/Semiconductor%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

There’s a well-known comedian who likes to say, “I don’t know it for a fact, I just know it's true.” Well, if you’ve been thinking as I have that the influence of artificial intelligence (AI) on the S&P 500 Index ($SPX) has become too big to ignore, now you know it's true.

As a recent analysis by Goldman Sachs concluded, AI-linked companies have jumped from just 25% of the index in late 2022 (when ChatGPT launched) to 45% now. Let’s be clear: 45% of the S&P 500 now has its fate tied to AI. The spend, the ROI potential, the spoils, and the risks. Let that sink in.

With the index having morphed from the Magnificent 7 to the broader AI pie, we should consider what this means to all of the 11 sectors of the S&P 500. Perhaps most or all businesses will be AI-aligned in some way, shape, or form soon. It is becoming that ubiquitous.

But my question is this: does it create even more of a feast-or-famine situation for investors when looking across sectors? I’m a risk manager first, and I can’t help but think that yet another assumed investing ritual that has worked for the past century is now at risk of becoming a dinosaur. Right before our eyes.

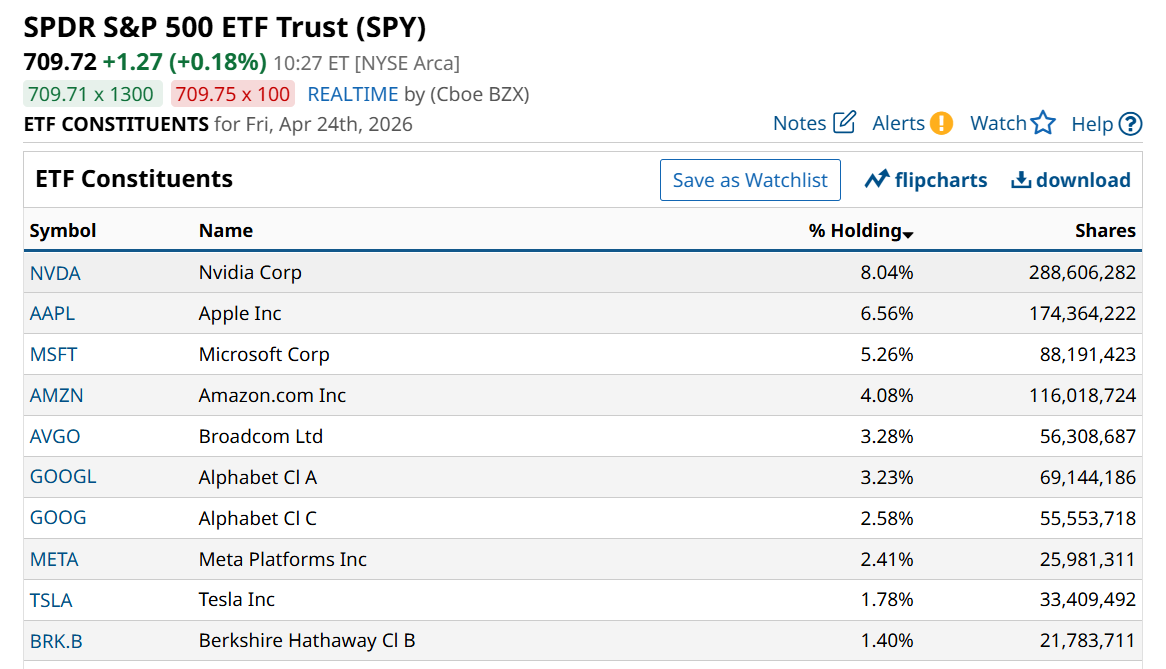

The sector allocation of the S&P 500 ETF (SPY), as of March 31, is largely tech and a handful of supporting players. There are also several sectors that barely matter in the grand scheme of things. They do not occupy enough space within the index to carry any meaningful influence.

Here is the impact across the board.

The Power Trio: Tech, Communications, and Discretionary

These three sectors now house the vast majority of the index’s most elite businesses, including most of the Mag 7. With tech alone making up over 33% of the index, and the three sectors having a majority vote (if this were Congress, which thankfully it isn’t), the correlation between these sectors and the broader S&P 500 is nearly 1:1.

For investors, this means that "diversifying" across these three sectors no longer provides safety; it simply doubles down on the same AI-driven momentum. If the AI hardware cycle pauses, these three sectors act as a single, massive weight on the index.

That doesn’t mean as an investor, I shy away from it. But I confront it, acknowledge it, and make sure I’m perennially hedged from that possible wake-up call, with my phone pinging me that the global markets just decided the tech bubble is done. If you lived and invested through 1987, 2000, and 2008, you know what I mean. If not, now you know!

The AI Utility: Energy and Utilities

These traditionally boring sectors have been drafted into the AI trade out of necessity. The massive data centers required for generative AI are power-hungry, leading to a fundamental repricing of the utilities sector as an infrastructure play.

Similarly, energy is no longer just a bet on crude oil; it is a bet on the baseload power needed to fuel the cloud. While they provide some defensive cushion, their performance is now increasingly linked to the capital expenditure plans of the hyperscalers.

The Performance Gap: Financials, Industrials, and Materials

For these “deep cyclical" sectors, the 45% AI concentration has created what I’ve heard referred to as a "capital vacuum." Even when these sectors report solid earnings, they often struggle to attract the same level of institutional flow as the AI-adjacent names.

