/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

There's always a strange nervousness that comes with trying to price a company that no one doubts anymore. Unlike those messy, “misunderstood” names that are easy to dig into, a company everyone already likes gives you almost nothing to push back against… except for maybe some far-fetched speculation. And that's exactly why it's the process of digging into those messy names where investors usually find their edge.

I'm not talking about those speculative artificial intelligence (AI) infrastructure bets that are clearly overvalued, but those well-established names with the deepest pockets that even the most conservative investors pour money into.

With those companies, the bright future has already been imagined for you by everyone else in the room, and it's already baked into the stock price. And that is where many investors fall into an unintended trap.

That's because when the whole world believes, doubting it feels like being a silly contrarian. Following the herd just feels safer, which is exactly backward. After all, a great company and a great investment are two entirely different things, and more often than not, the gap between them is the cost of entry.

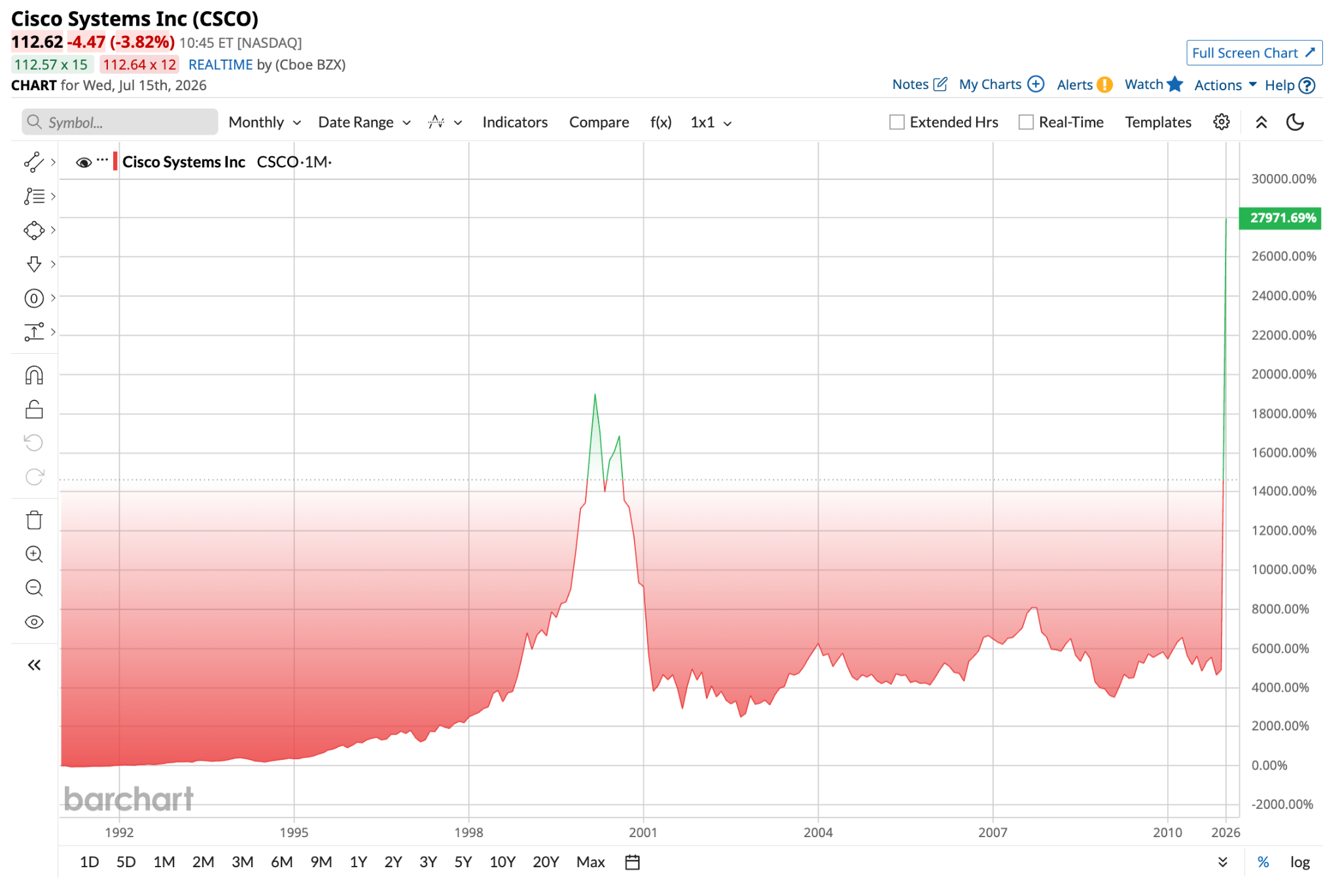

Don't believe me? Ask anyone who bought Cisco (CSCO) at its 2000 peak.

