/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

Palantir Technologies (PLTR) has become one of Wall Street's biggest talking points this year as investors remain divided over its artificial intelligence (AI) prospects. Supporters argue the company has built one of the decade's most important AI businesses, backed by strong revenue growth, expanding profitability, and long-standing relationships with governments and enterprise customers.

However, critics believe enthusiasm has pushed the stock to a valuation requiring near-flawless execution. Despite that debate, DA Davidson analyst Gil Luria says Palantir holds competitive advantages few software companies can match, with AI further strengthening its position.

Investor optimism grew on Thursday, July 2, when Palantir’s shares rose 2.84% after DA Davidson upgraded the stock to “Buy” from “Neutral” and raised its price target to $175 from $165. Luria said recent developments in the AI industry highlight the growing need for software that can orchestrate multiple AI models, an area where Palantir already excels.

In addition, he cited tensions between Anthropic and the U.S. government, arguing they exposed the risks of relying on a single AI provider. Palantir's orchestration layer lets organizations switch between AI models with minimal disruption, improving flexibility and business continuity.

DA Davidson believes rising enterprise demand for reliable, adaptable AI orchestration software could further strengthen Palantir's long-term growth prospects.

About Palantir Stock

Headquartered in Aventura, Florida, Palantir develops software platforms that help government agencies and commercial organizations integrate, analyze, and operationalize complex data.

With a market cap of roughly $310 billion, the company offers four flagship products - Gotham, Foundry, Apollo, and the AI Platform - supporting defense operations, intelligence missions, enterprise workflows, and AI-driven decision-making across industries.

Despite its solid business foundation, PLTR stock has struggled this year, declining 1.14% over the last 52 weeks, falling 25.27% year-to-date (YTD), and losing another 2% in the past month.

The weakness stemmed largely from valuation concerns rather than operating performance, as investors questioned whether Palantir's premium pricing remained justified amid broader caution toward AI and software stocks.

Sentiment improved after Nvidia Corporation (NVDA) announced a new AI partnership with Palantir and the company secured a major U.S. Army contract, reinforcing confidence in demand. Meanwhile, Cathie Wood's ARK Innovation ETF (ARKK) bought the dip, while Wall Street analysts upgraded the stock, arguing the sell-off had become disconnected from fundamentals.

Shares subsequently rallied 17.62% over the last five trading sessions.

Even after the rebound, one question continues hanging over Palantir. Valuation remains the elephant in the room. The company still ranks among the most expensive names in the software sector.

Nevertheless, PLTR stock is currently trading at 87.60 times forward adjusted earnings and 40.16 times sales. Both multiples are well above industry averages, indicating that investors still pay a hefty premium for the company's growth.

Palantir Surpasses Q1 Earnings

Palantir strengthened investor confidence with its Q1 FY2026 results on May 4, once again surpassing Wall Street expectations. Revenue surged 84.7% year-over-year (YOY) to $1.63 billion, beating analysts' estimate of $1.54 billion, while adjusted EPS amounted to $0.33, topping the Street's forecast of $0.28.

Growth remained strong across both businesses, with U.S. commercial revenue climbing 133% to $595 million and U.S. government revenue rising 84% to $687 million. Profitability also improved as adjusted income from operations increased 151.7% YOY to $983.5 million, while adjusted free cash flow grew 149.6% to $924.6 million.

The balance sheet looked even healthier by quarter-end. Cash and cash equivalents climbed to $2.3 billion, up from $1.4 billion as of Dec. 31, 2025, giving the company an even stronger financial cushion.

Palantir also continued piling up large customer wins without taking its foot off the gas. During the quarter, the company closed 206 deals worth at least $1 million, including 72 above $5 million and 47 exceeding $10 million, lifting total closed contract value to $2.41 billion, up 61% YOY.

Management's outlook added another layer of confidence. For Q2 FY2026, the company expects revenue of $1.797 billion to $1.801 billion and adjusted income from operations of $1.063 billion to $1.067 billion.

The firm also raised its full-year guidance. Management now expects full-year 2026 revenue to reach between $7.650 billion and $7.662 billion. They also increased their U.S. commercial revenue forecast to more than $3.224 billion, representing growth of at least 120%.

