU investors have much reason to worry.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)