Artificial intelligence (AI) server giant Super Micro Computer (SMCI) has endured a turbulent year, with headlines dominated by accounting concerns, governance issues, and regulatory scrutiny. The company even received a nudge from Nvidia (NVDA) CEO Jensen Huang to further strengthen its compliance and corporate governance practices. While those challenges have weighed on investor sentiment, Super Micro’s fundamentals continue to tell a different story.

Fresh off a blockbuster fiscal third-quarter earnings report and amid relentless demand for AI infrastructure, the company is once again reminding Wall Street why it remains a key player in the AI revolution. On June 2, Super Micro unveiled its latest collaboration with Advanced Micro Devices (AMD), announcing plans to showcase the next-generation AMD Helios rack-scale platform at Computex in Taipei, one of the world's largest AI and technology exhibitions.

The Helios platform represents a major leap in AI computing power, packing 72 AMD Instinct MI455X GPUs, 6th Gen AMD EPYC processors, and AMD Pensando networking technologies into a rack-scale architecture powered by AMD’s open ROCm software stack. Designed for hyperscalers, cloud providers, NeoClouds, and enterprises, the system is built to tackle some of the most demanding AI workloads, including sovereign AI projects, large language model (LLM) training, inference, and fine-tuning.

As the race to build AI infrastructure intensifies, Super Micro is proving that its growth story extends far beyond the controversies. With strong execution, expanding partnerships, and a growing portfolio of cutting-edge AI systems, the company is reinforcing its position at the heart of the AI boom. Against that backdrop, here's a closer look at SMCI.

About Super Micro Stock

Founded in San Jose, California, Super Micro Computer has grown from a niche server maker into one of the biggest players in AI-focused IT infrastructure. The company designs and builds systems for enterprise computing, cloud data centers, artificial intelligence workloads, and emerging technologies such as 5G and edge computing. Its portfolio spans servers, storage solutions, AI platforms, networking products, software, IoT offerings, and support services, placing Super Micro right at the center of the AI infrastructure boom.

A major strength of Super Micro's business is its ability to design and manufacture many of its products in-house. With operations across the U.S., Taiwan, and the Netherlands, the company maintains significant control over key components such as motherboards, power systems, and chassis. This vertically integrated model helps improve efficiency, supports large-scale production, and allows the company to quickly adapt to changing customer needs in the fast-growing AI and data center markets.

Super Micro is also known for its modular "Server Building Block Solutions" strategy, which gives customers the flexibility to tailor systems to their specific workloads. From processors and GPUs to storage, networking, and cooling technologies, including both air and liquid cooling, the company's products can be customized for a wide range of enterprise, cloud, and AI applications. Today, Super Micro carries a market value of roughly $30.17 billion.

While the company's regulatory and governance issues have created uncertainty for investors, SMCI stock has staged a remarkable turnaround in 2026. Strong earnings growth and surging demand for AI infrastructure have helped shift attention back to the company's underlying business momentum. Investors cheered the latest AMD Helios platform announcement on June 2, sending shares 7% higher.

In fact, the stock also received a boost from Dell’s (DELL) strong quarterly results, as enthusiasm around AI infrastructure spending spilled over to other server makers. Although SMCI remains almost 25% below its 52-week high of $62.36 reached last July, the stock has still delivered a 9.12% gain over the past year. Its 2026 performance has been even more impressive, with shares soaring 61% year-to-date (YTD), easily outpacing the broader S&P 500 Index's ($SPX) 10.74% gain over the same period.

Deep Diving Into Super Micro’s Q3 Performance

Super Micro's fiscal third-quarter 2026 results, released on May 5, highlighted both the opportunities and growing pains that come with operating at the center of the AI infrastructure boom. While the company delivered a mixed earnings report, investors focused on the bigger picture, sending SMCI shares soaring 24.5% in the following trading session.

Revenue climbed to $10.24 billion during the quarter, more than doubling from $4.6 billion a year earlier and marking an impressive 123% year-over-year (YOY) increase. Even so, the figure came in below Wall Street's expectations of roughly $12.36 billion, reflecting just how elevated investor expectations have become amid the AI spending frenzy.

Despite the revenue shortfall, demand trends remained highly encouraging. Super Micro noted that orders and backlog continued to grow as customers accelerated investments in AI infrastructure. AI GPU platforms remained the company's primary growth engine, accounting for more than 80% of total quarterly revenue.

The company's customer mix also showed strength across multiple end markets. Revenue from enterprise and channel customers rose to $2.8 billion, representing 28% of total sales compared to 15% in the prior quarter and increasing 46% from a year ago. Meanwhile, revenue generated from OEM appliance and large data center customers reached $7.4 billion, accounting for roughly 72% of total revenue and posting an impressive 183% year-over-year increase.

Where Super Micro truly impressed investors was on the earnings front. The company reported adjusted non-GAAP earnings of $0.84 per share, comfortably ahead of analyst expectations of approximately $0.63 per share. Earnings surged 171% from $0.31 per share in the year-ago quarter, helped by a meaningful improvement in profitability.

