/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

Micron Technology (MU) shares are ripping higher ahead of the memory chipmaker’s Q3 earnings scheduled for June 24 after market close.

Analysts expect MU to nearly quadruple its third-quarter revenue to roughly $35 billion on a more than 10x increase in adjusted per-share earnings to $20.81.

Still, options pricing currently signals a post-earnings pullback in Micron stock, which is already up a remarkable 280% versus the start of this year.

Where Options Data Suggests Micron Stock is Headed

According to Barchart, the put-to-call ratio on options contracts expiring June 26 sits at 0.99x at the time of writing, indicating traders aren’t particularly bullish for the near term.

The lower price on those contracts sits at $1,060 currently, signaling potential for a more than 11% decline in MU shares almost immediately after the quarterly print.

Additionally, Micron’s relative strength index (RSI) is hovering around 70 today, suggesting the stock is about to hit overbought conditions that often trigger a pullback.

It's also worth mentioning that MU has a history of losing more than 2% on average in July, a seasonal pattern that reinforces the near-term downside risk.

Bernstein Still Recommends Buying MU Shares

Bernstein’s senior analyst Mark Li doesn’t really agree with the derivatives market on MU, though.

He maintained an “Outperform” rating on Micron shares this morning and raised his price target aggressively to $1,300, signaling potential upside of another 9% from here.

Li’s research note attributed the constructive view to “increased forecasts of conventional memory pricing as well as HBM (high bandwidth memory) pricing going forward.”

The bullish call arrives on the heels of MU’s strategic partnership with Anthropic, which offers strong visibility into the company’s future revenue growth.

Note that Micron does currently pay a small dividend yield of 0.05% as well.

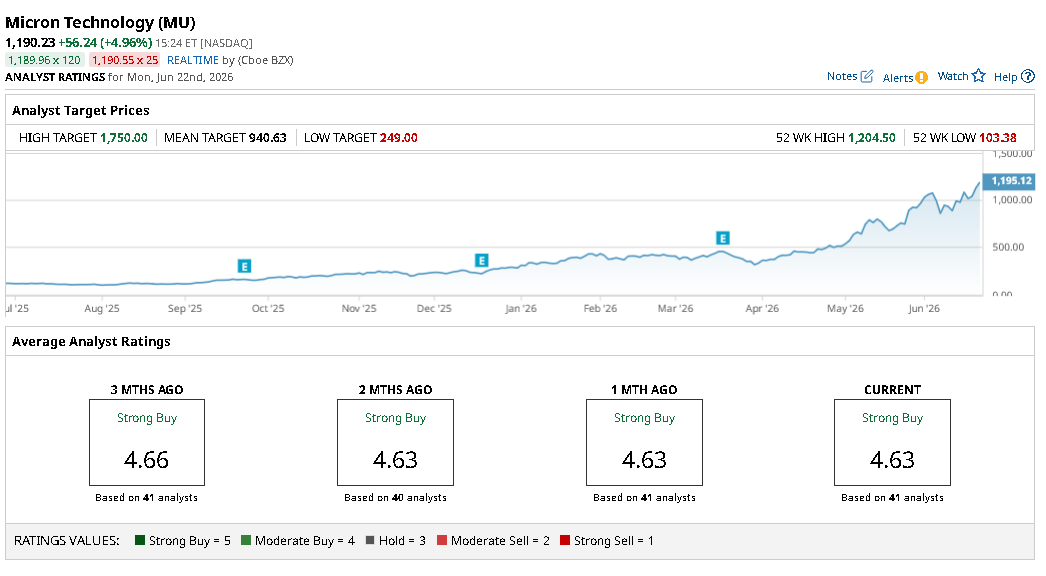

What’s the Consensus Rating on Micron Technology?

Some Wall Street analysts, however, do not share Li’s optimism on MU stock for the remainder of 2026.

While the consensus rating on Micron Technology remains at “Strong Buy” currently, the mean price target of $940 suggests the company is overvalued by more than 25% at the time of writing.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)