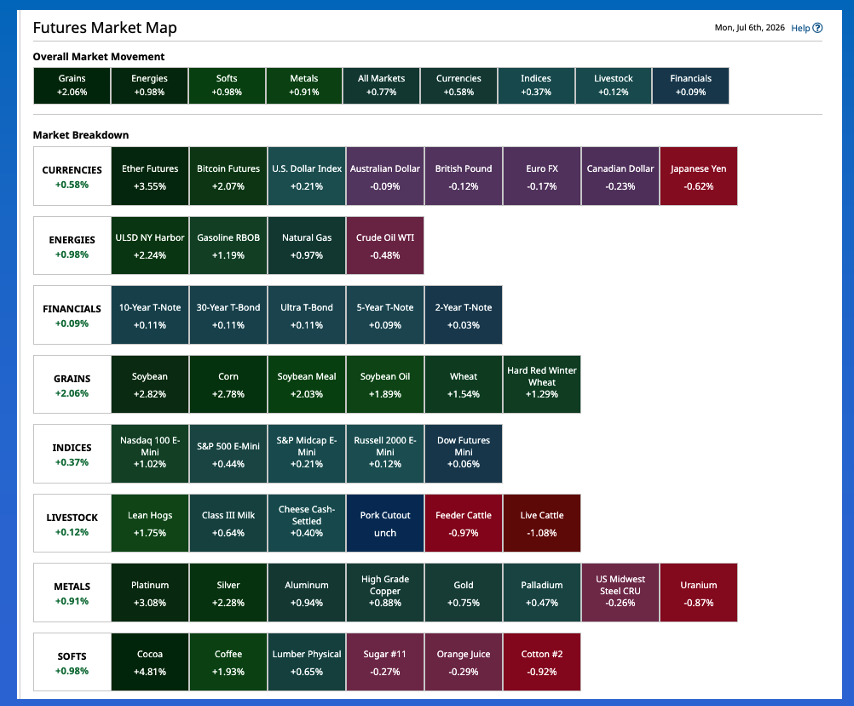

The commodity complex was showing gains across the board to start the week.

According to headlines, the Middle East took a backseat to Europe over the US 3-day holiday weekend.

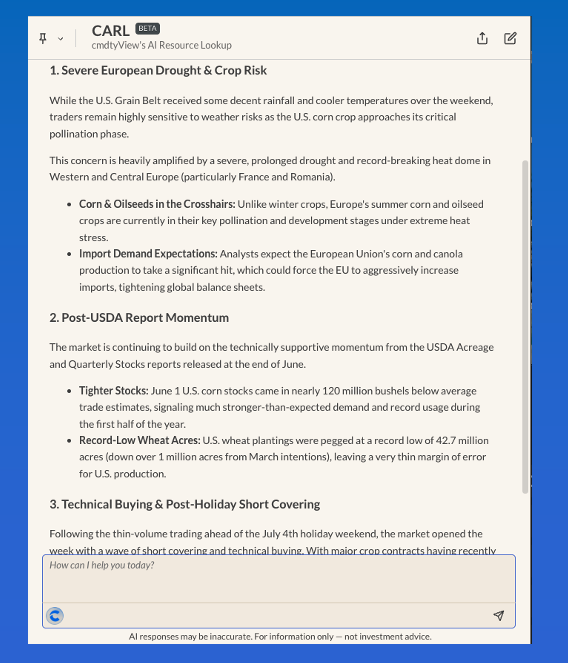

Barchart's AI analyst CARL also mentioned the “severe, prolonged drought and record breaking heat dome in Western and Central Eurpoe” as a key factor.

Morning Summary: It didn’t take long Sunday night to understand this was going to be another one of those weeks. A friend in the brokerage industry sent me a message last night – before the Grains sector opened – that read, “I’m not sure what the commercial view (of Grains) will be with the flooding in Iowa and the ‘extreme heat’ in the extended forecast for the US Midwest and Plains. Should make for an interesting week, as well as the Goldman Roll starting…”. He was spot-on, on all accounts. A look at the Barchart Futures Market Heat Map early Monday morning and the commodity complex is glowing green from one end to the other, led by the Grains sector. I’ll talk about this more in a moment. Softs followed at a distance with cocoa taking the reins this time around the clock on what looked to be fund short-covering. On the other hand, coffee continued its rally, the September issue (KCU26) up 8.75 cents (per pound), or 2.9%, at this writing on continued commercial strength. Recall from recent conversations coffee’s inverted (backwardated, for those of you from New York) forward curve continues to show a long-term bullish supply and demand situation. As for markets not trading overnight, it will be interesting to see what happens out in the Barn Monday.