Margins, which had been under pressure in recent quarters, showed notable signs of recovery. Non-GAAP gross margin improved to 10.1%, up from 6.4% in the previous quarter and 9.7% a year earlier. Management attributed the improvement to a more favorable product and customer mix, lower tariff-related costs, reduced expedite expenses, and fewer inventory reserve charges.

At the same time, the company continues to invest heavily to support its rapid expansion. Operating cash flow reflected those demands, with $6.6 billion used in operations during the quarter, while capital expenditures and investments totaled $97 million. As of March 31, Super Micro held $1.3 billion in cash and cash equivalents, compared to $8.8 billion in total bank debt and convertible notes. Management's outlook suggests the growth story is far from over.

For the fiscal fourth quarter, Super Micro expects revenue between $11 billion and $12.5 billion, along with GAAP earnings per share of $0.53 to $0.67 and non-GAAP earnings per share of $0.65 to $0.79. For fiscal 2026 as a whole, the company is projecting revenue in the range of $38.9 billion to $40.4 billion, underscoring the extraordinary scale of demand tied to the ongoing AI infrastructure buildout.

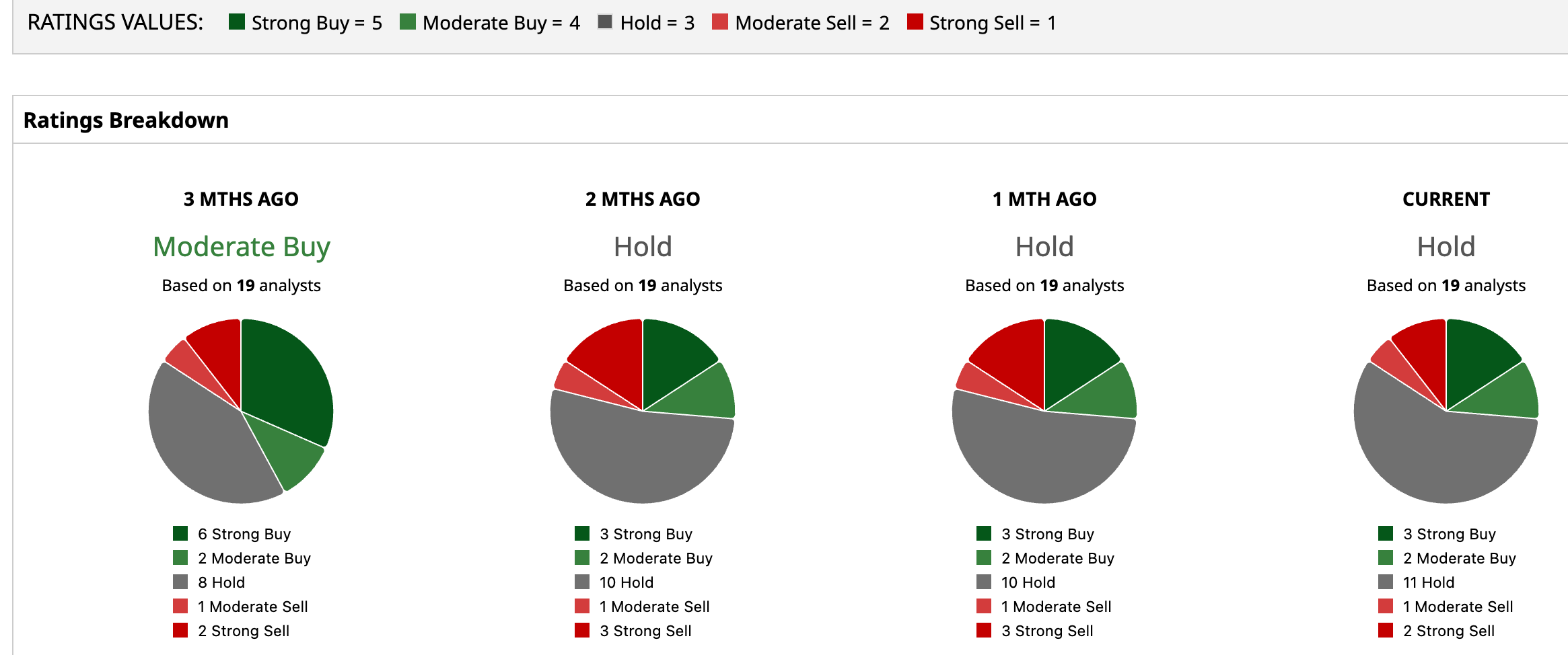

How Are Analysts Viewing Super Micro Stock?

While investor enthusiasm around Super Micro has picked up considerably in recent weeks, Wall Street remains somewhat divided on the stock's outlook. SMCI currently carries a consensus "Hold" rating, suggesting that many analysts are waiting for additional proof that the company's rapid growth can be sustained. Among the 19 analysts covering the stock, three rate it a "Strong Buy," two recommend "Moderate Buy," and 11 maintain "Hold" ratings. Meanwhile, one analyst has assigned a "Moderate Sell" rating, while two remain firmly bearish with "Strong Sell" recommendations.

Notably, the stock's recent rally has been so powerful that shares have already surged past both the consensus price target of $36.27 and the Street-high target of $50, highlighting how dramatically investor sentiment has shifted amid the ongoing AI infrastructure boom.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.