/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Artificial intelligence (AI) has undoubtedly been the biggest theme in the stock market over the past few years, with many AI-focused companies delivering spectacular gains. But as the sector matures, investors are beginning to look beyond industry giants like Nvidia Corporation (NVDA) and explore other parts of the AI supply chain that stand to benefit from the next phase of growth. One of the biggest winners from this shift has been Micron Technology (MU), which has enjoyed a stellar rally during the first half of 2026, outperforming many other AI-related stocks that have struggled to maintain their momentum.

The company's strong performance has been fueled by booming demand for its memory and storage chips, which are essential for AI workloads and data centers. At the same time, tight supply has pushed memory prices higher, creating an ideal environment for Micron. Now, the company is back in the spotlight after announcing an investment in Taiwanese wafer manufacturer GlobalWafers to help finance its new wafer fabrication facility in Sherman, Texas. The move is part of Micron's broader strategy to strengthen the United States semiconductor supply chain while supporting its long-term manufacturing expansion.

Also, the development has drawn attention from Wedbush Securities, which believes the investment could signal that wafer supply may become the next major hardware bottleneck for the semiconductor industry. According to the firm's analysis, Micron's decision suggests it expects wafer demand to rise significantly as investments in AI memory and logic chips accelerate through 2028, 2029, and 2030. If that plays out, securing wafer supply early could become an important competitive advantage. To support its long-term expansion, Micron plans to invest up to $3 billion to strengthen the U.S. semiconductor supply chain ecosystem, including its stake in GlobalWafers.

So, with Micron strengthening its position in the AI supply chain and preparing for future demand, let's take a closer look at whether the stock still has room to climb.

About Micron Stock

Founded in 1978, Idaho-based Micron Technology is one of the world's leading memory and storage chipmakers. The company develops a broad portfolio of DRAM, NAND, and NOR memory and storage products that power everything from smartphones and PCs to data centers, automotive systems, and industrial devices. Micron has built its business around developing innovative memory and storage solutions that help process, store, and move the growing volumes of data generated every day.

As AI adoption accelerates, the company's chips have become increasingly important, supporting compute-intensive applications, cloud infrastructure, and next-generation data centers. Its products also play a key role across the client and mobile ecosystem, extending from the data center to the intelligent edge. With a strong emphasis on technology innovation, manufacturing capabilities, operational efficiency, and customer-focused product development, Micron has positioned itself as one of the key companies enabling the AI-driven data economy.

The memory giant, now valued at around $1.11 trillion, has been on an extraordinary run over the past year. Fueled by explosive demand for memory and storage solutions amid the AI boom, the stock has soared an incredible 672.2% over the last 12 months, turning it into one of the market's biggest winners. The momentum hasn't faded in 2026 either. Shares have surged another 225% year-to-date (YTD), leaving the broader S&P 500 Index ($SPX) well behind. The benchmark index has returned 21.3% over the past year and 10.6% so far this year.

Nevertheless, no stock moves in a straight line forever. After hitting a record high of $1,255 on June 25 following its blockbuster Q3 earnings report, the shares have pulled back 27%. While some investors may see the decline as a sign to stay on the sidelines, others could view it as an opportunity to buy into one of the AI sector's strongest performers at a more attractive price.

Micron's AI-Fueled Growth Story Reached New Heights in Q3

Micron's latest earnings report left little doubt that the AI boom is still in full swing. With demand for AI-enabled memory and storage chips continuing to far outstrip supply, prices have remained elevated, and Micron is reaping the rewards. The company's third-quarter fiscal 2026 results, released on June 24, showcased just how powerful these industry tailwinds have become, delivering record-breaking numbers that blew past Wall Street's expectations. Investors cheered the report, sending the stock 15.74% higher in the following trading session.

The memory giant posted record quarterly revenue of $41.46 billion, marking its fifth straight quarter of record sales. Revenue surged an impressive 74% from the previous quarter and an astonishing 346% from the $9.30 billion reported in the same period last year. The result also comfortably topped analysts' consensus estimate of $36.72 billion, highlighting the extraordinary pace at which AI-driven demand is accelerating.

The growth story didn't stop at the top line. Micron's profitability reached new heights as strong pricing power and a richer mix of next-generation memory products drove non-GAAP gross margins to a record 84.9%, the highest in the company's history. That translated into non-GAAP net income of $28.86 billion and adjusted earnings per share (EPS) of $25.11, representing an eye-popping year-over-year (YOY) increase of more than 1,000%. Once again, Micron comfortably outperformed Wall Street's EPS estimate of $21.39.

