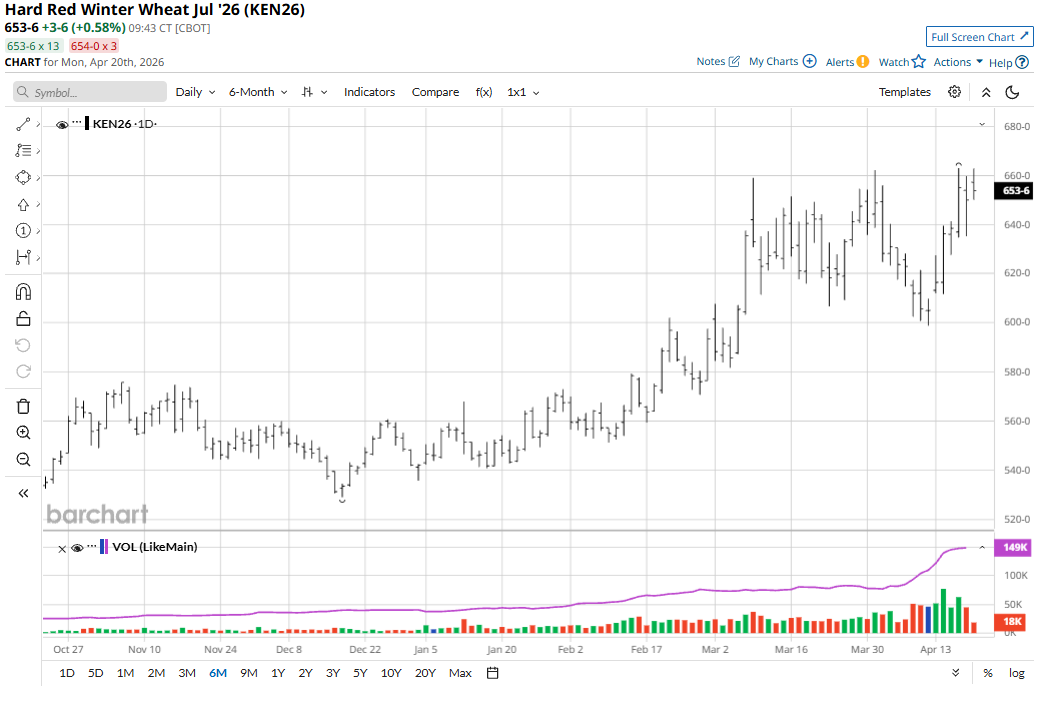

July soft red winter (SRW) wheat (ZWN26) futures on Friday fell 7 1/4 cents to $5.99 1/4 and for the week were up 18 1/2 cents. July hard red winter (HRW) wheat (KEN26) futures lost 5 cents to $6.50 but for the week were up 45 cents.

The winter wheat futures markets on Friday saw some routine profit-taking pressure heading into the weekend. However, it was a good week for the bulls, which suggests some more price strength this week.

Too-dry weather in U.S. HRW country, as well as dry conditions in Australian wheat regions, are supporting the rallies in wheat futures markets. Forecasts for the U.S. HRW area don’t look promising, either. A cold snap over the weekend may produce some damage to the HRW crop in the western High Plains. Precipitation next week in HRW country will remain limited.

News reports say farmers in Argentina are considering a reduction in wheat plantings due to high fertilizer costs, with some switching to corn or soybeans due to limited profit margins. In the meantime, Australia’s wheat acreage for the 2026/27 crop is expected to fall to a seven-year low due to weak prices and shortages of fertilizer and fuel, Bloomberg reported.

Another bright spot for the wheat markets has been the selloff in the U.S. dollar index ($DXY), which hit a six-week low this week. If the greenback continues to depreciate in the coming weeks and months, such would make U.S. wheat more price-competitive on the world market and likely provide a boost to U.S. export sales that have been lagging recently.

Corn Futures May Have Put in a Price Bottom

July corn (ZCN26) futures on Friday fell 1/4 cent to $4.57 1/2 and for the week were up 6 1/2 cents. Corn futures trading has been choppy, but the bulls had the better week, supported by rallying wheat prices. Last week’s price action in July corn suggests the market may have put in a near-term bottom, as the technical posture has improved.

Corn traders will keep watching the weekly USDA crop progress reports on Monday afternoons. Corn planting in the U.S. Midwest may be slowed in northern regions due to recent heavy rains. A drier weather pattern will occur in that area this week, however.

It appears the war in the Middle East may be winding down (or trying to), which will allow the grain market traders to once again be better focused on their own supply and demand fundamentals in the coming weeks and months.

Soybeans See Choppy and Sideways Trading Action

July soybeans (ZSN26) on Friday rose 2 1/2 cents to $11.83 and for the week were down 8 1/4 cents. The soybean market paused most of the session Friday, amid a sharp selloff in bean oil (ZLN26) that came due to a strong downside move in crude oil (CLK26) prices. Spreaders were featured selling bean oil and buying meal (ZMN26).

Soybean planting progress will be tracked by USDA in its weekly crop progress report on Monday afternoons. Planting has been off to a quick start in the southeastern U.S., with warm and dry conditions allowing for plenty of fieldwork.

The scheduled summit meeting between Presidents Donald Trump and Xi Jinping in China in mid-May will be a focal point for the soy complex traders.

Strong domestic soybean crushing numbers in recent reports offer a firm underpinning for the soy complex futures. The latest National Oilseed Processors Association (NOPA) report for March showed the second- highest daily crush use on record for the month of March.

Cotton Bulls Keep Their Pedal to the Metal

July cotton (CTN26) futures on Friday rose 169 points to 79.82 cents and hit a two-year high. For the week, July cotton was up 4.49 cents.

Technical buying has been featured in the natural fiber amid a strong price uptrend in place on the daily bar chart. Better risk appetite in the general marketplace recently, as well as a recently weak U.S. dollar index, have also supported buying interest in cotton futures.

Slightly improving U.S.-China trade relations could be a positive element on the U.S. cotton export demand front in the coming months. The Trump-Xi meeting in China in mid-May will be closely monitored by cotton traders. China is a major cotton importer.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)