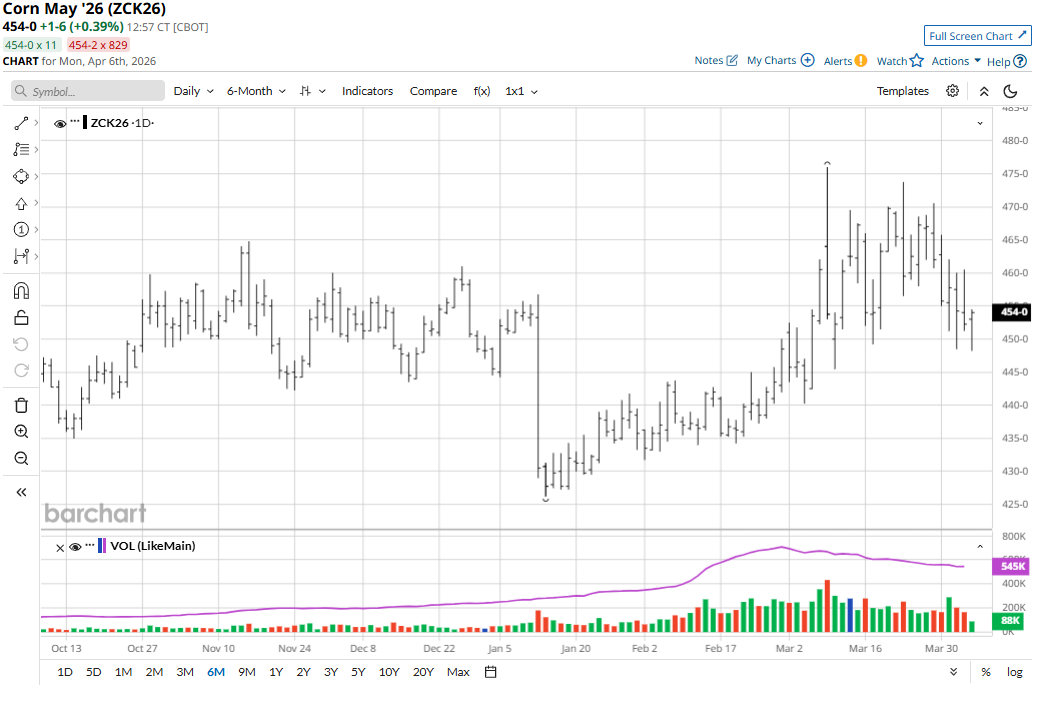

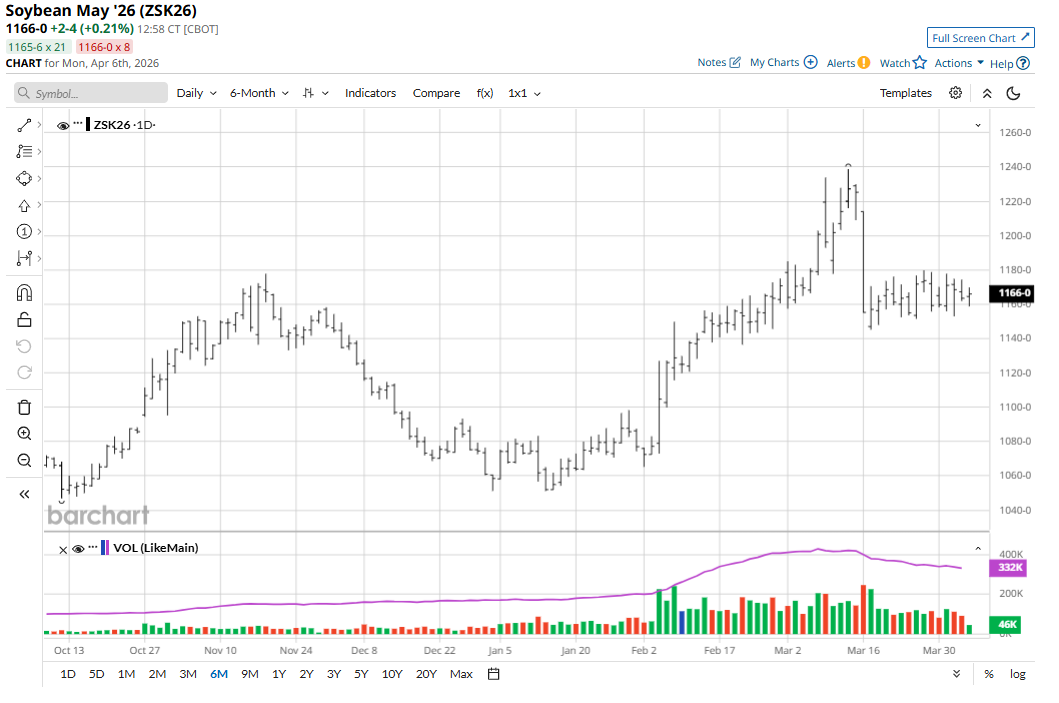

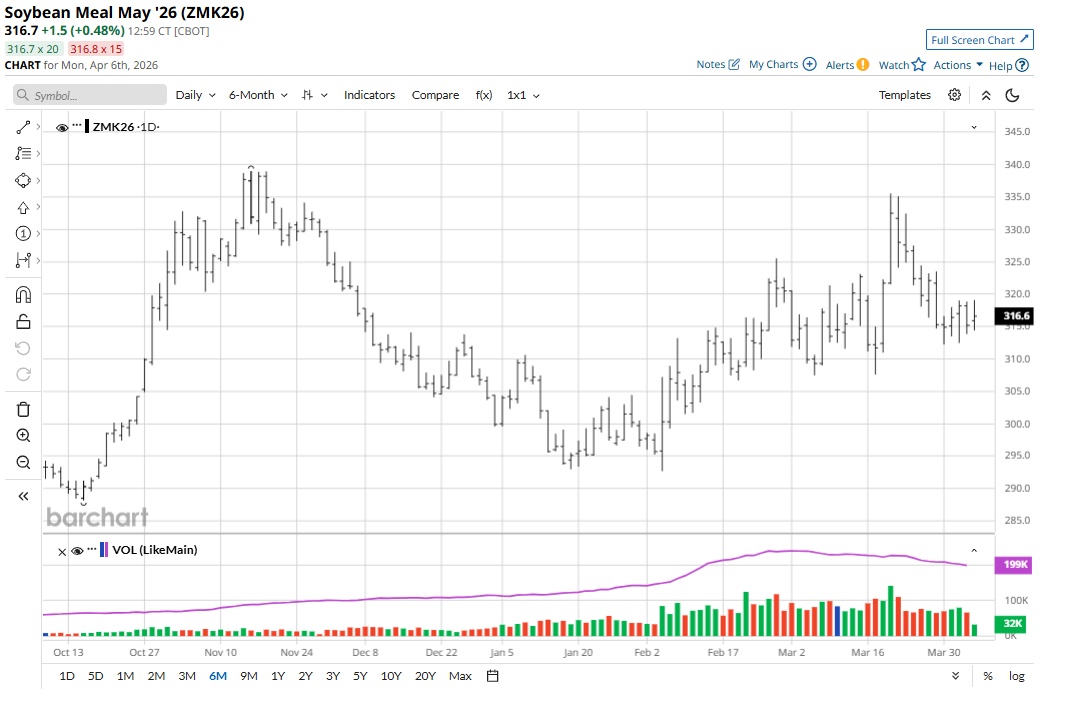

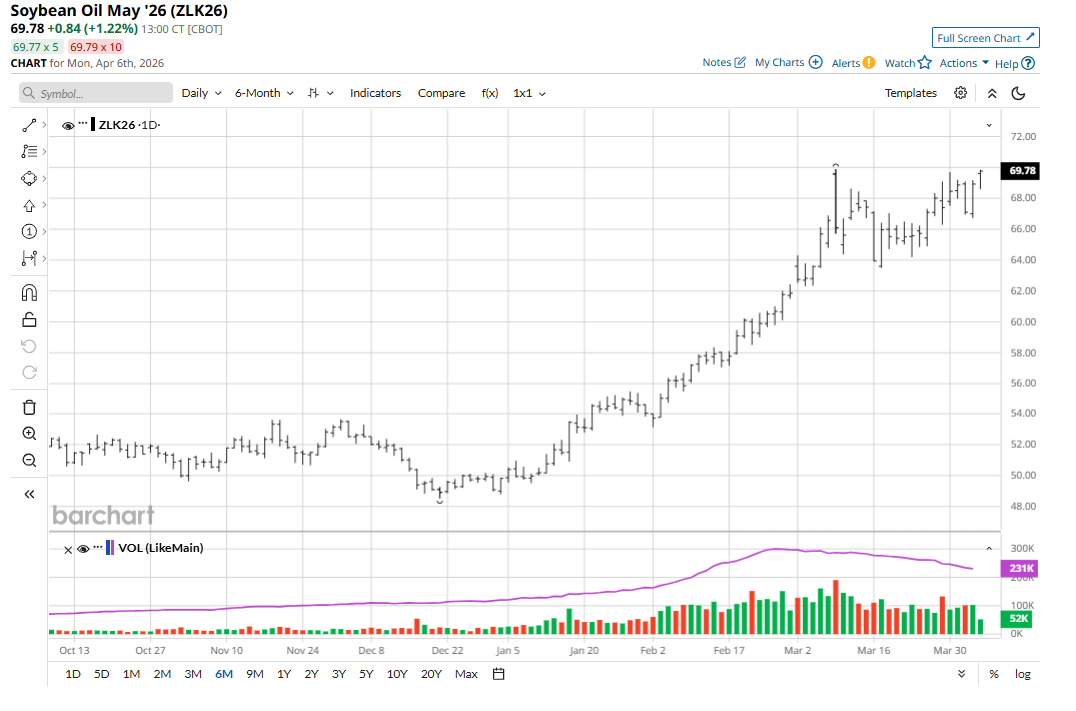

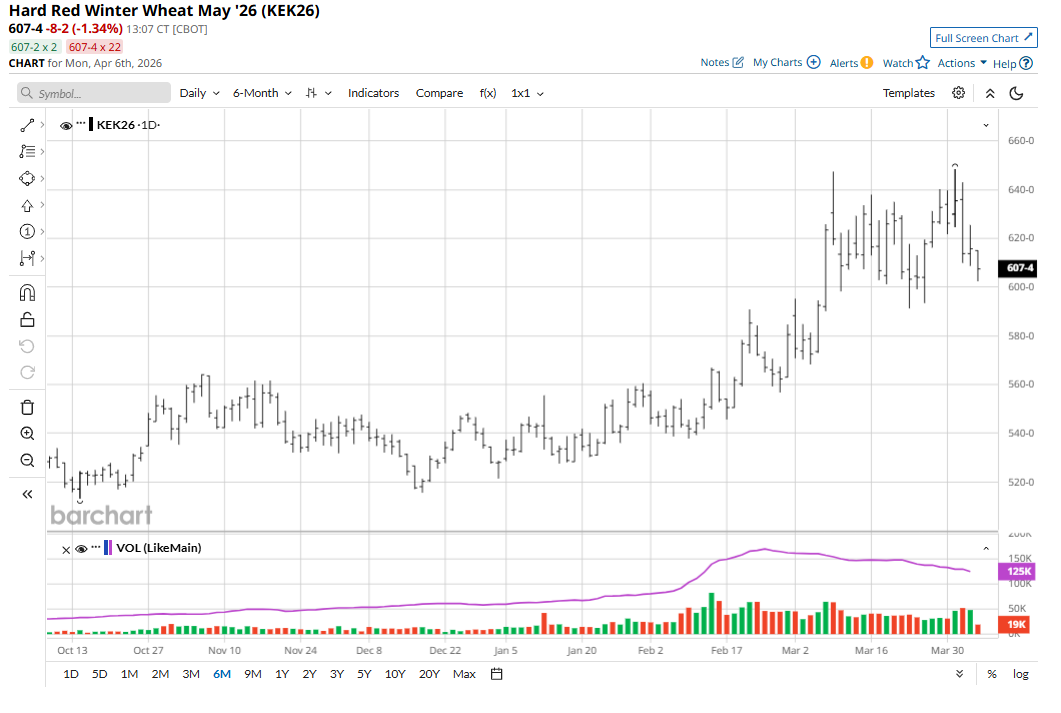