The biggest growth engine was the company's data center business, where AI workloads continue to fuel an unprecedented appetite for high-performance memory and storage. Revenue from Micron's combined Cloud Memory and Core Data Center business units exceeded $25 billion during the quarter, representing an annualized revenue run rate of more than $100 billion. At the same time, data center SSD revenue surpassed $5 billion, more than doubling from the previous quarter as hyperscalers and enterprises ramped up AI infrastructure spending.

The strength was evident across Micron's entire product portfolio. DRAM revenue jumped 67% sequentially to $31.3 billion, accounting for 76% of total revenue, while NAND revenue surged 99% sequentially to $9.9 billion. Perhaps even more importantly, management said industry demand for both DRAM and NAND continues to significantly exceed available supply, with these tight market conditions expected to persist well beyond calendar 2027 as AI adoption accelerates across industries and structural supply constraints remain in place.

And if the third quarter wasn't impressive enough, Micron's outlook suggests the company expects the momentum to continue. For the fourth quarter of fiscal 2026, management forecast revenue of $50 billion, plus or minus $1 billion, alongside non-GAAP gross margins of roughly 86%. Adjusted EPS is projected to land between $30 and $32, signaling yet another quarter of exceptional profitability. With AI demand showing no signs of slowing and supply remaining constrained, Micron appears well positioned to extend its remarkable growth streak.

