/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

After years of decline, Intel (INTC) has certainly staged a dramatic comeback. Under the leadership of CEO Lip-Bu Tan, investor confidence has steadily returned, fueled by meaningful investments to revive the company's foundry business, sweeping restructuring initiatives, early customer wins for its next-generation server processors, and strong government backing.

Together, these efforts have helped restore faith in a stock that had been steadily losing ground to the semiconductor industry's biggest players. Now, after delivering triple-digit gains so far in 2026, one Wall Street analyst believes Intel's rally may be far from over.

HSBC recently doubled its price target on Intel to $200 — the highest on Wall Street — while maintaining a "Buy" rating. The firm pointed to a stronger outlook for Intel's server CPU business and, for the first time, included the company's foundry operations in its valuation. Analyst Frank Lee said the foundry story is now "too good to ignore," arguing that Intel is emerging as a compelling alternative to Taiwan Semiconductor (TSM) (TSMC) as front-end fabrication and advanced packaging constraints continue to tighten across the industry.

With Intel already delivering huge gains in 2026 and HSBC setting a new high price target, let's take a closer look.

About Intel Stock

For decades, Intel has been one of the defining names in the global semiconductor industry. Founded in 1968 and headquartered in Santa Clara, California, the company built its reputation by designing and manufacturing the processors that power millions of personal computers and data centers worldwide. But today, Intel is much more than a PC chipmaker. Its business spans several high-growth markets, including client computing, data center and artificial intelligence (AI) processors, networking and edge computing, and Intel Foundry Services (IFS), its fast-growing contract semiconductor manufacturing business.

As AI and advanced computing redefine the semiconductor landscape, Intel is executing one of the industry's most ambitious transformations with the goal of becoming both a leading chip designer and a world-class semiconductor manufacturer. That transformation follows one of the most challenging periods in Intel's history. The company spent years grappling with slowing growth, shrinking margins, declining earnings, and eroding investor confidence as rivals like Nvidia (NVDA) and Advanced Micro Devices (AMD) pulled ahead in the AI race.

Yet Intel has staged a remarkable turnaround, and the numbers tell the story. With a market capitalization of approximately $554 billion, the chipmaker's shares have skyrocketed a massive 394% over the past year, vastly outperforming the S&P 500 Index's ($SPX) 20% gain. The momentum has continued in 2026, with INTC stock surging 214%, once again eclipsing the broader market over the same period. After climbing to a record high of $142.35 on June 30, the stock has since pulled back about 20% from that peak.

Inside Intel’s Q1 Earnings Report

Intel's improving financial performance is giving investors fresh reason to believe its turnaround is gaining momentum. On April 23, the chip giant delivered a blockbuster fiscal 2026 first-quarter earnings report, surpassing Wall Street's expectations on nearly every key metric and sending INTC stock soaring 24% in the following trading session. Revenue, gross margin, and EPS all exceeded the high end of management's own guidance, marking Intel's sixth consecutive quarter of outperforming its forecasts.

Intel reported non-GAAP revenue of $13.58 billion, up 7% year-over-year (YOY) and well ahead of analysts' consensus estimate of $12.39 billion. However, the biggest surprise came on the bottom line. Intel posted non-GAAP earnings of $0.29 per share, up a massive 123% YOY and crushing expectations of just $0.01. The impressive earnings beat was driven largely by aggressive cost-cutting initiatives and a more favorable mix of higher-margin products.

Even so, Intel's turnaround is far from complete. On a GAAP basis, the company still reported a net loss of $3.7 billion, primarily due to one-time charges tied to goodwill impairment and ongoing restructuring efforts. Despite those headwinds, several of Intel's core businesses delivered encouraging signs that the recovery is broadening.

One of the biggest bright spots was the Data Center and AI (DCAI) segment, where Intel is beginning to gain traction in AI-related workloads as demand for high-performance CPUs continues to climb. Revenue from the business surged 22% YOY to $5.1 billion. Meanwhile, the Client Computing Group (CCG), home to Intel's PC processor business, generated $7.7 billion in revenue, up a modest 1% YOY.

Intel's ambitious foundry business also continued to build momentum. Revenue at Intel Foundry rose 16% to $5.4 billion, highlighting growing demand for the company's semiconductor manufacturing capabilities. While the segment remained unprofitable, its operating loss narrowed to $2.4 billion, improving by $72 million sequentially as stronger yields across Intel 4, Intel 3, and Intel 18A supported gross margins.

Those gains were partially offset by higher operating expenses, as Intel deliberately ramped up investments in Intel 14A to support technology evaluations by both internal teams and prospective external customers. Looking ahead, investors will be closely watching Intel's upcoming Q2 earnings report, which is scheduled for release after the market closes on July 23.

