Tobacco has always been in a strange corner of the market: controversial, heavily regulated, yet still capable of producing massive cash flow.

Altria and Philip Morris International sit right at the center of that discussion. At first glance, they may appear to be two versions of the same business, especially since both are connected to Marlboro. But once you look closer, the story starts to split. One is built around the U.S. market and pays a much higher dividend, while the other is larger, more global, and more aggressive in reshaping its business beyond traditional cigarettes.

So, which one is the better buy today: the cheaper income stock, or the global company trying to lead the next phase of nicotine?

Altria (MO)

Altria Group is a U.S.-based tobacco and nicotine company. It is known for Marlboro cigarettes through its Philip Morris USA business and while its core business remains cigarettes, the company has begun expanding into smokeless tobacco, nicotine pouches, and e-vapor products.

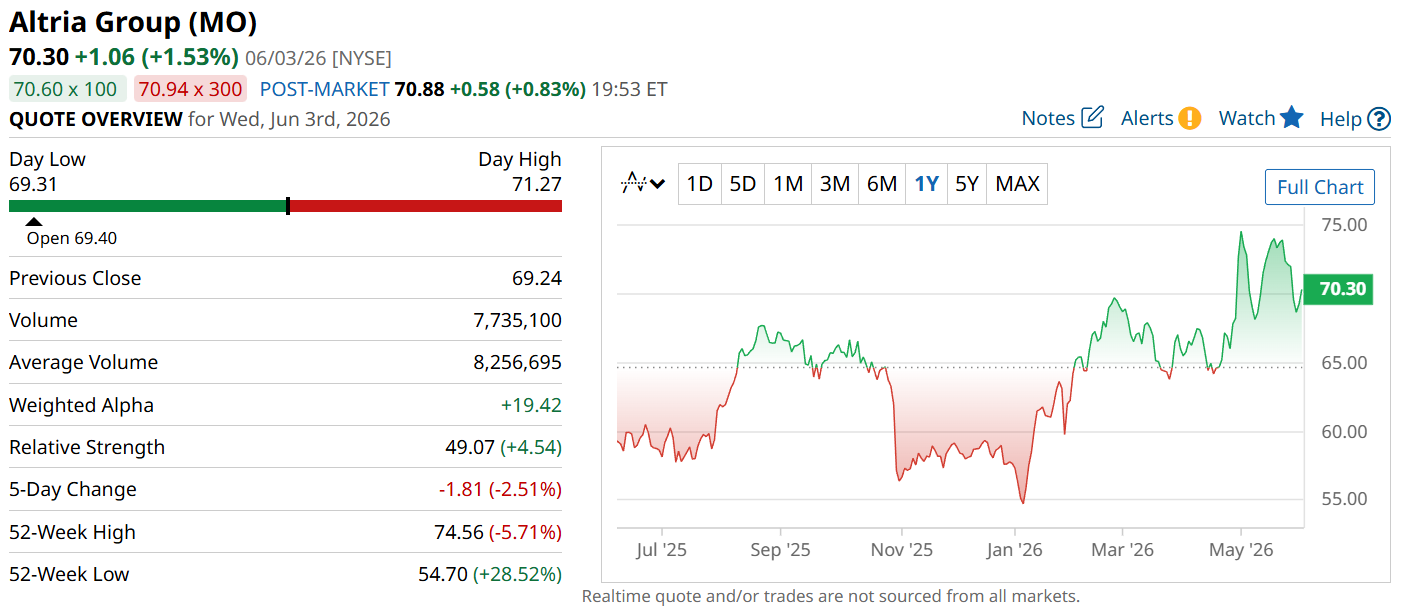

The stock has traded between ~$55 and ~$75 over the past 52 weeks and, at the time of writing, is trading near the upper end of that range with a market cap of ~$117 billion.

