/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

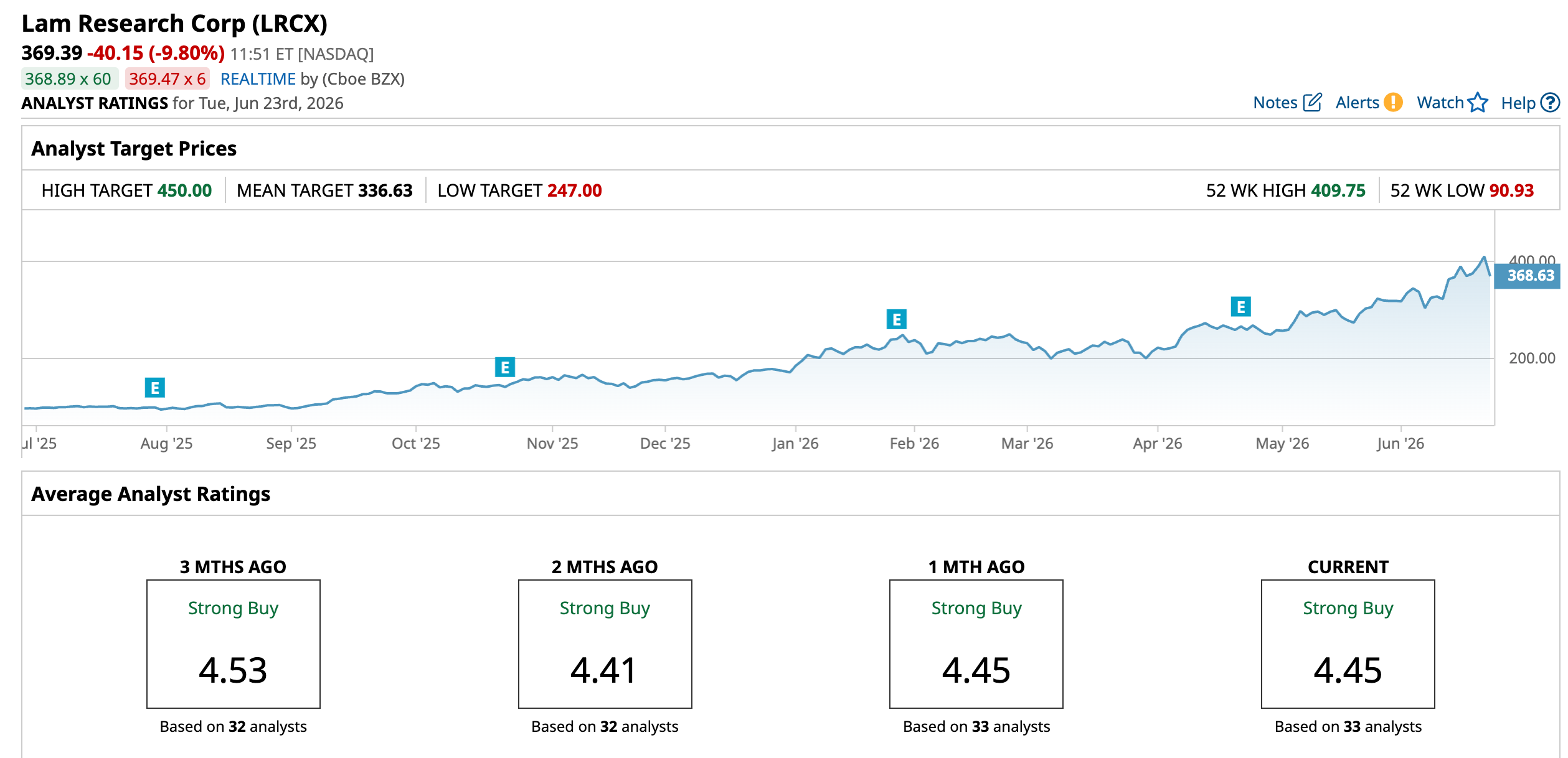

The artificial intelligence (AI) boom is reshaping the semiconductor industry, and investors are increasingly looking beyond chip designers toward the companies supplying the tools needed to manufacture next-generation processors and memory. Lam Research Corporation (LRCX) has emerged as a key beneficiary of this trend, with its stock gaining fresh momentum after Citi lifted its price target to a Street-high $450 while maintaining a bullish outlook on the semiconductor equipment sector.