The business did everything right for the next 25 years, and the stock still needed every one of those years just to get investors back to even. A generation of gains, gone – and not because the company failed, but because the price already assumed perfection.

So, today's piece is all about how I value stocks the market is already in love with, a.k.a. the Wall Street darlings. Specifically, I'm looking at the current Magnificent 7 - I say "current" because we all know they're only magnificent until they're not.

Why are beloved stocks the hardest to value?

In the markets, love is the hardest thing to price in because it already paid up for the future. But the harsh truth is that even companies with flawless execution might still hand us nothing better than an average return. That's because the growth opportunity we're paying for was already promised.

And usually, the disappointment doesn't even look like a failure when it comes. In most cases, it looks like success that simply matched what the price was already counting on, and history has a way of repeating itself almost word for word.

Let me give you another example. Back in the early 1970s, an informal group of stocks nicknamed the Nifty Fifty was treated as a forever holding. The investors' thinking was that you would buy them, never sell them, and that the quality made "any price" worth it. That felt smart because it wasn't wrong about the businesses themselves.

Any of this sound familiar to you?

Anyway, by 1972, the average Nifty Fifty stock had pushed past a price/earnings (P/E) ratio of 41, while the broader S&P 500 Index ($SPX) sat near 18x. Xerox (XRX) and Polaroid, for instance, carried multiples of roughly 46x and 91x, respectively, at their peaks.

Now, a quick explainer in case you're unfamiliar. The price-to-earnings (P/E) ratio is the stock price divided by the company's annual earnings per share. A higher number means investors are paying more for each dollar of earnings. Take Polaroid's 91x figure from above: that means investors were paying $91 for every $1 of Polaroid's annual profit.

Going back, the excitement around the Nifty Fifty wasn't driven by companies dressing up to look strong. That group consisted of many of the best businesses in the United States, and for that reason, the illusion of safety was the biggest risk. The quality convinced investors that the price didn't matter in the first place.

So what happened to them? Well, the stock market meltdown of 1973 and 1974 hit the Nifty Fifty harder than the broader market. And of course, the priciest names on the list fell the furthest.

Yet, most were still genuinely great businesses, so the survivors eventually grew into their prices. But that left long-term holders waiting out a rather long stretch just to break even. Better than a permanent loss, sure, but not ideal for long-term investing.

So, where does all that lead us?

