/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

You read about it everywhere.

AI platforms. AI data centers. AI chips.

I bet some of you have even seen ads for AI toasters.

And the funny thing is, the artificial intelligence (AI) theme seems to be working well for the market. The S&P 500 Index ($SPX) broke past 7,000 months ago and is now halfway towards 8,000. NVIDIA's (NVDA) market cap, standing at the forefront of the AI buildout, is now about $5 trillion. Investors are reporting triple-digit gains in AI and AI-adjacent sectors such as power, construction, and semiconductors, across both established and speculative companies.

Everything is trending up. Everything is hitting new highs. Everyone’s making money.

But I can’t help but be reminded of another time when the market looked like this.

Specifically, back in 2000, before the dot-com bubble burst and sent the stock market into a freefall that it took years to recover from.

And I’m not the only one. Legendary investor Michael Burry, Bridgewater Associates Founder Ray Dalio, and OpenAI CEO Sam Altman have raised concerns in one form or another about the AI “hype.”

Their messages boil down to this single point: the AI market is overextended, and we are in for a painful reality check soon.

But are we, really?

What are the similarities between now and the dot-com bubble? What are the differences?

And if there really is a bubble… when is it going to burst?

What is a market “bubble”?

First, let’s clear up some definitions.

A market bubble is a period in which the price of an asset or group of assets rises far above its fundamental value, driven primarily by investor speculation and optimism rather than by underlying financial performance.

And at a certain point, when optimism can no longer drive further growth, the bubble bursts, typically resulting in a sharp, fast decline in asset prices.

As the old saying goes, the fundamentals always catch up.

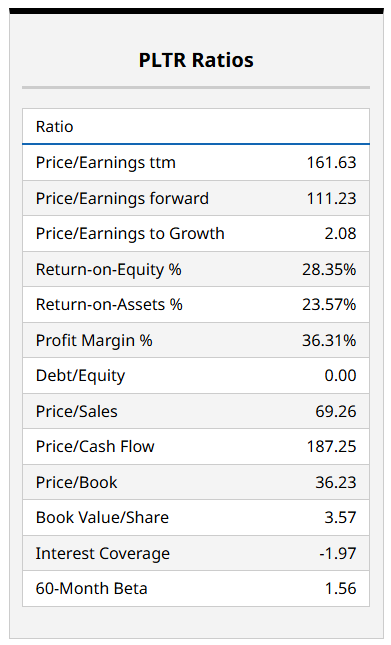

My favorite mini-example of this concept is Palantir (PLTR).

Back when I was covering it last year during its bull run, its price-to-earnings (P/E) ratio reached as high as 1,000, and its stock price was near $200. Quarter after quarter, the company reported revenue growth, improved profitability, and an increasing number of real-world applications for its AI platform.

But that was last year.

These days, Palantir is trading at $132, having fallen from an all-time high of $207.52. Its forward P/E ratio is around 111.

It’s still valued significantly higher than your typical tech company, but at least it’s more reasonable than those earlier valuation extremes.

The takeaway here is not that Palantir is a bad investment. I still think it’s an excellent business from a money-making standpoint. The problem is that, sometimes, stock prices rise much faster than the companies themselves can grow.

On that point, companies will be trapped in a vicious cycle: either catch up with ever-growing market expectations; or wait for reality to drag them back down so their valuations match their fundamentals.

When the latter scenario plays out, investors who weren’t able to run to the exits fast enough get the short end of the stick.

What happens to your money when a market bubble bursts?

So what actually happens to your money when a bubble bursts?

Well, first of all, it doesn't just disappear. A falling stock price simply means investors are no longer willing to pay the same price they were before. As expectations come back down to earth, valuations compress, and that's reflected in the share price.

If you bought near the top, that would translate into substantial paper losses. But if you never sell, those losses remain unrealized. Whether you eventually recover depends largely on the quality of the business you own.

Companies with strong fundamentals, growing earnings, and durable competitive advantages often recover over time. Some tech companies even surpassed their dot-com highs recently, but it took over two decades to do so.

Other companies went bankrupt. And when that happens, stockholders who failed to sell their shares on the market before the company collapsed often end up selling for pennies on the dollar. That’s because common stockholders are the last in line to get paid in the event of a bankruptcy.

Of course, nobody wants to see their investments vanish into thin air. That’s why so many investors are hyper-aware of any talk about “AI bubbles.”

Why some say we’re in an AI bubble today

But where are those concerns coming from? Why is there a persistent claim that we’re in an AI bubble today? Here are the top reasons why.