This has led to a massive dispersion in valuations; while the AI elite trade at aggressive multiples, many financials and materials stocks are trading at historic discounts. They have become the "other 55%," moving more in tune with interest rates and inflation headlines than the index itself.

The Defensive Lag: Staples, Healthcare, and Real Estate

The most painful impact has been on the traditional defensive sectors. Consumer staples and healthcare (outside of AI-driven drug discovery) have largely been cooked by the liquidity shift. In a market where 45% of the index offers 30%-plus earnings growth, a stable 4% dividend from a staples giant no longer looks attractive.

Real estate, specifically commercial, faces the dual headwind of high rates and the AI-driven “cognitive labor” shift, which is reducing the need for traditional office space.

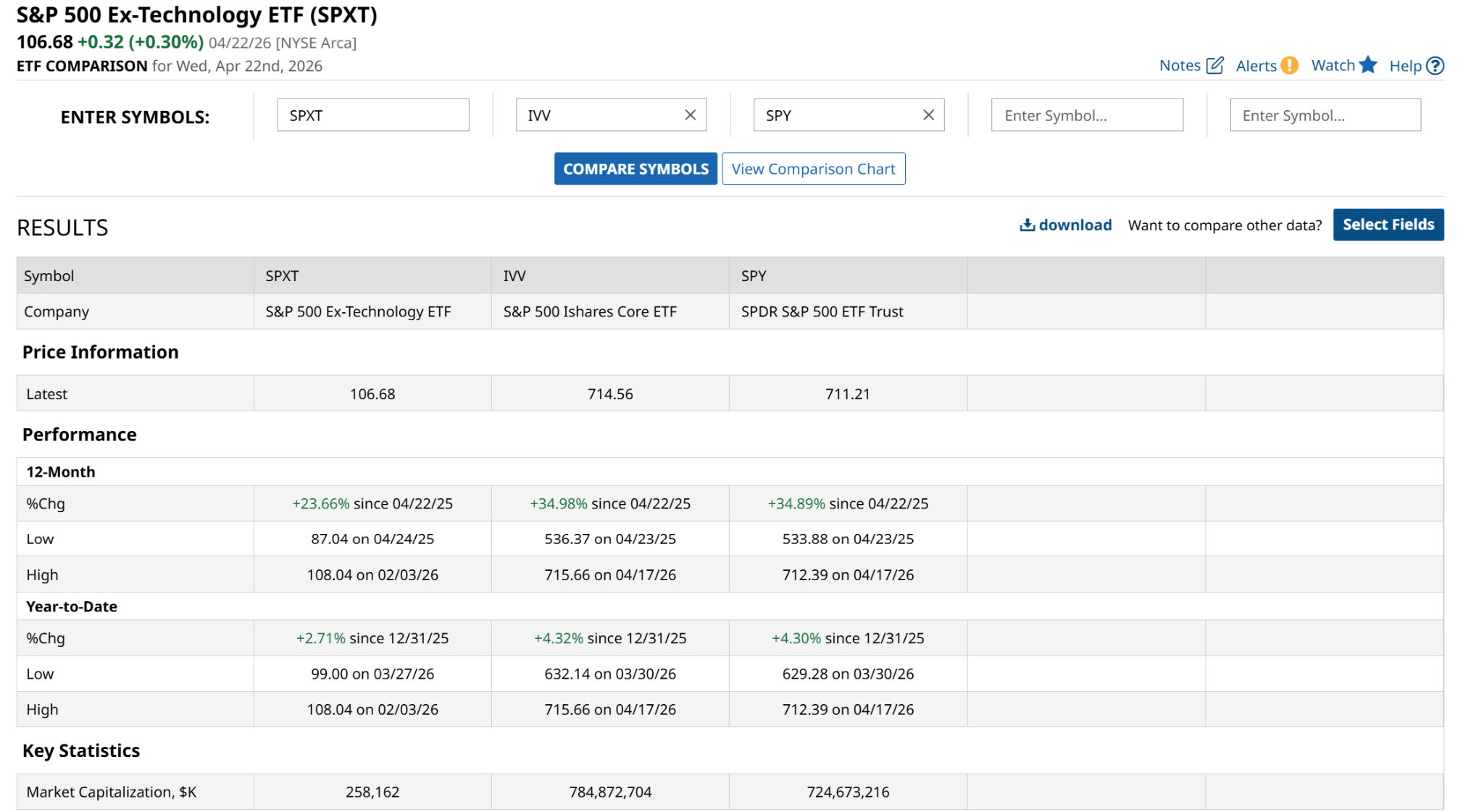

The S&P 500 Ex-Technology ETF (SPXT) is an exchange-traded fund (ETF) that could be considered a proxy for “not AI stocks” to some degree. That’s because it is the S&P 500 with the tech sector removed. That underperformance you see below is not just year to date and over the past 12 months. It is habitual, and thus now part of the mass investor psyche.

The Bottom Line

This level of concentration is a double-edged sword. When the AI engine is firing, the S&P 500 looks invincible, masking the stagnation in the bottom 400-plus stocks. However, it also means that the index is now vulnerable to an outsized failure.

If the AI narrative faces a genuine productivity reality check, there isn't enough weight in the other sectors to offset the drag. For the DIY investor and professional alike, the goal is to recognize that you are no longer buying a broad market index. You are buying a concentrated thematic fund with a 55% legacy stocks hedge.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)