The S&P 500 ETF (SPY) closed 2025 at a dollar price of $682 per share. Last Friday, it closed at $747, up $65 and just shy of a 10% gain. That sounds like a great half-year for the stock market. It’s too bad that the entire gain came from less than 5% of the stocks.

Headlines routinely point to that most popular market benchmark, the S&P 500 Index ($SPX), coasting along in positive territory as proof that the broader U.S. economy has successfully navigated its way through various macroeconomic headwinds.

But if you look behind the capitalization-weighted curtain, the consensus narrative completely falls apart. The truth is that the headline average is serving as a grand optical illusion, masking a quiet, widespread erosion eating away at corporate America.

The Secret S&P 500 Storm

According to an analysis by Apollo Chief Economist Torsten Slok, a sharp divide has emerged beneath the surface of the market’s advance. The index’s gains this year have been driven almost entirely by artificial intelligence-related companies and energy stocks. When you strip out those two segments, the remaining stocks are actually in the red for 2026. Mr. Slok cited that more than 490 stocks have netted out to zero.

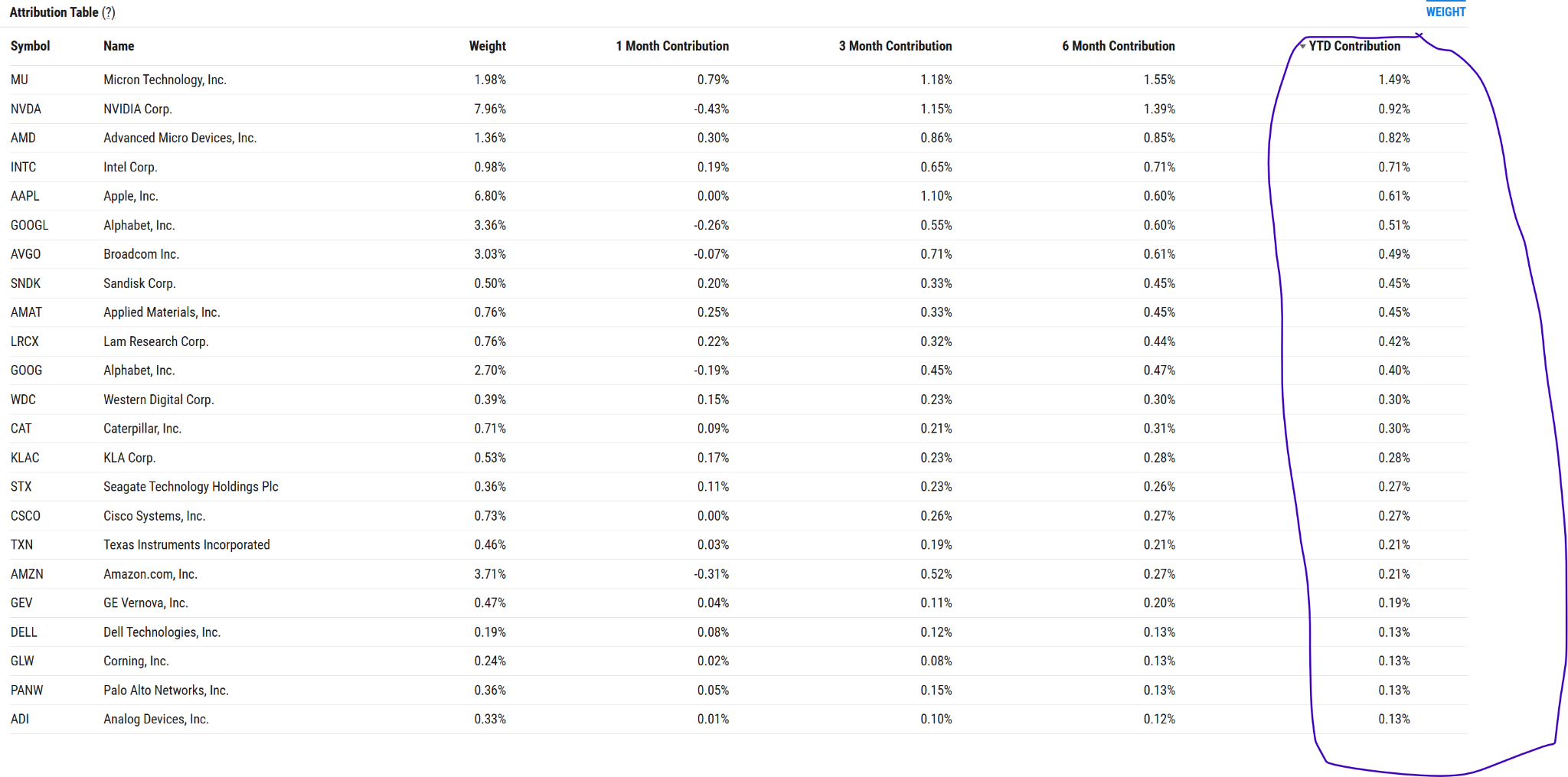

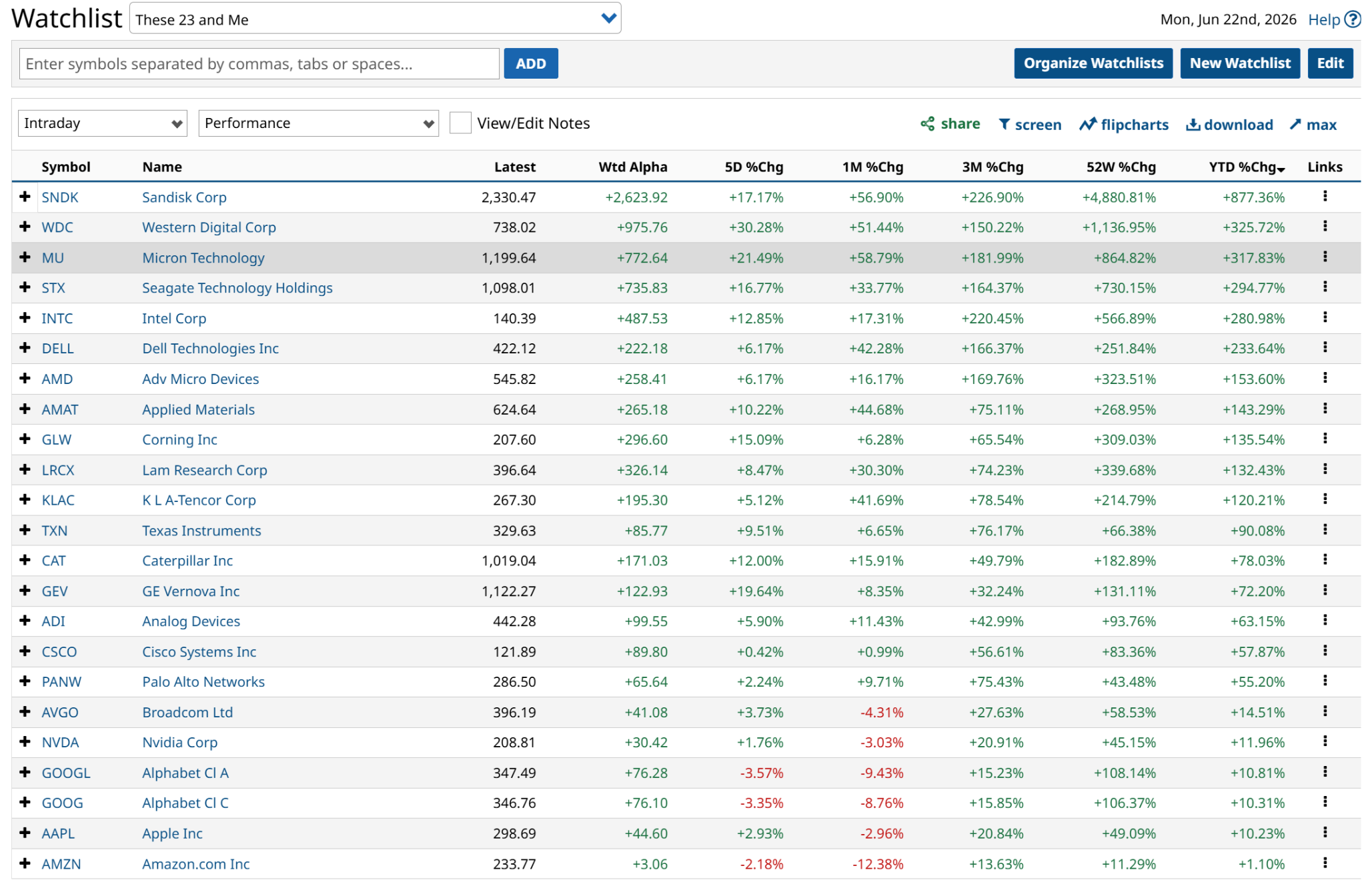

My analysis was a bit wider in that I found the 23 stocks above as the ones adding up to nearly a 10% gain so far this year. But either way, the key takeaway is the same:

Today’s stock market is a ghost town. From a distance, if you squint, it looks like a real city.

This extreme, lopsided divergence isn’t just an interesting statistical quirk. It is exactly the type of behavior you see right before a major, cyclical bear market takes hold.