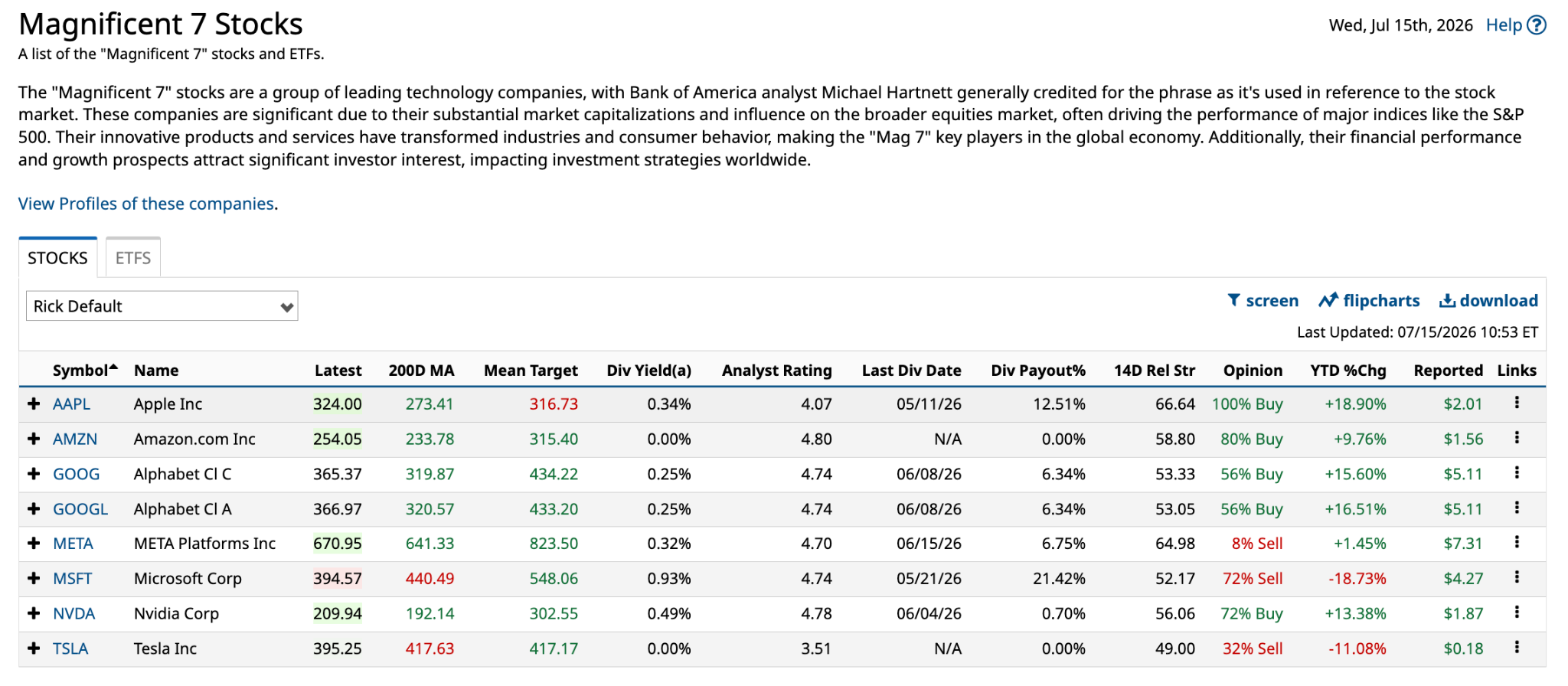

Today, the Magnificent 7 – NVIDIA (NVDA), Microsoft (MSFT), Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and Tesla (TSLA) – appear to be today's version of the Nifty Fifty.

Fifty years later, is history repeating itself – and just wearing flashier clothes filled with bits of gold from all of those AI chips? Well, don't run off with that comparison yet. To be clear, expensive is relative, and it doesn't automatically mean "bubble."

So let's take a look at the data. Based on their five-year average trailing P/E ratios, the Magnificent 7 traded at an average of approximately 57.6x earnings.