Momentum is expected to carry on as analysts project Q2 FY2026 EPS to grow 107.7% YOY to $0.27. Expectations remain equally strong beyond this quarter. Analysts forecast full-year FY2026 EPS of $1.16, reflecting growth of 84.1% from the prior year. Looking one year further, they expect FY2027 EPS to climb another 40.5% to $1.63.

What Do Analysts Expect for Palantir Stock?

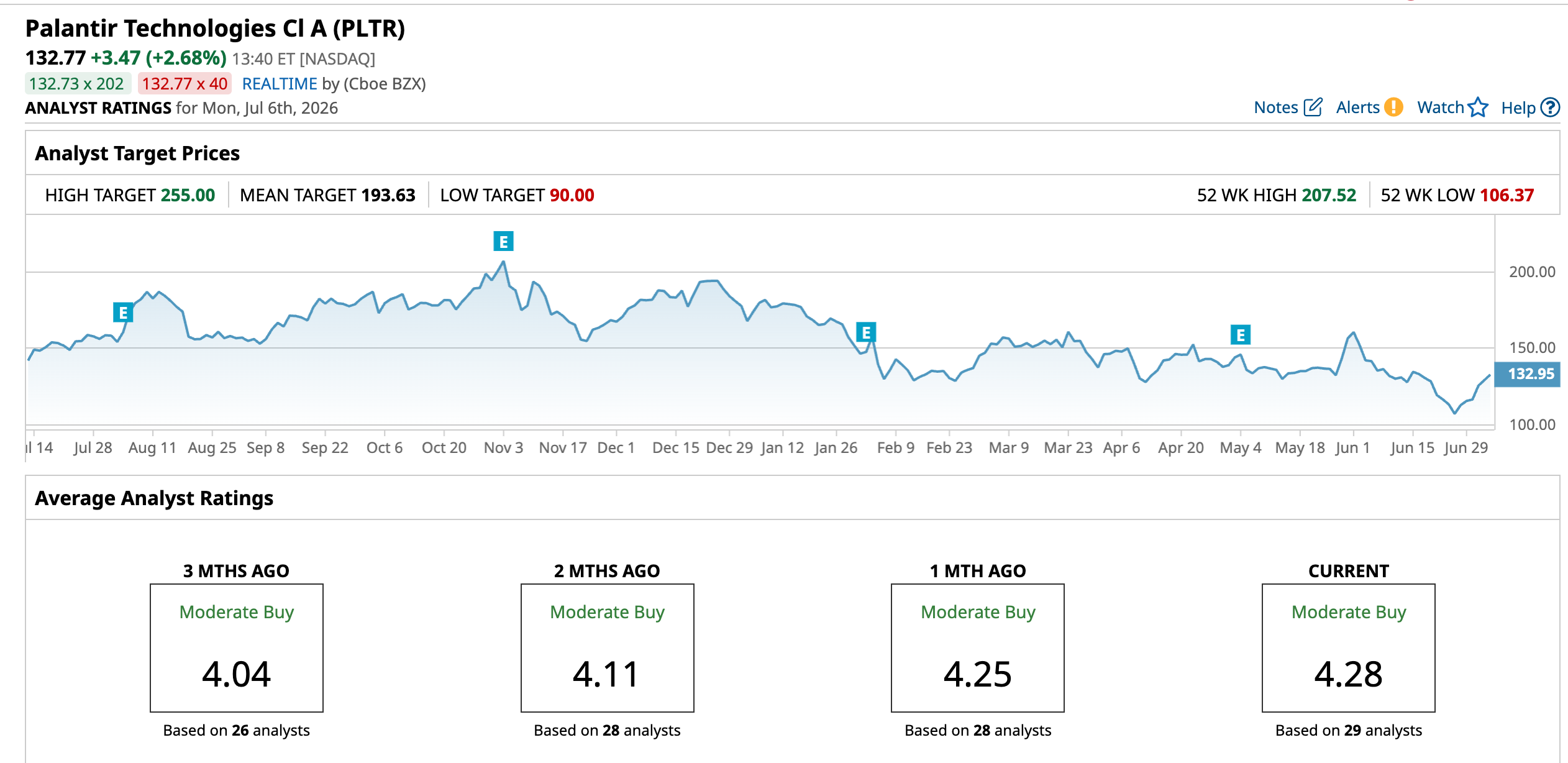

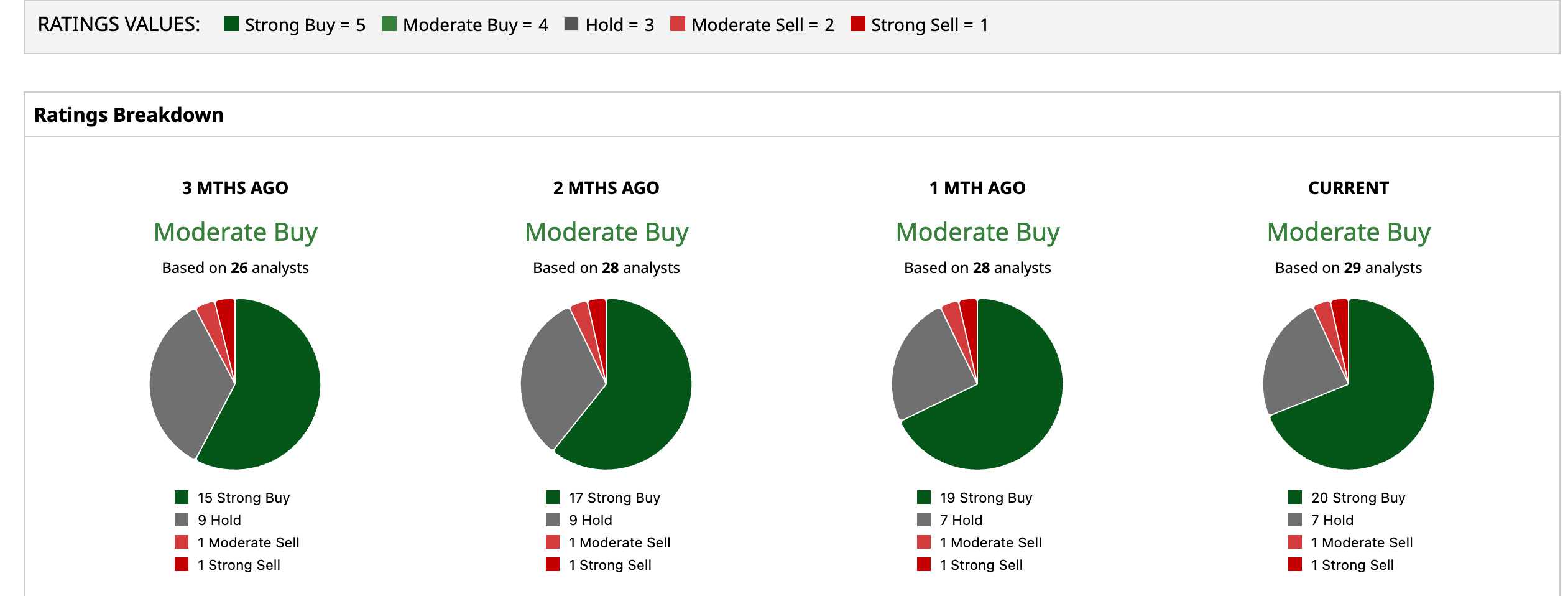

Strong earnings have certainly helped Palantir's case, although Wall Street still remains divided on just how much upside the stock has left after its massive run over the past few years. Even so, the overall rating still leans in the company's favor, as Wall Street has assigned Palantir a “Moderate Buy.”

Among 29 analysts currently covering the stock, 20 recommend “Strong Buy,” and seven prefer to stay on the sidelines with a “Hold” rating. One analyst has assigned a “Moderate Sell” rating, while another continues to recommend a “Strong Sell.”

Price targets also suggest many analysts believe the story has more chapters left to write. The average price target is $193.63, implying a potential 45.8% upside. Meanwhile, the Street-High target of $255 points to a 92.1% gain from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)