Corn: The corn market was showing a double-digit gain to start the week. In the grand scheme of things, it isn’t overly surprising to see this type of activity in King Corn coming out of the US July 4 holiday. The September issue (ZCU26) rallied as much as 12.5 cents through Monday’s pre-dawn hours on trade volume of about 36,000 contracts and was one tick off its session high at this writing. The more heavily traded December issue (ZCZ26) was up 13.25 cents, also one tick off its high, while registering 55,000 contracts changing hands. I asked CARL (Barchart’s AI analyst) what sparked the rally in Grains, and it told me much the same thing as my friend. It’s interesting to note CARL acknowledged rains and cooler weather over key US growing areas this past weekend, putting the emphasis on the “severe, prolonged drought and record-breaking heat dome in Western and Central Europe”. Since we opened Pandora’s Box of “Europe”, my Blink reaction is the focus should be in the East where headlines talk of “Ukraine’s strikes and Russia’s barrage on Kyiv” putting markets on “alert”. That being said, crude oil was one of the few markets not in the green to start the week.

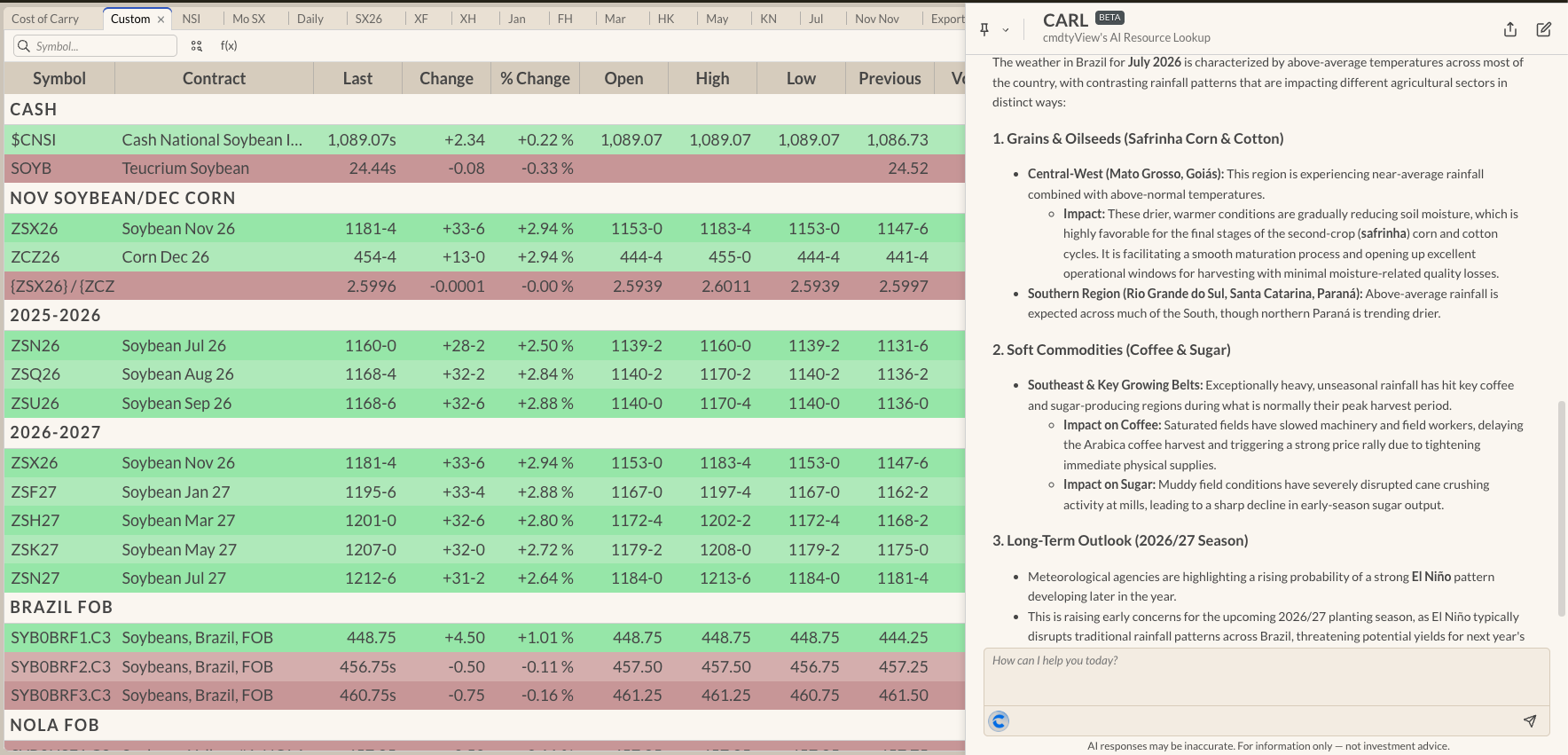

Soybeans: Meanwhile, the distillates (diesel fuel) market did rally overnight with the spot-month contract gaining as much as 10.6 cents (3.3%), sparking renewed buying interest in the oilseed sub-sector. November canola was up $13.10 (1.8%) at this writing while December soybean oil was sitting 1.25 cents (1.9%) in the green. Both pale in comparison to the overnight jump in soybeans, though, with the November issue (ZSX26) surging as much as 35.75 cents (3.1%) on trade volume of 60,000 contracts. My human analyst Blink reaction gave me two familiar possibilities: weather and renewed interest from the world’s largest buyer overnight. Again, weather across the US Midwest was mixed