Intel guided for Q2 revenue of $13.8 billion to $14.8 billion. The firm also expects a non-GAAP gross margin of approximately 39% as it continues balancing the high costs of expanding its manufacturing footprint with the profitable ramp-up of its next-generation AI and consumer-focused chips.

What Do Analysts Think About Intel Stock?

HSBC recently emerged as Intel's biggest bull, doubling its price target to $200 while reiterating a "Buy" rating. The firm believes Intel's improving server CPU business and rapidly evolving foundry operations could drive a multi-year earnings rebound. Analyst Frank Lee raised his 2026 server CPU shipment growth forecast from 20% to 25% and increased his 2027 projection from 20% to 30%, arguing that server CPUs will remain the primary engine of Intel's earnings growth.

The analyst's revenue forecasts for the DCAI business also sit well above the Wall Street consensus. Perhaps even more significant, HSBC included Intel's foundry business in its valuation for the first time, calling the opportunity "too good to ignore." Lee believes Intel is emerging as a credible alternative to TSMC as constraints in front-end fabrication and advanced packaging create opportunities for new manufacturing partners. He highlighted Intel's growing foundry customer base, including Tesla's (TSLA) Terafab and Apple (AAPL), and noted that the firm is actively engaging with Alphabet (GOOGL) and Nvidia. HSBC also pointed to Intel's Embedded Multi-die Interconnect Bridge (EMIB) advanced packaging tech as a potential competitive advantage.

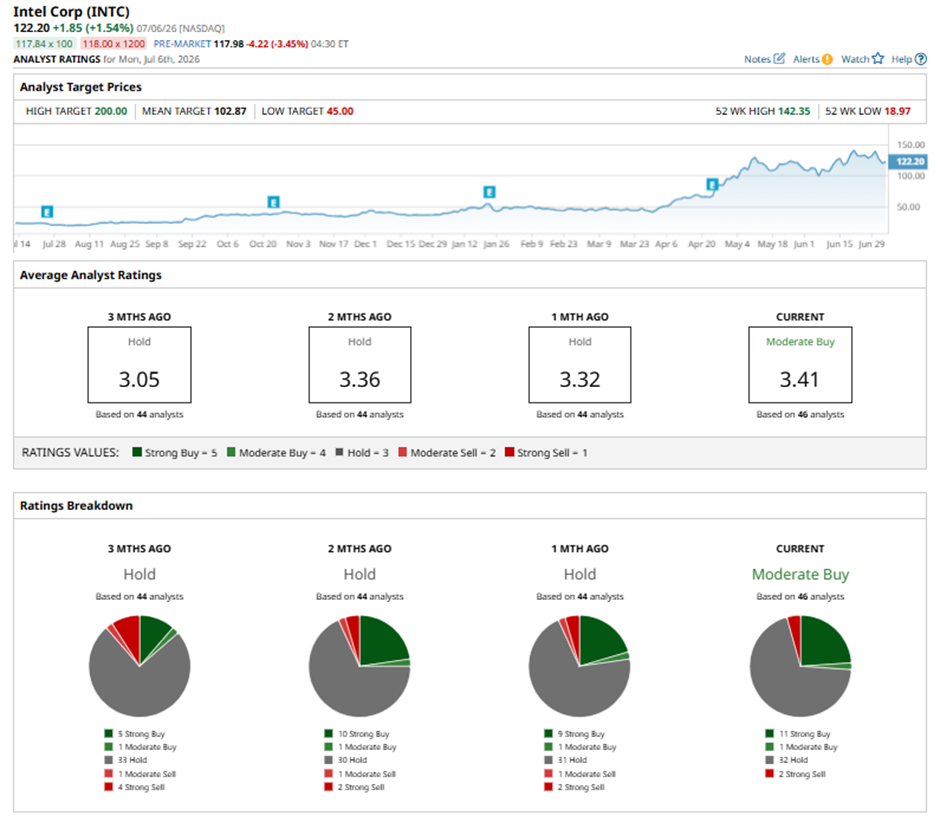

Wall Street remains broadly optimistic on Intel's long-term prospects, with INTC stock carrying a consensus "Moderate Buy" rating. Among the 46 analysts with coverage, 11 recommend a "Strong Buy," one has a "Moderate Buy," 32 analysts have a “Hold” rating, and just two maintain a "Strong Sell" rating. Although Intel has already surged beyond the average price target of $102.87, the Street-high target of $200 suggests the rally may be far from over. If this bullish outlook proves accurate, shares could climb another 78% from current levels, underscoring why Intel's turnaround story continues to gain traction among investors.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)