The Historical Receipts of Narrow Breadth

History shows us that markets like this, which quietly send most stocks into retreat, typically mean that the market is reaching a point of terminal exhaustion. This specific fragmentation has preceded almost every major market crash of the last century:

1929

In the months leading up to the Great Crash, the broad market had already stopped rising. A massive public obsession with a tiny handful of speculative market leaders — like Radio Corporation of America (RCA) — kept the headline indexes afloat while the underlying credit markets and industrial sectors began to decay.

1972

This was the “Nifty Fifty” Peak. Right before the brutal 1973-1974 bear market, institutional capital concentrated heavily into a tight club of 50 “one-decision” growth stocks. As in, you only had to buy them and never sell them. One decision! While those 50 names pushed index averages higher, the bottom 80% of the market was already flat or negative, hollowed out by rising capital costs. Just like now.

2000

In late 1999, the average S&P 500 stock was underperforming a simple, risk-free Treasury bill. Capital was being moved en masse from traditional value businesses, manufacturing, and real assets just to feed the parabolic tech and dot-com mania. Just like now.

The index looked bulletproof right up until the exact microsecond the tech engine, starved of liquidity, dragged the entire unhedged passive market down with it.

A Lesson in Rhyming

To me, this isn’t about expecting the past to cut and paste itself onto 2026’s stock market. It is to remind us that the stock market is not what many think it is right now. And that risk management should be balanced with aggressive “to the moon” buying.

Here’s that list of the 23 stocks adding up to the 10% gain in the S&P 500:

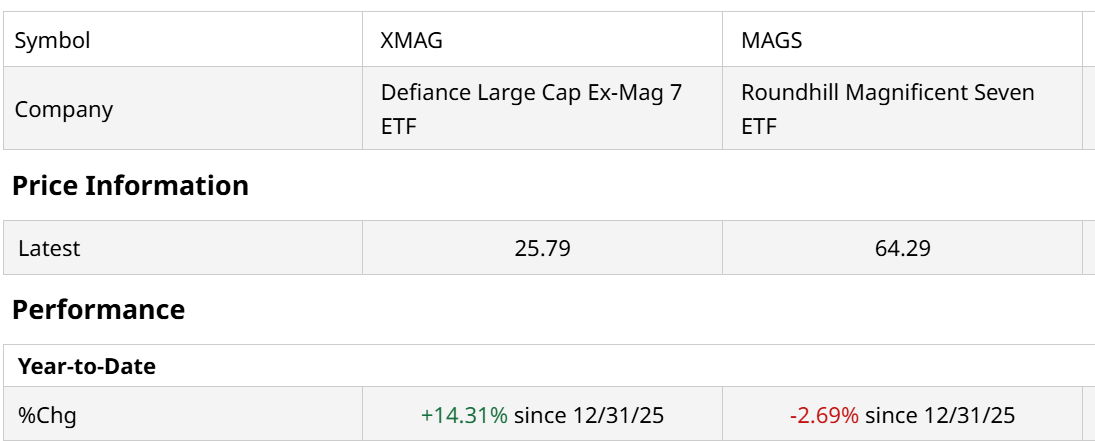

This is no longer about the Magnificent 7 stocks, as the Defiance Large-Cap Ex-Mag 7 ETF (XMAG), which intentionally excludes the Mag 7, shows.

They are not keeping up with the S&P 500 so far this year. In fact, they are down. On the other hand, XMAG is soaring, up more than 14% on the year. Most of those gains can be attributed to that group of 23 stocks above. It is a consistent story of a few leaders making up for the break-even rest of the pack.

A concentrated market like this means that the modern index is no longer functioning as a diversified basket reflecting the aggregate health of American business. Instead, it has effectively morphed into a highly speculative thematic fund. As someone who professionally managed money in the 1990s and through the dot-com bubble, I see way too many similarities. And I’ve adjusted to a shorter-term trading style.

Passive Investing Is Tempting Fate

Trillions of dollars in passive and momentum-driven capital are continually being forced into a tight circle of semiconductor, hardware, and digital infrastructure giants. This vertical capital allocation creates a sort of feedback loop. As the big stocks get bigger, at the expense of the rest, their weight in the index expands, causing every passive dollar to buy more of them, regardless of their underlying valuation or sales multiples. However, because the passive crowd has treated the index as a safe haven, the unwinding of this concentration will trigger a sharp distribution wave across the entire passive landscape. I just do not know exactly when.

Profiting from such an environment is not about the timing. It is about awareness and preparation. As noted here, my own personal plan includes what I do all the time anyway: be invested but hedged against disaster, using put options, option collars, cash, and inverse ETFs.

Do not let a few booming AI charts convince you that everything is fine. Recognize the lack of market breadth for what it truly is, acknowledge the history that makes this a very risky time for the stock market, and keep your risk strictly managed. Just in case the broader S&P 500 Index, and all of those ETF dollars that track it, are truly operating on borrowed time.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)