Philip Morris (PM)

Philip Morris International, on the other hand, is a global tobacco and nicotine company with a large international business and a U.S. segment tied to Swedish Match and ZYN. It is also best known internationally for Marlboro. Unlike Altria, it has put a heavier focus on smoke-free products, including heated tobacco, nicotine pouches, and alternatives for adult nicotine users.

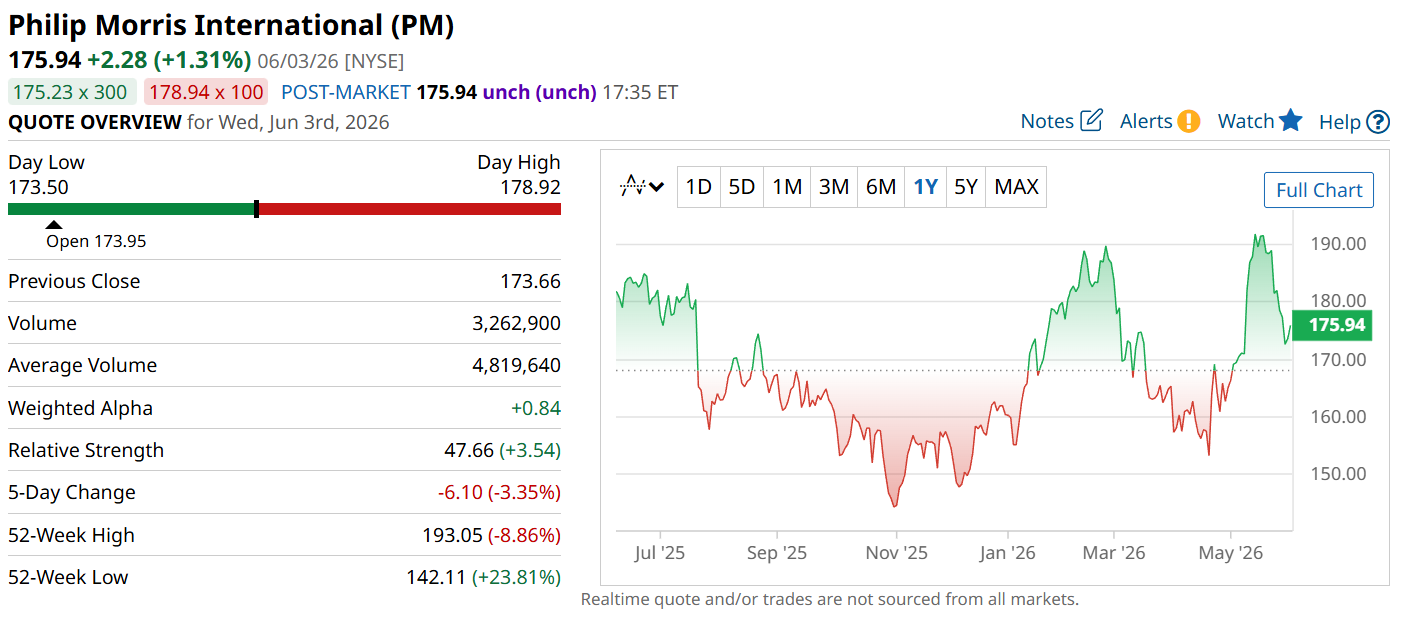

It is the bigger company in this comparison, with a market cap of ~$274 billion. The stock has traded between ~$142 and ~$193 over the past 52 weeks and is currently in the middle of that range.

It may be confusing that both companies are connected with Marlboro - the key distinction is geography. Altria controls the Marlboro business in the United States through Philip Morris USA (Altria’s subsidiary), while Philip Morris International (a separate publicly listed company) controls Marlboro in markets outside the U.S.

So, is the bigger company the better buy? There are other matters we should look at to answer that.

Business model comparison

Altria and Philip Morris International are both in the tobacco and nicotine industry. They share the same customer base, repeat purchases, and pricing power.

But the key difference is their markets and product direction.

Altria is mainly a U.S. business. Its challenge is that cigarette volumes in the U.S. continue to decline, so it relies on price increases and newer nicotine products to support its business.

