/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)

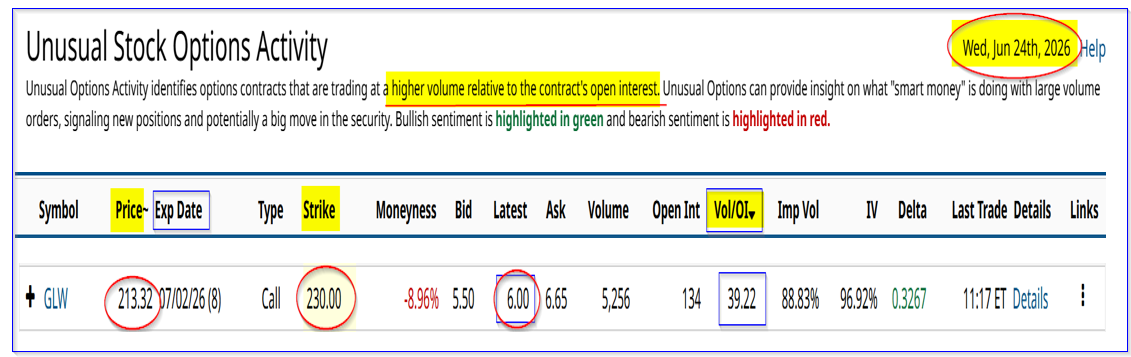

Corning, Inc. (GLW) stock is up over 10% today, and Barchart reports huge, unusual GLW call options volume in a nearby expiry period for an out-of-the-money strike price. Investors can't get enough of GLW stock.

GLW is at $216.16 today, up over 10% and over 28.5% since June 10 ($168.17), after Corning announced a new manufacturing collaboration deal with Amazon (AMZN) on June 8 for fiber optics related to data centers and AI-related demand.

As a result, Barchart reports that investors have been piling into GLW call options today. The Barchart Unusual Stock Options Activity Report shows that over 5,200 call option contracts have traded at the $230.00 strike price expiring in just 8 days (July 2).

This volume is over 39 times the prior number of outstanding call options at that strike price. It indicates that investors are buying large amounts of these call options and willing to pay at least $6.00 for these calls (at the midpoint).

That implies that the buyers believe GLW will be over $136.00 by the close on July 2 - i.e., a 9.17 gain by then. Moreover, short-sellers, especially covered call sellers, are able to make a good yield: 2.775% (i.e., $6.00/$216.16) over 8 days.

Both of these situations imply that investors are very bullish on GLW stock and believe it has further upside.

Given that the stock is up over 10% today alone, that seems possible. But let's also look at what the stock could be worth.

Strong Revenue and FCF Outlook

Analysts have raised their revenue prospects from $18.94 billion forecast for this year ending Dec. 31, 2026, to $22.51 billion next year. This represents an acceleration of sales (i.e., 18.85% growth in 2027 vs.16.4% growth in 2026).

As a result, we can expect its operating cash flow (OCF) and free cash flow (FCF) could move significantly higher, including the underlying margins.

For example, over the past 12 months (TTM), as of June 30, Corning generated $3.69 billion and $1.95 billion in OCF and FCF, respectively (Stock Analysis data). That was 22.6% and 11.95% of its trailing 12-month revenue of $16.321 billion.

As a result, if we assume a 25% OCF margin next year, less $2.00 billion in capex (i.e., 15% higher than $1.74 billion in the TTM period), its FCF could hit

$22.51b x 0.25 = $5.6275b operating cash flow (OCF)

$5.6275b OCF - $2.00b capex = $3.6275b FCF

That represents an 86% potential gain in FCF over the next year. This could push the stock significantly higher.

Corning's Fair Market Value (FMV) and Price Targets (PTs)

For example, if we assume that Corning were to pay out 100% of its FCF, its dividend yield would have been about 1%, given Corning's market value of $182.5 billion (Yahoo! Finance):

$1.95b FCF TTM / $182.5b = 0.0168 = 1.068% FCF yield

Therefore, using the 2027 FCF forecast of $3.63 billion, its fair market value (FMV) is $363 billion:

$3.63b FCF / 0.01 = $363 billion FMV

That is almost double its value today:

$363b / $182.5b = 1.989

In other words, GLW's price target could be as much as $430 per share:

$216.16 x 1.989 = $429.94 PT

In fact, even if some of my assumptions are relaxed, its minimum PT is at least 74% higher. For example, using a lower 23% OCF margin with a $2 billion capex, its PT would be 74% higher:

$22.51b x 0.23 = $5.1773 billion OCF - $2.0b capex = $3.1773b FCF

$3.1773b / 0.01 = $317.7 billion FMV

$317.7 FMV / $182.5b today = 1.74 -1 = 74% upside

PT = 216.16 x 1.74 = $376.12 per share

The bottom line is that GLW is worth between $376 and $430, or about $400 per share. That could be why investors are so bullish today and why there is so much unusual call options activity.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.