Citi noted a bullish outlook for NAND equipment demand driven by the rapid expansion of AI workloads. It expects rising memory requirements from agentic AI, tighter DRAM supply, and increased adoption of solutions such as KV cache offloading to accelerate demand for NAND and semiconductor manufacturing equipment.

Also, Citi raised its wafer fabrication equipment (WFE) outlook, forecasting a potential market size of around $145 billion, $200 billion, and $250 billion in 2026, 2027, and 2028, respectively, supported by capacity expansions from prominent companies. Furthermore, it highlighted a stronger semiconductor capital spending outlook, with expectations that expanding AI infrastructure could create a multi-year growth cycle for equipment makers like Lam Research.

With Lam’s strong exposure to memory manufacturing, advanced chip production, and AI-driven semiconductor demand, investors are now watching whether the company can capitalize on a potential NAND recovery and a broader equipment upcycle that could push LRCX shares higher.

About Lam Research Stock

Lam Research is a leading global supplier of semiconductor manufacturing equipment used by chipmakers to produce advanced memory and logic chips. Headquartered in Fremont, California, Lam Research provides critical wafer fabrication solutions, including etch, deposition, and cleaning technologies that enable the production of next-generation semiconductors for applications such as artificial intelligence, data centers, smartphones, and high-performance computing.

The company has become a key player in the semiconductor equipment industry, benefiting from long-term trends including AI infrastructure expansion, rising memory demand, and increased semiconductor complexity. Lam Research currently has a market cap of $512.16 billion, reflecting strong investor confidence in its role as a major beneficiary of the ongoing semiconductor manufacturing upcycle.