Meanwhile, Philip Morris International has a wider global footprint and is more aggressive in expanding into smoke-free products. Specifically, it invests heavily in heated tobacco, nicotine pouches, and other alternatives for nicotine users.

Put simply, Altria may lead locally, but Philip Morris has the larger market opportunity, with a global presence and greater alignment with industry trends.

Financial health

Now let’s look at their latest reported quarterly numbers.

| Metric | Altria | Philip Morris International |

| Sales | $5.43 billion (+3.2% YOY) | $10.15 billion (+9.1% YOY) |

| Net Income | $2.18 billion (+100%+ YOY) | $2.44 billion (-9% YOY) |

| Operating Cash Flow | $2.32 billion | -$399 million |

| P/E Ratio (Forward) | 12.08x | 20.44x |

| Price/Sales Ratio | 4.92x | 2.87x |

Right away, Philip Morris International is the larger company by sales, reporting a 9.1% YOY increase to $10.15 billion. Altria, meanwhile, was up 3.2% YOY to $5.43 billion.

In terms of net income, the gap narrows. Altria’s earnings more than doubled YOY to around $2.18 billion, while Philip Morris’ net income was down 9% YOY to about $2.44 billion.

Next is operating cash flow, which shows how much cash the business generated from its operations. It’s also used to pay dividends, service debt, and fund buybacks.

Altria generated $2.32 billion. Philip Morris, meanwhile, was negative at $399 million. That said, quarterly cash flow can be uneven, so it is worth watching over a longer period.

Valuation is another important difference that investors should know about. Altria trades at a P/E ratio of 12x, while Philip Morris trades at 20x. This metric shows how much investors pay per dollar of next year's earnings. The broader consumer staples sector is trading at 16x.

However, if we consider the Price/Sales, Philip Morris looks cheaper at around 3x compared to Altria’s 5x. This shouldn't be a big surprise, as Philip Morris has a bigger global footprint. Yet, overall, Altria looks cheaper and squeezes more profit out of every dollar of revenue, while Philip Morris has the advantage in sales and what could be a stronger growth story tied to smoke-free products.

Which one wins in dividend metrics?

Now, let’s talk about what could be the make-or-break case for long-term investors: dividends.

Altria pays a forward annual dividend of $4.24, which translates to a yield of around 6%. It has raised its dividend 60 times in the past 56 years, making it a Dividend King - an elite group of companies that have raised their dividends for more than 50 straight years. It also has a 76% dividend payout ratio, meaning it uses a larger portion of its income for dividend payments.

Meanwhile, Philip Morris International has increased dividends every year since 2008, which is a shorter span than Altria’s but still a good sign of consistency. The company pays $5.88 per year, which translates to a yield of approximately 3.4%. The dividend payout ratio is at 74%, slightly lower but not by a significant margin.

For investors who value dividend metrics above all else, Altria is the clear winner here, with a stronger track record and more consistent payouts.

What does Wall Street say?

Now, let’s see what the experts think.