Pro Bubble #1. Current valuations are too high

Today, valuation is one of the biggest pieces of evidence that we are in an AI bubble. Or at least, that’s what pro-bubble proponents say.

Over the past few years, investors have poured hundreds of billions of dollars into any stock, sector, or startup with an AI story, driving many companies to trade at earnings multiples well above historical norms. In some cases, these valuations imply years of near-perfect execution and extraordinary growth, leaving very little room for disappointment.

During the dot-com bubble, valuation excesses were evident in both market-level data and individual company multiples. Back then, renowned economist Robert Shiller’s historical data showed the broader market’s cyclically adjusted P/E ratio reaching the mid-40s, while S&P 500 P/E data also showed valuations well above long-term norms.

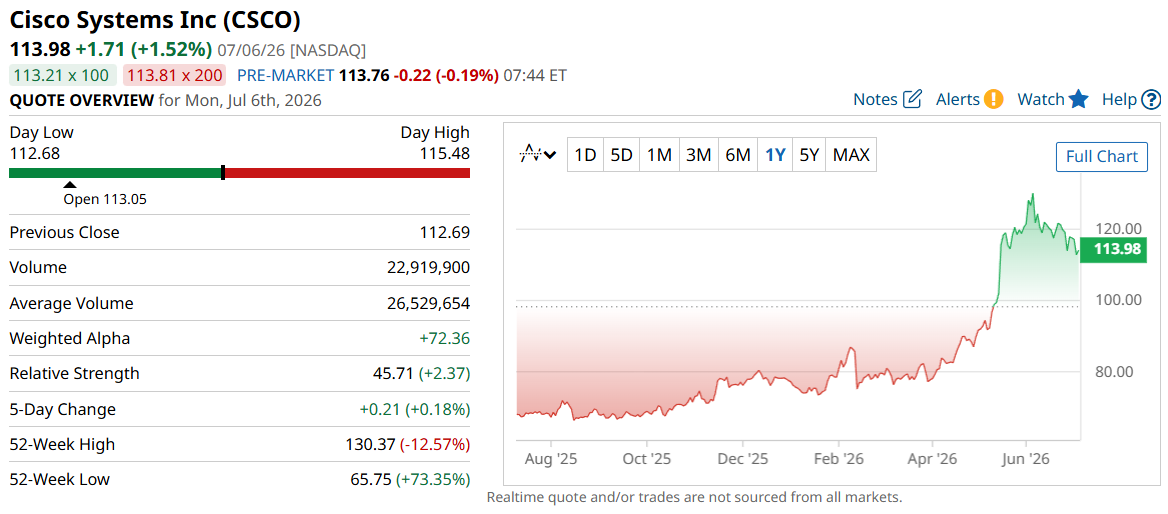

Those are the broad strokes. If we go down to individual company levels, Cisco (CSCO), which was positioned as the “picks-and-shovels” play during the dot-com era, traded at around 200x GAAP earnings before the crash.

But it gets even worse. Yahoo, the de facto internet leader and practically the Google (GOOGL) of its day, traded at over 1,400x earnings at the end of 1999.

Today, both of these companies still exist, but in vastly different forms.

Yahoo, which had the resources and opportunity to buy the fledgling Google back then, is now a small, privately held company that caters to sports, email, finance, and news services- basically a shadow of its former self.

On the other hand, Cisco has found its stride once again, exceeding its dot-com-era highs and reaching as high as $130 per share just a month ago.

Better yet, its valuations, while high, are nowhere near where they were back in the 90s.

Now, Cisco is an example of a survivor. But not every company was so fortunate.

For every Cisco, there were a dozen Pets.com, Webvan, eToys.com, Boo.com, Flooz.com, and much, much more.

Don’t recognize the names? I don’t blame you. That’s because they all sank during or after the dot-com bubble burst.

These companies were the purest examples of hype without fundamentals. Anything with “dot com” in its name was selling like hotcakes, even though their revenue was laughable, their cash flow statements were blood-red, and their business models ran on blind optimism or outright lies rather than an actual path to profitability.

Pro Bubble #2: 40% of the S&P 500 is just 10 companies

During the dot-com bubble, the 10 largest companies in the S&P 500 made up roughly 26% to 29% of the index. That meant 490 companies made up only around 70%-74% of the S&P 500’s total weight.

That was unusually concentrated by historical standards.

Today?

The top 10 make up nearly 40%.

Why is this a problem?

Well, simple. A handful of companies now account for nearly half of the index. So, the S&P 500’s performance no longer depends on how much the overall market moved but on how much the stocks of these 10 companies shifted.

Does this prove that we’re in an AI bubble? Of course not.