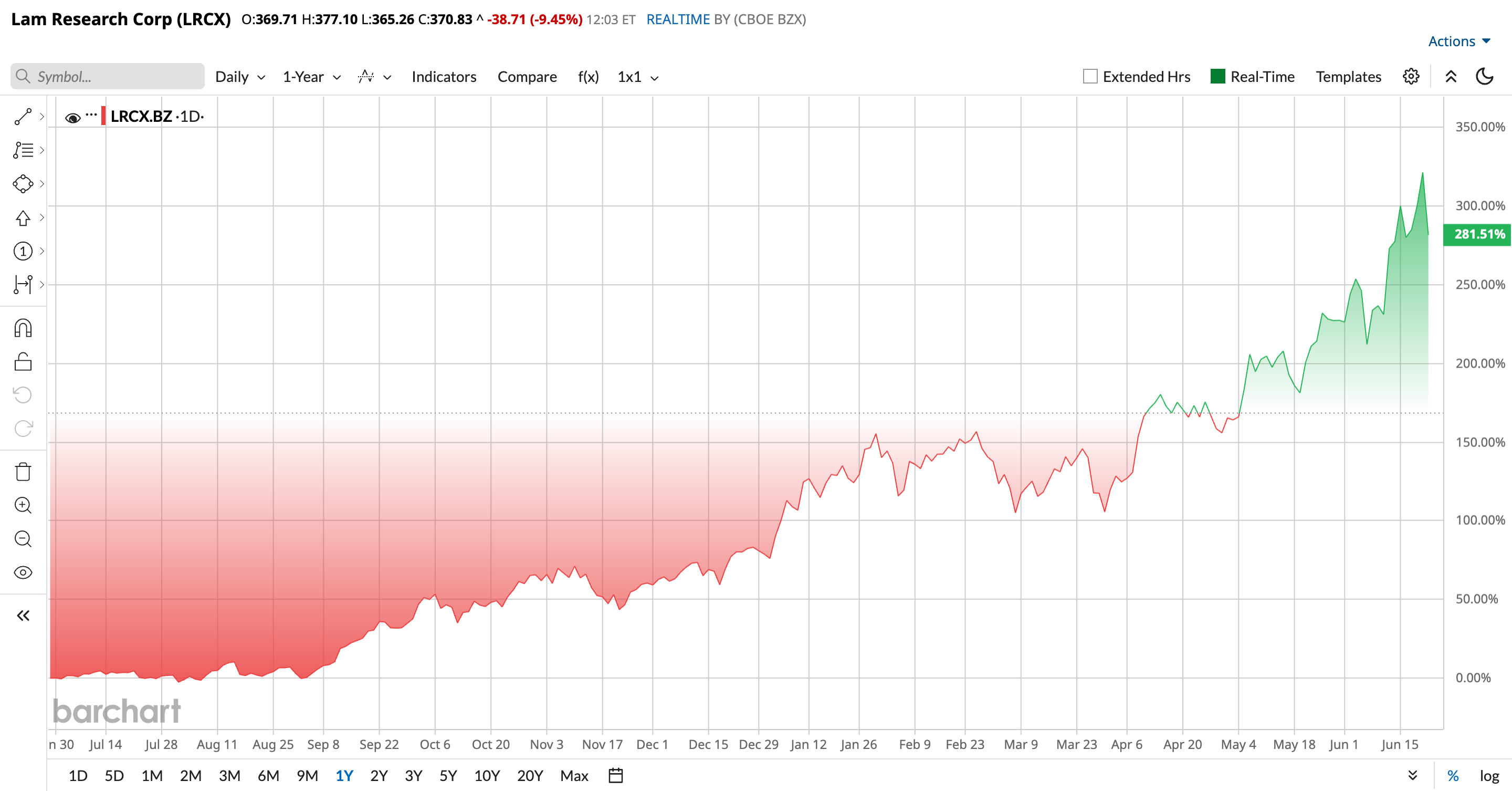

Lam Research shares have delivered a powerful rally as investors increasingly position the semiconductor equipment maker as a key beneficiary of the AI-driven chip cycle. Over the past year, LRCX stock has gained 301.3%, reflecting strong optimism around rising semiconductor capital spending, memory recovery, and growing demand for advanced wafer fabrication equipment. Year-to-date (YTD), shares have climbed 114.8%, significantly outperforming the broader market as investors anticipate a sustained upcycle in AI infrastructure and semiconductor manufacturing.

Momentum has accelerated in recent weeks, with Lam Research gaining 20.4% over the past month as improving NAND demand expectations and bullish analyst commentary boosted sentiment. The stock also reached a new high of $409.75 on June 22, while closing at $409.54 after rising 5.27% during the session, as investors reacted positively to the improving outlook for semiconductor equipment demand.

The rally has been fueled by expectations that AI workloads will drive a structural increase in memory demand, benefiting Lam’s exposure to NAND, DRAM, and advanced semiconductor manufacturing technologies. Citi’s decision to raise its price target on Lam Research to a Street-high $450 further strengthened the bullish case, with the firm pointing to a potential multi-year wafer fabrication equipment expansion cycle.

The stock is evidently trading at a premium valuation compared to its industry peers at 68.24 times forward price-to-earnings.

Solid Quarterly Performance

Lam Research delivered a strong performance for the fiscal third-quarter ended March 29, reinforcing its position as a major beneficiary of the AI-driven semiconductor equipment cycle. The company released results on April 22.

For the March 2026 quarter, Lam reported revenue of $5.84 billion, up 23.7% year-over-year (YOY) from $4.7 billion in the prior-year period, driven by stronger demand for wafer fabrication equipment supporting AI, memory, and advanced logic production. Non-GAAP EPS came in at $1.47, increasing 41.3% YOY, and exceeding the consensus estimate.

Key profitability metrics also improved with non-GAAP gross margin reaching 49.9%, supported by a favorable product mix and execution efficiency. Operating margin was 35%, highlighting strong cost discipline as revenue expanded. Net income rose to to $1.825 billion, compared with about $1.6 billion in the previous quarter, showing continued earnings momentum.

The company’s geographic revenue mix remained diversified, with China contributing 34% of revenue, followed by South Korea and Taiwan at 23% each, reflecting continued demand from leading semiconductor manufacturing regions.

Furthermore, Lam provided a strong outlook for the June 2026 quarter, guiding for revenue of around $6.6 billion and non-GAAP EPS of approximately $1.65. Management emphasized that AI-driven semiconductor demand, expanding memory requirements, and investments in next-generation chip manufacturing are creating strong growth opportunities.

Analysts expect the company’s EPS to improve 37.7% YOY to $5.70 in fiscal 2026 and rise another 37.7% to $7.85 in fiscal 2027.

