/Palantir%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock.jpg)

Palantir Technologies (PLTR) generated strong Q1 free cash flow (FCF) and higher FCF margins. And analysts keep hiking their revenue forecasts. So, why is PLTR stock so cheap? It could be worth 62% more at $219 per share. This article will show why.

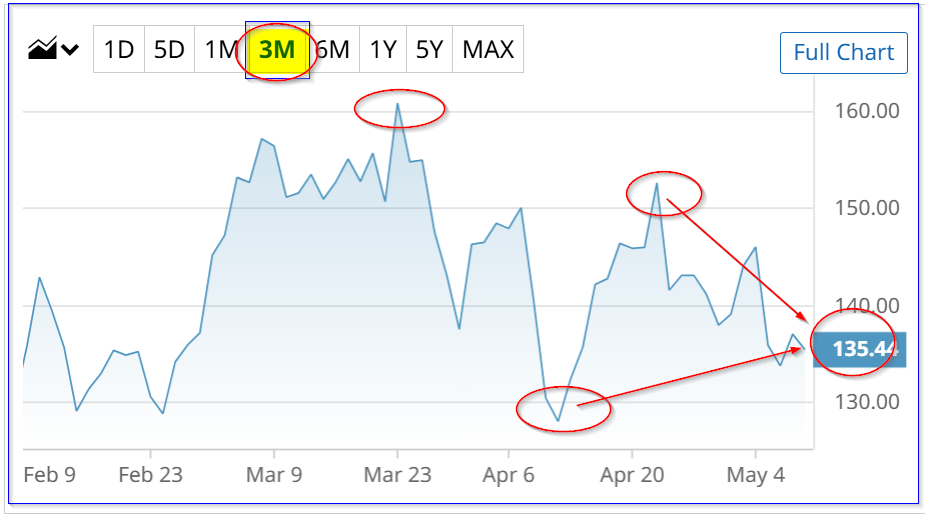

PLTR is at $135.14 in midday trading, down 1% but off 7.3% since May 4 when its Q1 shareholder letter was released after the market close. It's only slightly over its 6-month low of $128.84 on Feb. 28.

Strong FCF and FCF Margins

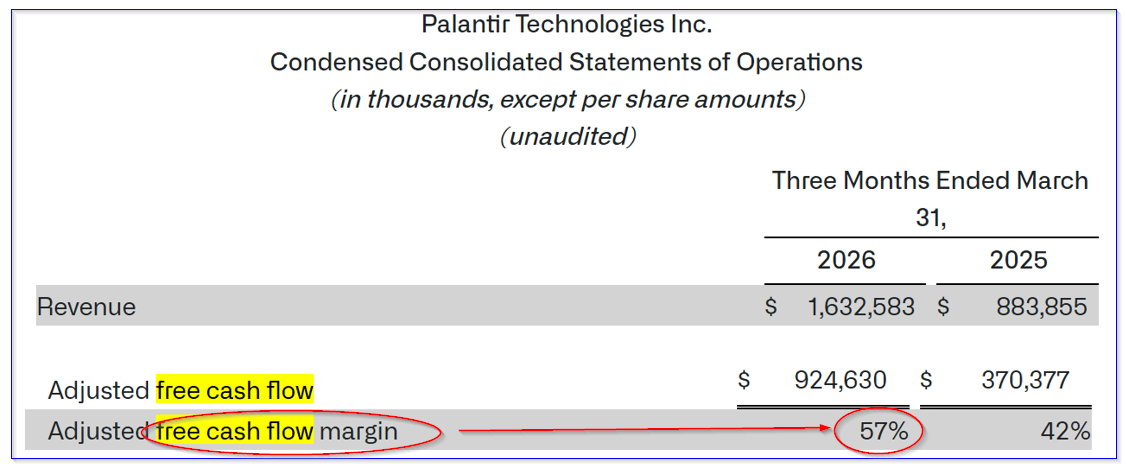

Palantir reported strong Q1 revenue growth (+85% YoY), adjusted free cash flow (FCF) growth (+150%), and adj. FCF margins (56.5% vs 41.9% last year). This can be seen in the tables below.

This was slightly better with its Q4 adj. FCF margin (56.3%, i.e., $791.4m adj. FCF on $1.4 billion in revenue), and much better than its 2025 adj. FCF margin of 50.7% (i.e., $2.27 billion adj. FCF on $4.475 billion in revenue).

In other words, management is continuing to squeeze out higher cash flow as revenue rises. That is a true sign of operating leverage and deep profitability.

It implies that adj. FCF will grow exponentially as revenue grows. That should increase the value of PLTR stock.

In fact, management raised its adj. FCF 2026 estimate to be between $4.2 billion and $4.4 billion. That's up +7% from $3.925 billion to $4.125 billion in its Q4 shareholder letter.

Moreover, given management's new higher 2026 revenue estimate range of $7.65 billion to $7.662 billion, it implies 2026's adj. FCF margin will be:

$4.3 billion (midpoint) adj FCF / $7.656 billion revenue = 0.5617 = 56.17% adj FCF margin

(By the way, this is very unique. Palantir is one of the only tech companies, besides Palo Alto Networks (PANW), that guides investors on its adj. FCF margins).