over the weekend, putting the spotlight on the extended forecast calling for more heat and less precipitation from Illinois west. But it is early July, and the old adage for the Northern Hemisphere is “soybeans are made in August”. South of the equator, it is the equivalent of early January up north, meaning the weather focus is more on coffee and sugar growing areas of Brazil. What about China, then? It’s possible the recent downturn in US prices could spark some new buying interest given supplies in China’s largest supplier (Brazil) may be tightening.

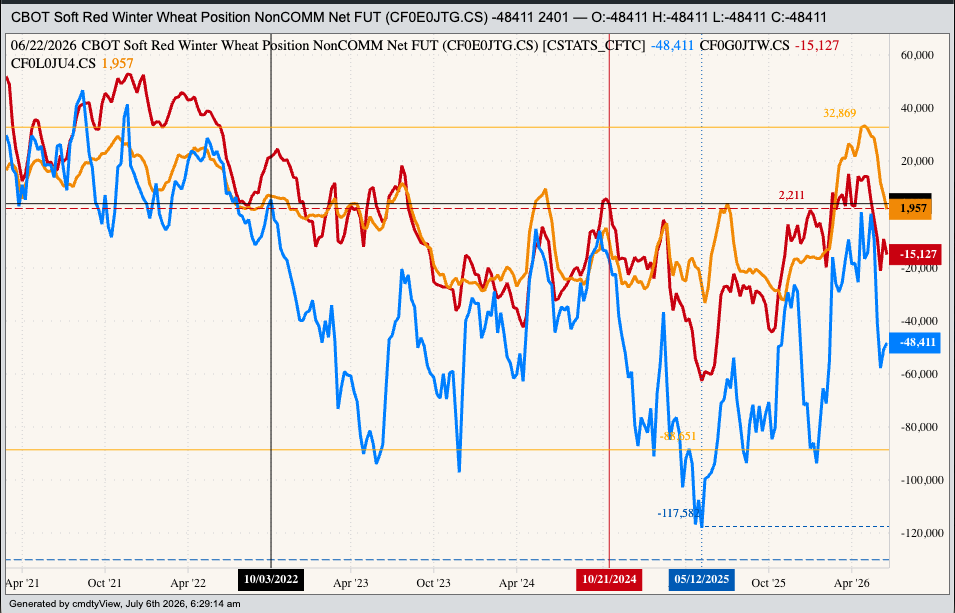

Wheat: The wheat sub-sector was not overlooked overnight, with all three markets in the green early Monday morning as well. As usual, most of the activity was in the SRW market where the September issue (ZWU26) rallied as much as 10.5 cents on trade volume approaching 10,000 contracts. If there is a link between weather problems in Central and Western Europe and US crops, it could be in the SRW wheat market. Recall from previous conversations the US is not going to be running out of SRW any time soon, but reduced production across Europe could lead to increased demand for US supplies. Last week saw a dramatic change in the September-December futures spread as it settled covering 60% calculated full commercial carry as compared to the previous week’s 74%. Similar activity was seen in both the December-March and March-May spreads. Additionally, the previous Commitments of Traders report showed Watson held net-short futures positions in both SRW and HRW opening the door to a round of short-covering support. As for national average basis (US), last week’s SRW calculation came in at 51.5 cents under September futures, as compared to the previous week’s 60.0 cents under and the previous 5-year average weekly close of 54.0 cents under September.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)