/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

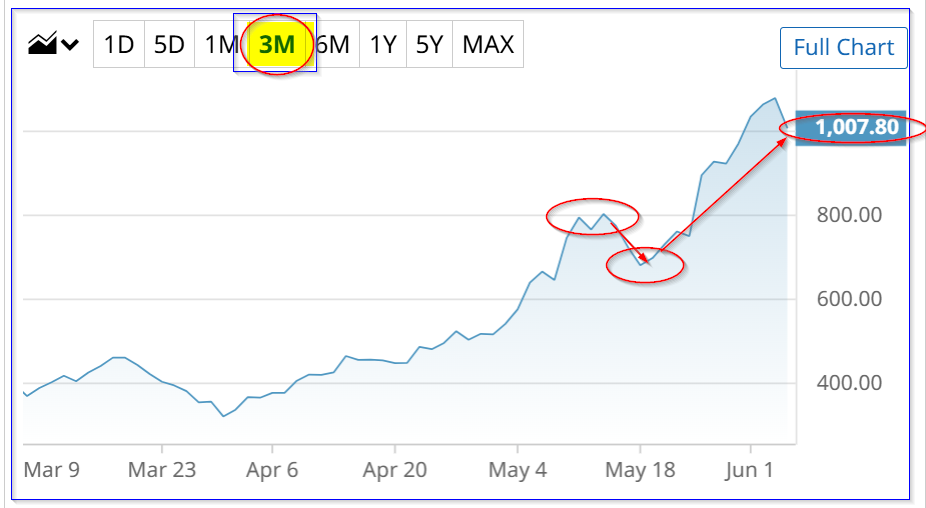

Micron Technology (MU) stock may have peaked as it is off its recent highs. At over $1,000 per share, it is well over most analysts' price targets. One issue is how analysts and the market are valuing Micron's expected free cash flow (FCF). This article will discuss that issue.

MU is at $1,022 in midday trading on Thursday, June 4. That is off its recent closing price peak of $1,079.57 on June 3. However, since its recent May 13 peak of $803.63 (and later slide to $681.54 on May 18), MU stock has spiked +27%. It's still up over 50% since the May 18 trough. But can it keep climbing at this rate?

Updated Price Targets for MU Stock

In my May 24 Barchart article, “Micron Stock is Up over 133% From Its Lows - But Is MU Still Undervalued?” I showed that MU stock was worth $843.75 per share. That was equivalent to a $906 billion market valuation.

But that was after using analysts' next revenue estimates of $172.76 billion, a 28.85% free cash flow (FCF) margin, and a 5.5% FCF yield. Since then, analysts have raised their revenue forecasts.

So, using new estimates of $176.41 billion, a 29% FCF margin estimate (slightly higher), and a lower 5.0% FCF yield (slightly better), Micron could be worth over $1.02 trillion:

$176.41b x 0.29 = $51.16 billion FCF FY 27

$51.16b / 0.05 = $1,023 billion (i.e., $1.023 trillion)

That compares with its market cap today of $1.137 trillion, according to Yahoo! Finance. In other words, MU stock is worth 10% less than its existing market value:

1,012 x 0.90 = $910.80 per share price target (PT)

The problem is that MU is still well over analysts' price targets (PTs). This is even though they have been raising these PTs as MU continues to move higher.

For example, analysts surveyed by Yahoo! Finance have an average PT of $739.47, up from $613.22 on May 24 (in my last Barchart article). Similarly, Barchart's PT is now $739.34, and AnaChart's survey, which typically includes more recent analyst write-ups and fewer legacy or unupdated recommendations, is $631.65.

Issues with Micron's Valuation Methodology

One problem with MU's stock valuation, and particularly why there could still be significant upside, is the multiple that analysts are using to value its FCF.

For example, it is not uncommon for many technology stocks, especially in the hardware side of AI-demand-driven stocks, to have a 3.0% FCF yield metric, or lower.

For example, Nvidia generated slightly over $119 billion in trailing 12-month (TTM) free cash flow, according to Stock Analysis. Today, its market cap is $5.298 trillion. So, its FCF yield is:

$119b / $5,298 = 0.02246/100 = 2.246% FCF yield

This means that, theoretically, if Nvidia were to pay out 100% of its FCF to shareholders in dividends (even though it does so with buybacks as well), the dividend yield would be 2.246%.

That is less than half the 5.0% FCF yield that I am using for the Micron valuation. In other words, using a 2.5% FCF yield metric, MU could be worth over twice its present market value:

$51b FY 27 FCF / 0.025 = $2,040 billion (i.e., $2.04 trillion)

Analysts and the market have been reluctant to value Micron and other memory product makers at this lower FCF yield. They don't expect that Micron would eventually have a 2.5% dividend yield (assuming a 100% FCF payout), vs. its present 5.0% yield.

One reason is that the industry has been very cyclical. For example, as soon as the industry builds out capacity to meet present AI-driven demand, memory device prices could drop considerably.

Ultimate Potential Upside

However, if the market determines that device demand is set to continue climbing over the next 3 to 5 years, rather than just 1 to 3 years, the valuation metric could start to rise towards a 3.0% FCF yield or so.

That shows that a potential upside for Micron over the next year could be startlingly higher.

For example, let's say that in one year Micron's expected FCF is $65 billion in the following year (FY 28) and the market is willing to give Micron a 3.0% FCF yield:

$65b / 0.03 = $2,167 billion (i.e., $2.167 trillion)

That is still 91% higher than Micron's valuation today of $1.137 trillion. In other words, Micron's PT next year could be $1,952 (i.e., $1.91 x $1,022 price today).

And during this whole period, analysts will constantly be playing catch-up with their target prices, as they may not be willing to give Micron a similar FCF yield to Nividia, or even close to it.

So, the bottom line here is that if AI-driven demand continues to drive up memory device prices higher than the market expects, Micron's FCF yield will keep falling. That will push its valuation higher.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)