However, today we’re seeing an even greater concentration risk in the market than we did right before the dot-com bubble burst. The higher investors bid up those companies, the less room there is for disappointment. And when companies inevitably fail to meet lofty, often unrealistic expectations of a rabidly optimistic market, the downside can be… catastrophic.

Pro Bubble #3: Capex vs. revenue is an ongoing battle

There’s also concern about the growing spending on AI. We’ve seen stocks like Microsoft (MSFT) and Meta (META) take hits after announcing increases in capex due to data center and AI-related developments.

To give you a better idea of why, here’s a quick reference table of guided capex for some of the top hyperscalers in the market.

| Company | 2026 capex guide | Latest annual revenue | Capex as % of revenue | Latest annual net income |

| Microsoft | ~$190B | $281.72B | 67.4% | $101.83B |

| Meta | $125B to $145B | $200.97B | 62.2% to 72.2% | $60.46B |

| Amazon | ~$200B | $716.92B | 27.9% | $77.67B |

| Alphabet | $180B to $190B | $402.84B | 44.7% to 47.2% | $132.17B |

| Total | ~$695B to $725B | $1.60T | 43.4% to 45.2% | $372.13B |

The top companies in the world are spending a large chunk of their revenue on AI-related investments. Amazon (AMZN) may look like an outlier here, but that’s only because of its enormous but low-margin retail business. If we remove that and consider only the AWS segment, the comparison would be a $200 billion investment versus the latest annual revenue of $128.7 billion.

Remember, these investments are being made long before anyone knows how big the eventual payoff will be. Companies are spending hundreds of billions of dollars today in hopes that AI will generate even greater profits tomorrow.

Now, if the bet pays off, everyone’s happy. Elevated valuations today might appear justified tomorrow.

But if AI adoption falls short of everyone’s expectations, the market will start asking if the spending was all worth it, which could put pressure on the company’s stock.

Why we’re NOT in an AI bubble today

Of course, the story is much more complex than the risks. I admit that some factors might look strikingly similar, but the AI market differs from the dot-com boom in many important ways.

Here are a couple of them.

Anti Bubble #1: AI companies are actually making real money right now

One of the biggest issues during the dot-com bubble was that most companies didn’t even have a shred of hope of reporting meaningful revenue, much less a profitable quarter.

That’s not the case today.

The companies leading the AI race are among the most wildly profitable businesses in history. Microsoft, Alphabet, Meta, Amazon, and NVIDIA generate hundreds of billions of dollars in annual revenue and tens of billions in free cash flow, all while maintaining double-digit margins that, more often than not, exceed the tech sector and overall market average.

| Company | Net margin |

| Microsoft | 36.1% |

| Meta | 30.1% |

| Amazon | 10.8% |

| Alphabet | 32.8% |

| Apple | 26.9% |

| Nvidia | 55.6% |

| Broadcom | 36.2% |

| Total/weighted average | 27.3% |

Unlike many dot-com startups, they aren't relying on investor capital or hype to keep the lights on. They’re more than capable of keeping everything running. Heck, they can even buy the electric company that runs it all if they wanted to.

Overextended analogies aside, that doesn’t mean hyperscalers are immune to overvaluation. It just means that the debate shifts from “untenable market hype destined for an ugly, inevitable crash” to “overoptimistic investors pricing in years of near-perfect execution.”

Their continued performance also keeps forward P/E ratios in the market a bit more realistic than during the dot-com bubble.

Anti Bubble #2: Top experts say they don't see the evidence

Another point for the AI optimists is that not everyone agrees that we’re in a bubble.

JPMorgan Asset Management has said it does not currently believe AI is a bubble, citing many of the same reasons I outlined in the previous section. However, it does warn investors against chasing empty hype.

The brokerage also notes that “investors are scrutinizing individual company fundamentals rather than placing options on the overall market, which would be more common behaviour in the late-stage euphoria of a bubble forming.”

Fed Chair Jerome Powell has made a similar point, saying the AI boom differs from the dot-com era because today’s highly valued companies “actually have earnings,” while AI-related spending on data centers and chips is already contributing tangibly to economic growth.

So, while opinions differ on valuations, there's broad agreement on one point: AI is creating real businesses, generating real revenue, and driving tangible economic activity.

What should investors do today?

If you're worried about an AI bubble, does that mean you should sell everything, have a seat in the backyard over the summer with a nice cold drink, and wait for this all to blow over?

Not necessarily.

But investors shouldn’t be complacent, either.