| Company | 5-Year Avg. Trailing P/E |

| Meta | 22.98x |

| Alphabet | 24.44x |

| Apple | 30.09x |

| Microsoft | 33.96x |

| Amazon | 43.93x* |

| Nvidia | 63.44x |

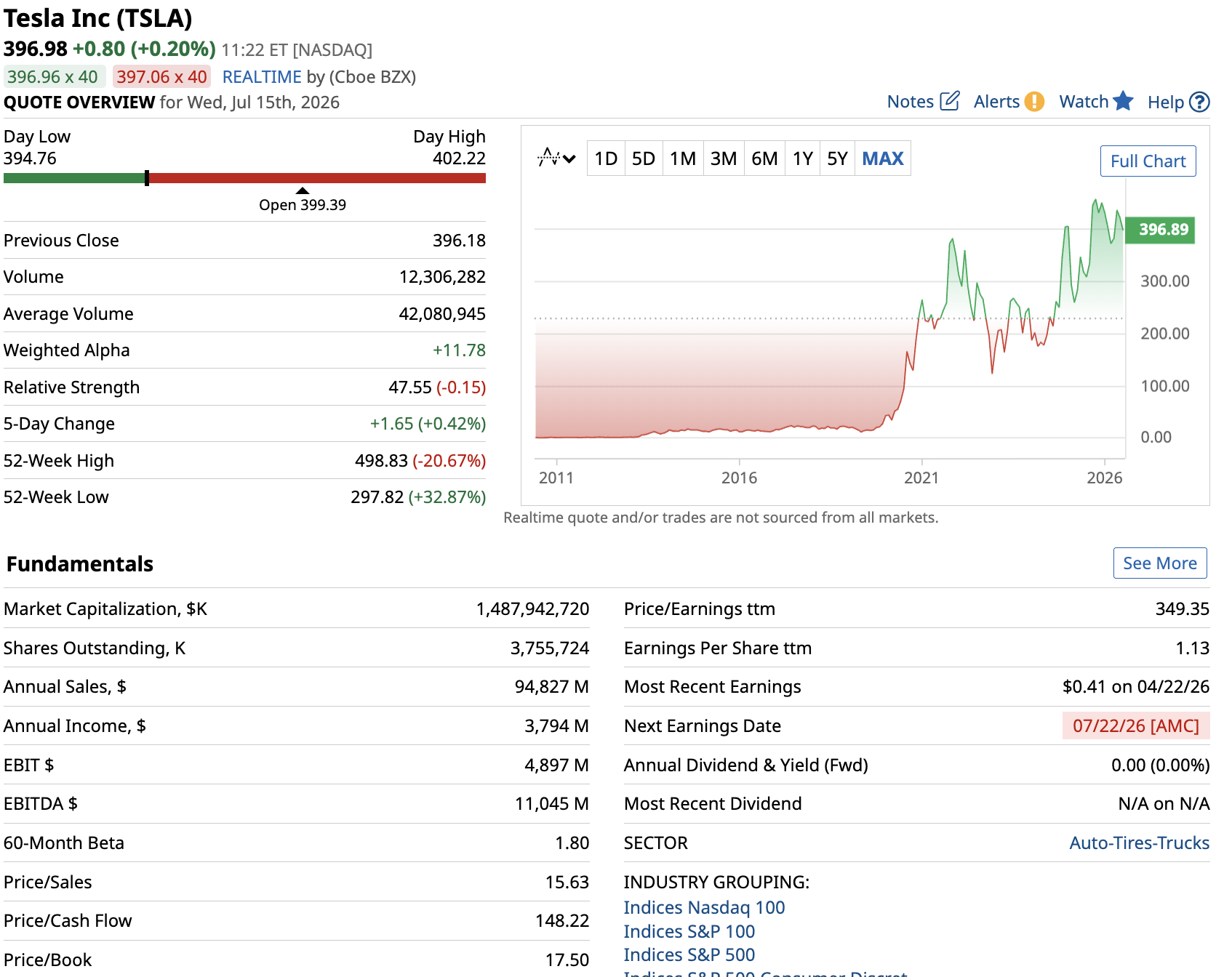

| Tesla | 184.46x |

| Average | 57.61x |

| Average (excluding Tesla) | 36.5x |

However, Tesla's five-year average trailing P/E of 184.46x is a massive outlier (not to mention its 349.35x ttm P/E) that heavily skews the group's average. And honestly, the valuation has never made sense to me, which is exactly why I've only owned the name for short periods over my trading career.

So, if we exclude Tesla, the group's five-year average trailing P/E falls to approximately 36.5x. The median, which is less affected by Tesla's extreme valuation, is 33.96x.

But even including Tesla and all its hype, the Magnificent Seven's average still sits below the roughly 66x forward earnings at which the seven largest companies by market value traded in 1999. Those were Microsoft, General Electric (GE), Cisco, Walmart (WMT), ExxonMobil (XOM), Intel (INTC), and Nippon Telegraph and Telephone.

To be fair, that 66x figure is a forward multiple, while the Magnificent 7 number above is trailing, so we should treat the comparison as directional rather than exact. But I think this distinction is important because it tells us that, despite everything that has happened in the stock market so far, the Magnificent 7 isn't priced at the peak of the dot-com years. It also warns us against the easy, and frankly lazy, habit of calling every Wall Street trend a bubble.

The point is that a premium can absolutely be justified. The question is whether it can be justified by fundamentals, and answering that requires methodology.

How to properly value expensive stocks

So how do you avoid buying the next Cisco at its peak? Or rather, how do we get it at a fair price?

Well, the thing to let go of right away is the idea of a perfect number, because valuation is a search for a reasonable range. The way Benjamin Graham framed it, this is an art more than a science, and the margin of safety is the cushion that saves us when that art turns out to be wrong.

That cushion is basically the discount, or the gap between what investors pay and what the business is honestly worth.

In fact, plenty of value investors won't touch a stock without a margin of safety of at least 30%, and they're happy to wait, sometimes even years, when the discount is thinner than that.

Now, if we point that standard at a beloved stock, the problem jumps right out, because consensus optimism and a discount don't live together. Optimism eats the discount. Can you see it now?

The very admiration that makes a company feel "safe" is the very same thing that erases the factor that would actually make it safe.

Because of this, anyone targeting a 30% margin of safety from a stock everybody loves is going to spend most of the cycle holding cash or feeling left out. As a conservative investor myself, I know that feeling all too well, but that is the cost of discipline.