Last week’s holiday-shortened four-day trading period saw May corn (ZCK26) lose 9 3/4 cents on the week. May soybeans (ZSK26) on the week were up 4 1/4 cents. May soybean meal (ZMK26) was down 10 cents and May bean oil (ZLK26) rallied 153 points last week. May soft red winter wheat (ZWK26) futures were down 6 3/4 cents last week, while May hard red winter (KEK26) lost 17 cents.

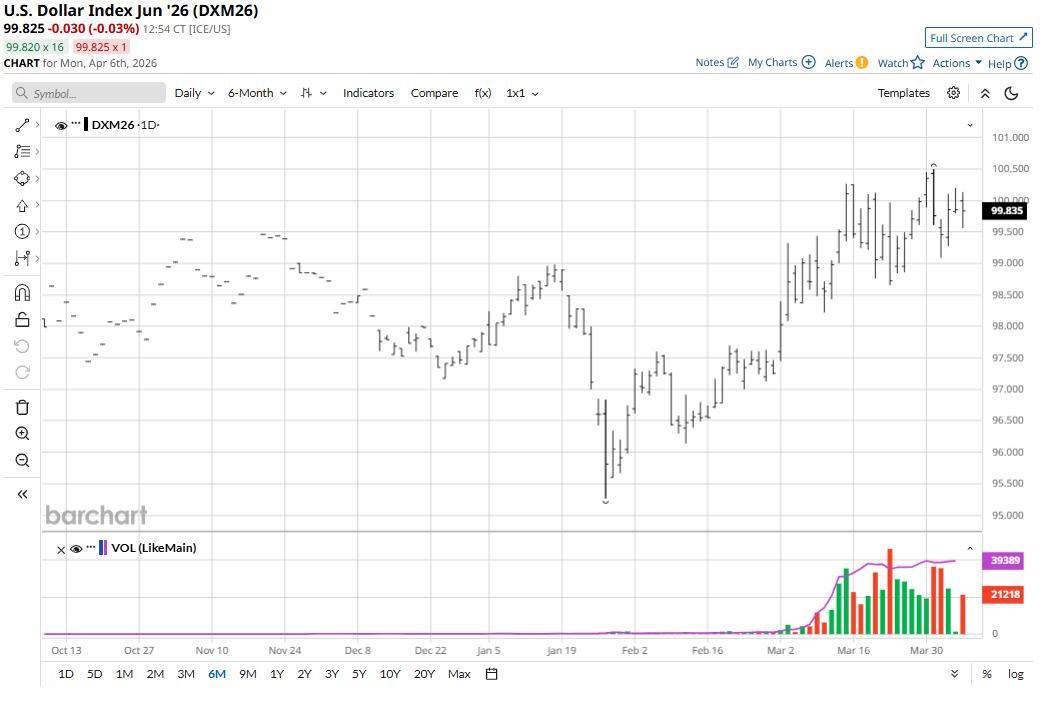

A strong U.S. dollar index ($DXY) that is near a 10-month high has been a negative “outside-market” influence on grains recently. A stronger greenback makes U.S. grain more expensive to purchase in non-U.S. currency. Most global grain trade is priced in U.S. dollars.