Let's look at its future adj. FCF and related valuation.

Forecasting FCF

Analysts have hiked their 2026 and 2027 revenue forecasts. Seeking Alpha reports that the average of 29 analysts' revenue estimates for 2026 and 2027 is:

2026 revenue ……….. $7.67 billion (up from $7.26 billion last month)

2027 revenue ………. $11.09 billion (up from $10.39 billion)

As a result, for the next 12 months (NTM), the average revenue forecast is $9.38 billion.

So, if we assume a 56.17% adj. FCF margin (as management does - see above):

$9.38 billion NTM revenue x 0.5617 = $5.27 billion adj. FCF

That's +22.5% higher than management's midpoint 2026 FCF guidance. And don't forget, once the market focuses on 2027, adj. FCF estimates could be even higher. This implies PLTR's value could be much higher over the coming year.

Higher Price Targets

For example, just as I did in my April 12 Barchart article, let's use a 1.0% FCF multiple to value PLTR's adj. FCF forecasts:

$5.27 billion / 0.01 = $527 billion market value

That's over $200 billion and +62% higher than Palantir's present market cap of $325 billion, according to Yahoo! Finance:

$527b / $325b = 1.622

In other words, PLTR stock is worth 62.2% more:

$135.14 x 1.622 = $219.20 price target (PT)

Other analysts agree that PLTR is undervalued. For example, Yahoo! Finance shows that 31 analysts have an average PT of $181.73 (+34.5%), and Barchart's mean survey PT is $192.00 (i.e., +42%).

The bottom line is that PLTR stock is deeply undervalued. However, there is no guarantee it won't keep falling. So, one way to play it is to sell short cash-secured, near-term put options to set a lower buy-in price.

Shorting Cash-Secured PLTR Puts

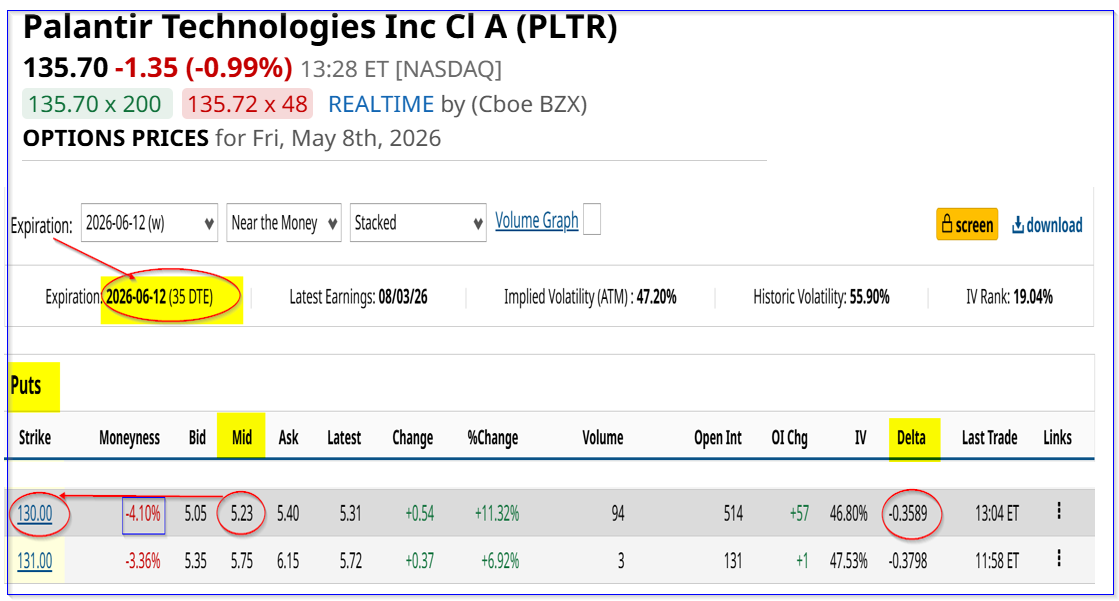

For example, the June 12 options expiry period shows that the $130 strike price put option, i.e., 4% below today's price, has an attractive midpoint premium of $5.23.

That implies that a cash-secured short-seller of this put can make an immediate yield of 4.0% (i.e., $5.23/$130.00 = 0.0402).

This means that if an investor secures $13,000 in cash or buying power with their brokerage firm, can then enter an order to “Sell to Open” 1 put contract. The cash acts as collateral to buy 100 shares at $130.00.

The account will then immediately receive $523, bringing in 4.0% of the collateral secured. Even if PLTR falls to $130 by June 12, the account will keep the $523.

As a result, if the account is assigned to buy 100 shares at $130, the actual breakeven is lower:

$130 - $5.23 = $124.77, or -7.67% below today's price

That's an attractive proposition to many value investors. For example, if an investor can repeat this play for 3 months, the potential return is over 12%, even if the account is not assigned to buy shares. And the annualized expected return is over 48%.

That's not equal to the upside of 62% of owning PLTR outright. But it provides a good expected return with a potentially lower buy-in point.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)