Now, the margin of safety tells us how much cushion we want, but it doesn't tell us what a business is actually worth in the first place. That job falls to the valuation metrics, but a few of the classic ones need a tune-up before you can apply them to a Wall Street darling.

The price-to-book ratio, for example, used to be a valuation gold standard. Price-to-book compares a company's market value to the value of everything on its balance sheet, including buildings, equipment, cash, and similar assets. It's easy enough to count all the company's belongings and frame it into how much it's valued.

But today, P/B has lost most of its meaning due to the modern, asset-light business models so many companies run on.

For an asset-light company that barely owns those kinds of things, most of its actual value lives in things you can't touch, like a software ecosystem, patents, its partners, the network of customers who keep coming back, or even the branding itself.

An asset-light business often carries a relatively high price-to-book ratio almost by default, and that's where much value commentary trips over its own feet, because it reads that inherently high ratio as “proof” that the stock is overpriced. The real reason is that P/B was designed for manufacturers and other industrial firms that were dominant before the advent of computers.

Apple, for example, has a 5-year average price-to-book ratio of 48x, which is miles above the generally accepted P/B level of 1.0.

And before we argue that Apple is a manufacturing business, consider that it outsources a substantial share of its production through third-party partners such as Foxconn parent Hon Hai Precision Industry and other suppliers, so it owns relatively little of the physical production capacity behind its products.

So, considering that, the margin of safety for an asset-light business has to be built around durability and competitive edges instead of whatever is on the books.

And that is where the PEG ratio earns its keep. For starters, PEG takes the P/E ratio and divides it by the company's growth rate, then ties the price investors are paying to the growth that's supposed to justify it. So, a PEG near 1x means the premium and the growth roughly match up.

A PEG well above 1x means you're paying for growth the company hasn't actually proven it can deliver yet. That said, it's a blunt valuation metric, and I would never lean on PEG ratios alone. However, it's pretty good at making the premium defend itself.

Graham also left behind another methodology that aged really, really well: comparing a stock's earnings yield to bond yields.

The core idea is that a stock's earnings-to-price ratio should be at least as high as the yield you'd get on safe, high-grade bonds. To get that number, just flip the P/E formula to earnings over price, or one divided by the P/E ratio.

What keeps this valuation method useful at all times is that it's really a test of opportunity cost, and it resets itself as interest rates move.

Put simply, when bonds pay next to nothing, a higher P/E is easier to justify. But when bond yields climb, that same high multiple suddenly looks expensive, even though the company hasn't really changed.

It's a widely known principle, but investors tend to forget it during long stretches of cheap money – only to be harshly reminded later.

What happens when you pay for perfection?

A stock is priced for perfection when the market assumes flawless execution forever. There's no room for a stumble, and even genuinely good results can come across as disappointing simply because the price quietly demands higher figures. I think the most relatable example in modern history belongs to Cisco Systems.

Back in March 2000, Cisco's P/E ratio peaked at a whopping 200x. And from the start of 1999 to that peak, Cisco shares jumped over 230%.

That bull run lifted the company's market value to around $555 billion and briefly made Cisco the most valuable company on Earth. It was practically the NVIDIA of its time.

But that run was driven by Cisco's perfect market position. The company's networking gear ran the internet, and the internet was about to change the world. Both halves of that statement turned out to be true, and yet Cisco became a cautionary tale.

How, you ask?

Through the late 1990s, telecom carriers, dot-com startups, and many other enterprises were in a frenzy buying networking gear, with much of it funded by easy capital. All of that money was appearing on Cisco's balance sheets, and investors were singing the company's praises.

But when the bubble popped and funding dried up, those very same customers slashed spending or went bankrupt, and demand for Cisco's networking gear fell off a cliff.

And yet, through all of that, Cisco seemingly did everything right. After the catastrophe that slowed the biggest companies and sank the rest, Cisco remained a market leader, returned to profitability, and continued growing over the long term.

Still, the stock took about 25 years to crawl back to its 2000 high, and it has since pulled well past that old peak, fueled in no small part by the same AI infrastructure demand now propping up the Magnificent 7.

That's a whole generation of gains, gone. All that time and patience, just to get back to even.

That's what happens when investors pay for perfection.

A great company can still be a lousy investment if you buy it at the wrong price at the wrong time. Once the perfect expectations are out of the picture, the stock has to spend years growing into a valuation it never should've worn.

How do the Magnificent 7 stack up against each other?