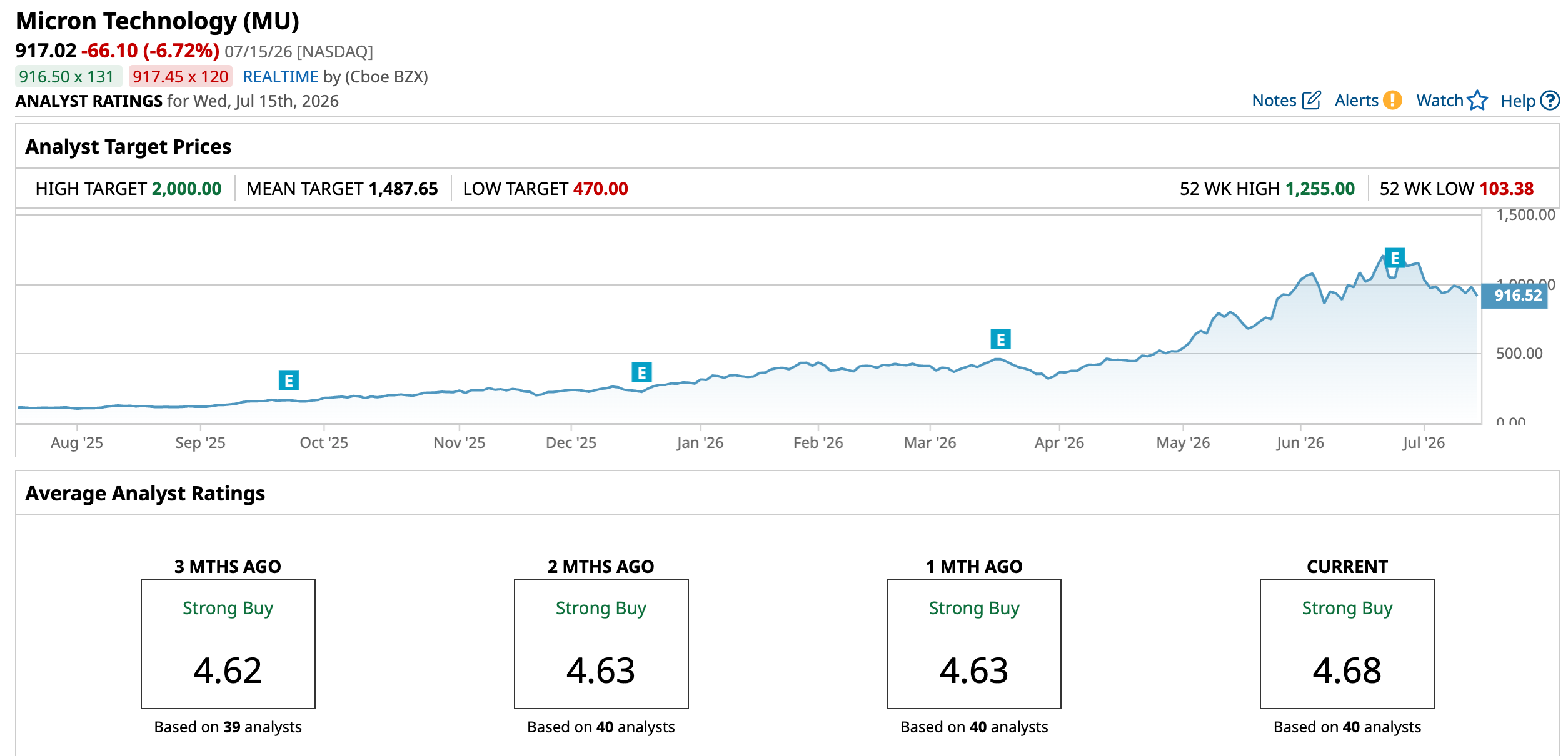

How Are Analysts Viewing Micron Stock?

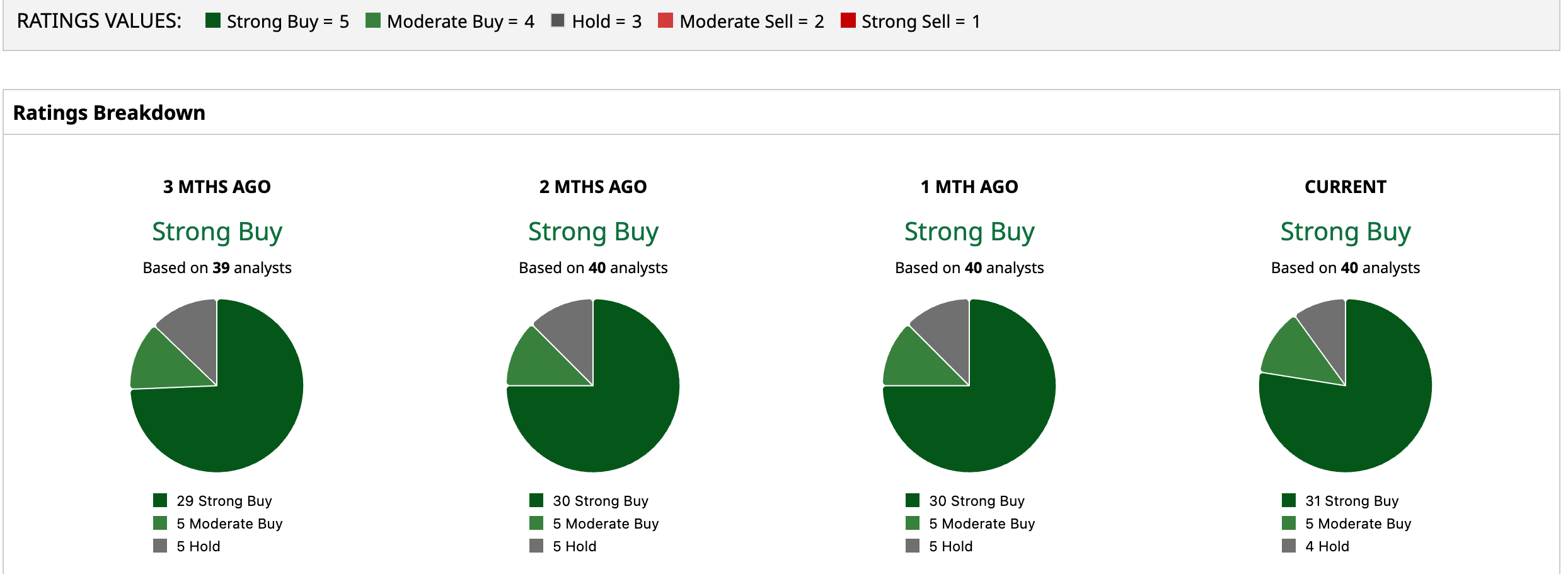

Overall, Wall Street remains overwhelmingly bullish on Micron. The stock currently carries a consensus "Strong Buy" rating, reflecting analysts' confidence in its long-term growth prospects. Among the 40 analysts covering the company, 31 rate it a "Strong Buy," five recommend "Moderate Buy," while the remaining four suggest "Hold." In fact, analysts also see meaningful upside ahead.

The average price target of $1,487.65 implies the stock could climb 62.2% from current levels, while the Street-high target of $2,000 points to a potential rally of as much as 118.1%. Those optimistic targets suggest Wall Street believes Micron's AI-driven growth story may still have plenty of room to run.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)