What Do Analysts Expect for Lam Research Stock?

In addition to Citi, several other analysts have also boosted price targets and strengthened their bullish stance. This month, Cantor Fitzgerald raised its price target on Lam Research to $425 from $320 while maintaining an “Overweight” rating, citing strong long-term growth drivers from AI-related semiconductor demand. The firm highlighted AI-driven logic investments, advanced packaging, and HBM expansion as key catalysts for wafer fabrication equipment growth.

Also, last month, Mizuho raised its price target on Lam Research to $380 from $330 while maintaining an “Outperform” rating, citing a stronger semiconductor equipment outlook driven by AI and memory demand.

Meanwhile, Morgan Stanley upgraded Lam Research to “Overweight” from “Equal Weight” and raised its price target to $331 from $293, amid stronger growth expectations from a NAND recovery.

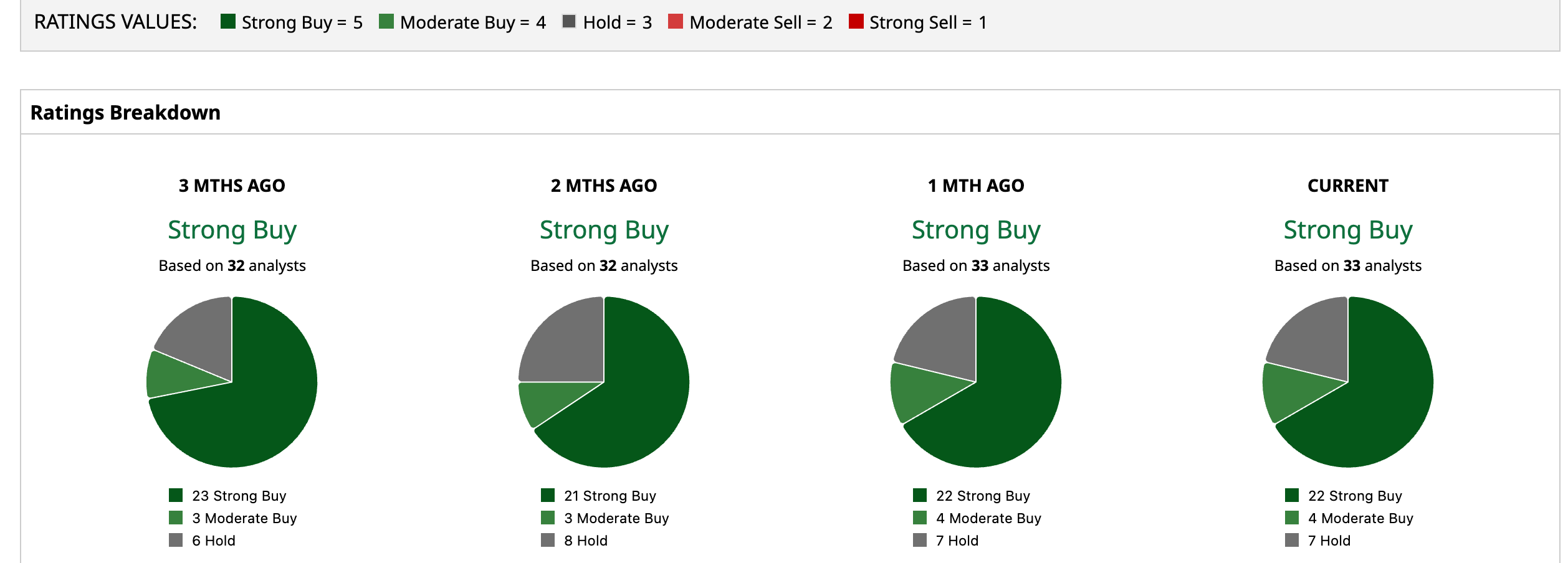

Overall, LRCX has a consensus “Strong Buy” rating. Of the 33 analysts covering the stock, 22 advise a “Strong Buy,” four suggest a “Moderate Buy,” and the remaining seven analysts give a “Hold” rating.

The stock has already surged past the average analyst price target for LRCX of $336.63, while Citi’s Street-high target price of $450 suggests that the stock could rally as much as 21.8%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)