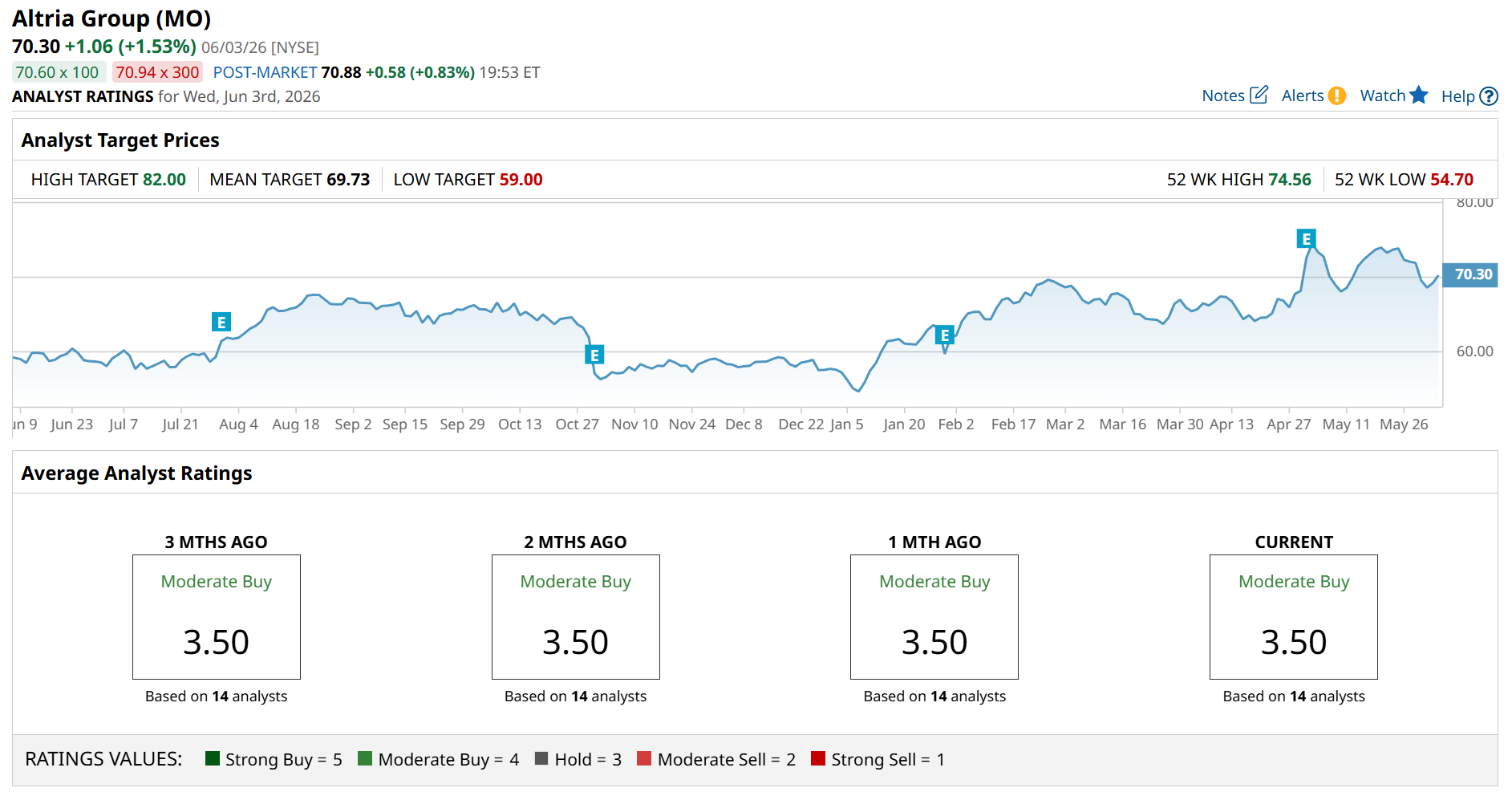

A consensus among 14 analysts rates MO stock a “Moderate Buy” with an average score of 3.50. The stock is trading just above its mean target price, while the high target price suggests up to 17% upside potential if reached.