The truth is, nobody really knows with 100% certainty if today’s AI leaders are fairly valued, overvalued, or in the middle of a pressurized bubble. Stocks are only as valuable as the market is willing to bear, and fair prices are much easier to eyeball in hindsight. Just ask investors who sold NVIDIA in 2021 because they thought the stock was “too expensive for a graphics card maker.” They’re probably kicking themselves for missing its historic run.

On the other hand, excessive optimism isn’t something you can take all the way to retirement. Not if you want to have money to spend in your golden years, anyway.

So, rather than perfectly timing the market, many investors can opt for caution. That can mean rebalancing oversized winners, avoiding leverage, trimming positions that have grown too large, and ensuring that no single theme dominates the entire portfolio.

You can focus on constructing a diversified portfolio built to withstand market volatility. I publish many articles on Barchart featuring some of the top dividend stocks in the market today. They’re generally not AI stocks – far from it, actually. Most of them operate in boring sectors such as consumer staples, utilities, and healthcare.

But that’s exactly the point. These businesses generate consistent cash flow regardless of whether AI spending accelerates or slows. Honestly, the only way I could see some of these companies going under because of AI is if Skynet goes online and wipes us all out.

So, yes. These companies may not double overnight. Or even in six months. Or a year, two years, three… You get the idea. But they’ve historically provided a measure of stability when high-growth sectors become volatile.

These are the exact reasons why I personally won't buy SpaceX (SPCX) stock, at least not at today’s valuation. Sure, the company has a compelling story and a massive following. But it doesn’t make money, and for a company of that size and caliber, the lack of profit is quite concerning.

Remember, steady compounding growth beats large and fast price swings because you don’t have to time your entries and exits. Plus, investors can reduce their own AI bubble risk without making an all-or-nothing call. Remember: rebalancing, trimming oversized positions, avoiding leverage, and ensuring no single theme dominates their portfolio are some good ways to do it.

There's also a middle ground for investors who remain bullish on AI over the long term, but would prefer less valuation risk. Rather than focusing solely on the companies building AI models, some are investing in the businesses that support the entire ecosystem.

I mean the power producers, electrical equipment manufacturers, grid infrastructure companies, cooling specialists – the smaller players that nonetheless play key roles in advancing the AI sector while still having business outside the boom.

When will the AI bubble pop?

Now, I know I laid out a pretty nuanced take on the status of the AI market. But, I completely understand if some of you get to this point and still ask:

“So… when will the AI bubble burst?”

That’s the million-dollar question – and, unfortunately, it's one that I can’t answer.

I have been in the market for as long as I can remember. I’ve made both good decisions and some spectacularly bad ones, and I’ve learned from all of them. But even I don’t have a crystal ball that can tell whether and when the AI market will reach bubble status and pop.

Honestly, anyone who tells you that they know exactly when it’ll happen is taking you for a ride. Or they’re more confident than they should be. Markets have a habit of staying optimistic longer than most investors expect, and even far longer than most can stay solvent.

A good example of that concept is Tesla (TSLA), the only member of the Magnificent 7 with a triple-digit P/E, shrinking profits, and declining market share in the EV industry. Compared with the other most valuable companies in the world, including AI latecomers like TSMC (TSM), Broadcom (AVGO), and Micron (MU), Tesla arguably has weaker fundamentals and a more fragmented AI growth narrative. And yet, the stock has remained expensive for years.

Why will the AI bubble pop?

In any case, instead of asking if we’re in an AI bubble, I think it would be more useful to ask what could make the AI market turn for the worse rather than when.

- The first thing I'd watch is the hyperscalers themselves. Right now, Microsoft, Alphabet, Amazon, and Meta continue to increase their AI spending because they're seeing enough demand to justify it. If one or more of these companies suddenly cut capital expenditure guidance or delayed data center projects, that could be an early sign that expected returns aren't materializing.

- Second, watch the fundamentals. Revenue growth, cloud demand, AI adoption, and corporate spending all need to continue supporting today's lofty expectations. AI stocks are priced for exceptional performance. A few disappointing quarters could force investors to rethink those assumptions.

- Finally, keep an eye on the broader economy. If interest rates remain elevated, credit becomes tighter, or businesses begin pulling back on technology spending, speculative areas of the market - the smaller AI plays - are often the first to feel the pressure.

On the other hand, if enterprises continue to adopt AI at scale, productivity gains become more measurable, and today's massive investments translate into durable earnings growth, many of these valuations may prove more reasonable than they appear today.

At the end of the day, the basic tenets of responsible investing still apply. Don’t put all your eggs in one basket. Invest in businesses that you actually understand. And never risk more money than you can afford.

On the date of publication, Rick Orford had a position in: MSFT , GOOGL , META , AMZN . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)