Let’s go back to valuing a stock, or group of stocks, that everyone loves.

For this task, I prefer to look at historical P/E, P/B ratio, PEG ratio, and whether a stock's five-year earnings yield beats the Moody's Seasoned Aaa Corporate Bond Yield.

I picked this bond benchmark because Graham's whole idea is to measure the stock's earnings yield against something safe, something almost risk-free. If the stock’s earnings yield beats the risk-free asset, it’s worth looking at.

A stock's earnings yield is simply its historical P/E ratio flipped upside down, so you just divide 1 by the stock's P/E ratio. This shows how much profit the company earns per dollar you invest, which is why it's comparable to a bond yield.

And with everything I've gathered so far, here's how the Magnificent 7 stacks up based on historical data:

| Company | 5-Year Avg. Trailing P/E | 5-Year Avg. Earnings Yield | 5-Year Avg. P/B | 5-Year Avg. PEG | Beats 5.52% Current Aaa Bond Yield? |

| Meta | 22.98 | 4.61% | 6.32 | 1.96 | No |

| Alphabet | 24.44 | 4.16% | 6.91 | 1.34 | No |

| Microsoft | 33.96 | 2.99% | 12.26 | 2.43 | No |

| Nvidia | 63.44 | 1.83% | 30.45 | 1.34 | No |

| Amazon | 43.93* | 1.51% | 8.03 | 2.09 | No |

| Apple | 30.09 | 3.41% | 48.01 | 2.67 | No |

| Tesla | 184.46 | 1.18% | 19.17 | 5.92 | No |

*Note: Amazon's net loss in 2022 is not included in the calculation. Further, the 5.52% bond yield I used to compare is the Moody's Seasoned Aaa Corporate Bond Yield, current as of June 2026, not a five-year average.

Now, if Graham had used earnings yield alone to value the Magnificent Seven against today's 5.52% Aaa yield, he would have passed on every single one of them. And that's the uncomfortable part: it's the exact same verdict he would have handed Cisco in 2000, a business priced so flawlessly that it left no room for anything but perfection.

So, the natural next question becomes: which name is actually the cheapest?

Historically, Meta was the clear, all-around five-year winner. It came closest to clearing the bond-yield bar, though even its 4.61% earnings yield falls short of today's 5.52% Aaa yield. It also carried the lowest five-year average trailing P/E and P/B ratio.

There were also two notable extremes that round out the picture. Apple looks expensive on valuation metrics, while Tesla is in a universe of its own.

What to do when you love the stock, but the price scares you?

Let’s say you strongly believe in a beloved company for the long run – but at today's price, there's no margin of safety. Buying now might feel reckless, but staying out entirely also feels like walking away from a sure thing.

Well, it might not be for every investor, but options trading exists to live in the space between those two extremes, and it lets investors express a nuanced view instead of a binary “yes” or “no” vote.

I won't dig too much into options trading in this piece as I think it’s outside the scope, but I do believe it's worth mentioning, since expectations and speculation around the Magnificent 7 can easily trap investors, and we also don't want to miss the opportunity.

The cash-secured put can be very handy for great companies that might look too expensive at present. If you sell a put with a strike price below the current price, say 15% lower, you get paid a premium to wait.

In exchange, you take on the duty of buying the stock if it drops to the price you prefer. The key here, however, is that you should only sell cash-secured puts on stocks you truly want to own.

Or, if you already own 100 shares of a beloved company, you can write covered calls against them. It brings you income and lets you set a sell price you can live with (at the cost of capping your own upside, of course).

Now, for those who buy the story but refuse to overpay outright, a long-dated call can be a good option. These are often called LEAPS, and your downside is limited to the premium you paid, which is pretty compelling when a company you believe in is currently priced for perfection.

And of course, for investors holding a winner that's already delivered its most parabolic rally, protective puts can serve as insurance against Cisco-like events where years, even decades, are lost. You can use puts to hedge your position instead of abandoning it outright.

Final thoughts

A great company isn't automatically a great investment. The market can be right about a company, and you can still lose money if you buy at the top and it takes the stock a generation just to break even again.

So, maybe treat consensus optimism as a starting point for your own valuation model. The goal of understanding how much a company is worth isn’t to avoid great companies, but to avoid overpaying for them.

In short, believe in the business, but always respect the price.

On the date of publication, Rick Orford had a position in: AAPL , GOOGL , META , MSFT , AMZN . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.