Interestingly, the surge in Nymex West Texas Intermediate (WTI) crude oil (CLK26) futures above $113.00 a barrel last week provided little spillover support to the grain futures markets. Just three weeks earlier, grain futures prices were rallying in part due to the up-trending crude oil market.

Remember that traders and markets are fickle. It seems the rally in the grains three weeks ago came on notions that the rising tide in crude oil, the leader of the raw commodity sector, would lift all raw commodity boats.

Last week, the thinking in the raw commodity marketplace pivoted to ideas that spiking global energy prices will lead to problematic inflation and slowing global economic growth, which can be extrapolated to mean less global demand for raw commodities, including grains.

The other bearish element hanging over the grain futures markets at present is the keener risk aversion in the general marketplace — evidenced by the U.S. and global stock markets trending mostly lower since the start of the Middle East war. Speculative bulls do not like to see risk-off trading days in the stock market.

Corn Suffers Near-Term Technical Damage

May corn futures on Thursday saw a technically bearish weekly low close that also saw a price uptrend on the daily bar chart negated.

The corn market last week also got some modestly downbeat USDA data that included a report showing U.S. farmers intend to plant 95.3 million acres of corn, which is a 3% (3.45 million-acre) decrease from 2025, but is a higher number than most analysts had expected from the report. The weekly USDA corn export sales report also leaned bearish. On the positive side, the USDA quarterly grain stocks report that was out last Tuesday suggested demand for the largest U.S. corn crop on record continues strong.

Weekly USDA crop progress reports will begin in April, providing traders and farmers with some better perspective on planting and growing conditions for U.S. crops. In the coming weeks, corn traders will continue to monitor weather and growing/harvesting conditions for South American crops, as well as weather conditions in the U.S., as corn-planting season is now not that far off.

Soybean Market Languishing, Bean Oil Surges

USDA’s planting intentions report last week projected that U.S. farmers will plant 84.7 million acres of soybeans, a 4% increase from 2025. While the number was a significant year-over-year rise, the total acreage came in slightly below average trade expectations. However, the data did little to support the soybean bulls last week.

Recent trade in the soybean complex futures has seen spreaders featured buying soybean oil and selling meal futures. That’s bullish for bean oil at present. Bean oil has been supported by the renewed focus on biofuels as crude oil prices soar. However, those long bean oil, short meal spreads will have to be unwound at some point, which will be bullish for meal and bearish for bean oil.

Last week’s weekly USDA export sales report was also disappointing to the bean market bulls. U.S. soybean exports remain sluggish, with China slow to make additional purchases due in part to the premium U.S. soybeans hold over Brazilian beans.

The scheduled summit meeting between Presidents Donald Trump and Xi Jinping in China in mid-May will be a focal point for the soy complex traders.

Winter Wheat Futures Markets Choppy, HRW Bulls Eye Dry Weather

The winter wheat futures markets saw modest corrective rebounds to end the trading week Thursday. However, gains were limited as USDA Thursday morning reported weekly U.S. wheat export sales were a marketing-year low – down 51% from the previous week and down 33% from the four-week average.

Potentially lower yields from extreme weather in U.S. wheat country are working in tandem with historically low U.S. wheat acreage, as seen in last week’s USDA planting intentions report, to offer price support, or at least limit selling interest, in SRW and HRW futures. Currently, 57% of U.S. winter wheat acres are in drought. U.S. hard red winter wheat areas in the western high Plains region will not get much precipitation for a while, leaving crops stressed. Canada’s southwestern Prairies are also dry and need significant spring moisture.

The dry conditions could provide the winter wheat market bulls the spark they need to push prices out of their choppy trading ranges.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)