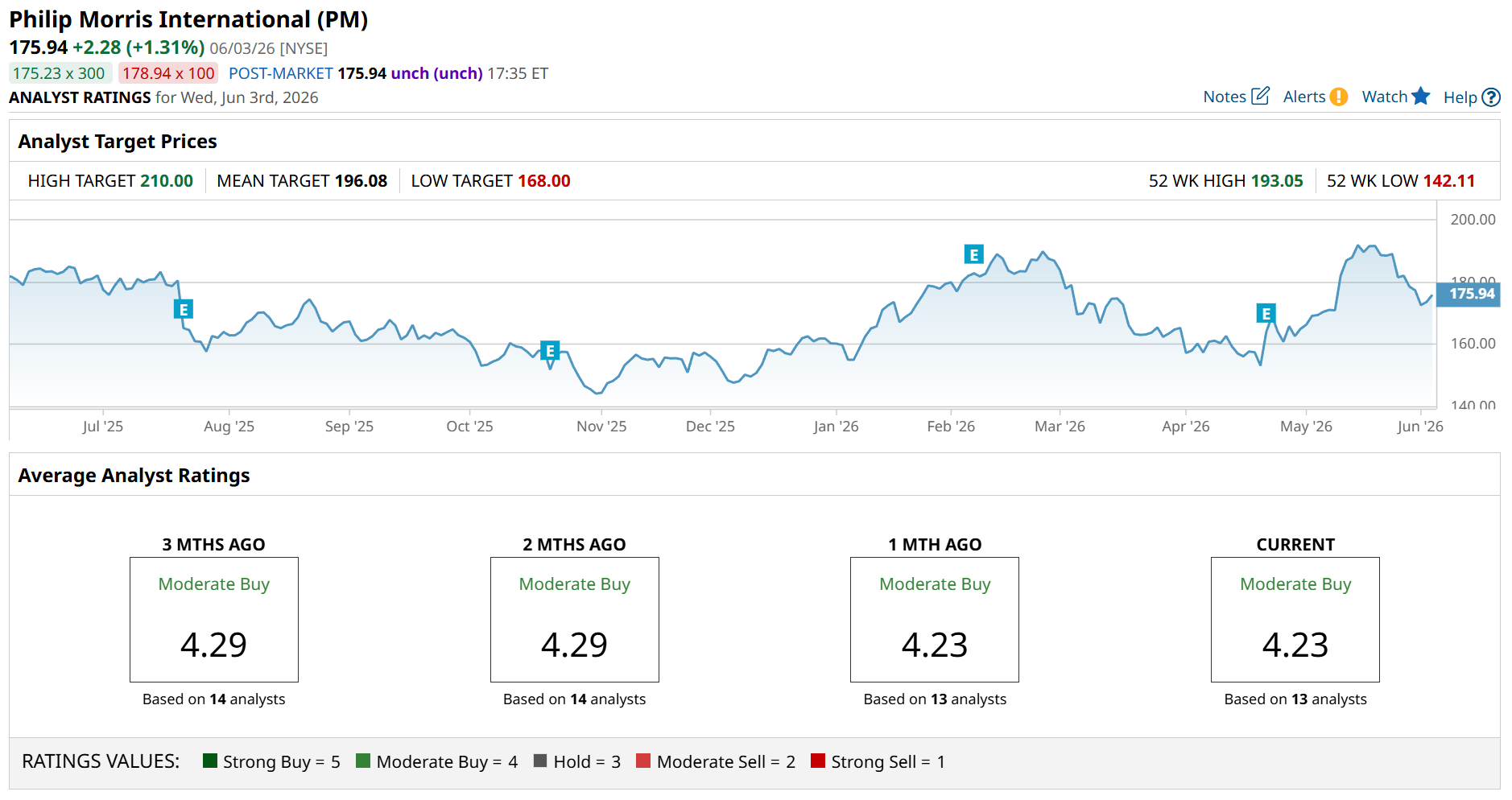

On the other hand, a consensus among 13 analysts rates Philip Morris stock a similar “Moderate Buy” rating, yet the average score is 4.23 - just a few points short of a “Strong Buy” rating. Meanwhile, its mean-to-high target prices suggest between 11% and 19% potential upside.

Final thoughts

Taking everything into account, Altria looks like the better value and income play. It trades at a lower P/E ratio, pays a much higher dividend yield, and still produces strong profits for its size. However, Philip Morris International appears to be the stronger long-term business. It has a larger global footprint, better sales growth, and a clearer path toward smoke-free products.

So, if the priority is income, Altria has the edge. But if the focus is business quality and long-term positioning, Philip Morris looks more compelling.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)