Netflix (NFLX) stock hit its 52-week low today and is down over 23% for the year. The streamer has looked weak after peaking in the first half of 2025 and has since lost nearly 46% of its market cap. Nothing has seemed to work for Netflix over the period. NFLX stock fell in the back half of 2025 after the company announced its intent to buy Warner Bros. Discovery’s (WBD) assets, which markets believed would leave it saddled with too much debt. The company eventually walked away from the deal, which led to a short-term spike in the stock, but recently it has fallen after reports that it lost out in its bid to acquire Roku (ROKU), which would be acquired by Fox (FOX).

Previously, Netflix shares rallied spectacularly in 2023 and 2024. The gains were preceded by a brutal 2022, when U.S. tech stocks plummeted. However, while the broad-based tech rally in 2023 supported Netflix’s price action, markets gave a thumbs-up to its ad-supported plan and password-sharing crackdown. Thanks to these measures, Netflix—which lost subscribers in the first half of 2022—added nearly 100 million new subscribers between 2023 and 2025. Many of the new members are getting onboarded on the cheaper ad-supported plan.

Meanwhile, Netflix has been out of favor with the markets for almost a year now. There are apprehensions about the company’s earnings outlook in the back half of the year since the management did not raise 2026 guidance despite a beat in Q1. There is also a leadership transition at the company as Chairman Reed Hastings is stepping down from his position this month.

The Bullish Thesis for Netflix

On a more structural note, Netflix hasn’t had any compelling story to sell to markets after the password-sharing crackdown and ad-supported tier, both of which have largely run their course. While Netflix is dabbling with artificial intelligence (AI), it won’t be a major trigger for the stock, as I noted in my previous article. I, however, see NFLX as a good buy at these levels. Here’s my bullish thesis for the stock.

- Ad Revenue Growth: During its Q4 2025 earnings call earlier this year, Netflix disclosed that the average revenue per user (ARPU) on the ad-supported plan was lower than the standard plan without ads. However, the company stressed that the gap is narrowing, and it expects that to close over time as it improves ad capabilities. Netflix’s ad revenues are growing at a stellar pace, albeit on a low base, and the management expects them to double to about $3 billion this year. While that is less than 6% of the total revenue analysts expect the company to post this year, the contribution should rise gradually as Netflix adds more members to the ad-supported tier and monetizes its growing user base efficiently.

- Margin Expansion: Netflix has proved its moat in the streaming space through regular price hikes. The price hikes, ad revenue growth, and member additions should help drive double-digit annualized top-line growth for Netflix in the medium to long term. Netflix is also a margin expansion story as it aims to keep content spending growth below revenue growth. The streaming industry has high operating leverage, as content and technology costs are largely fixed, and revenues from new members help expand margins.

- New Initiatives: Netflix still has much untapped potential from new initiatives like video gaming, which the management sees as a $140 billion market globally (excluding ad revenues), excluding China and Russia. Merchandise sales could also start contributing significantly to Netflix’s growth as the company ramps up original intellectual property (IP). No wonder the management wanted to acquire WBD’s IP, as it would have added franchises like Harry Potter to its arsenal.

- Reasonable Valuations: Netflix trades at a forward price-to-earnings (P/E) of 20.25x, which is below what its average S&P 500 Index ($SPX) peer trades at. I see a good margin of safety in NFLX at these levels.

NFLX Stock Looks Like a Buy

All said, I believe markets are currently in the AI FOMO trade, and tech companies that either don’t have an AI story to sell or, worse, are seen as net AI losers have been out of favor. However, at these levels, I find NFLX stock a good buy and expect it to deliver strong returns over the next couple of years once the market’s obsession with AI cools off.

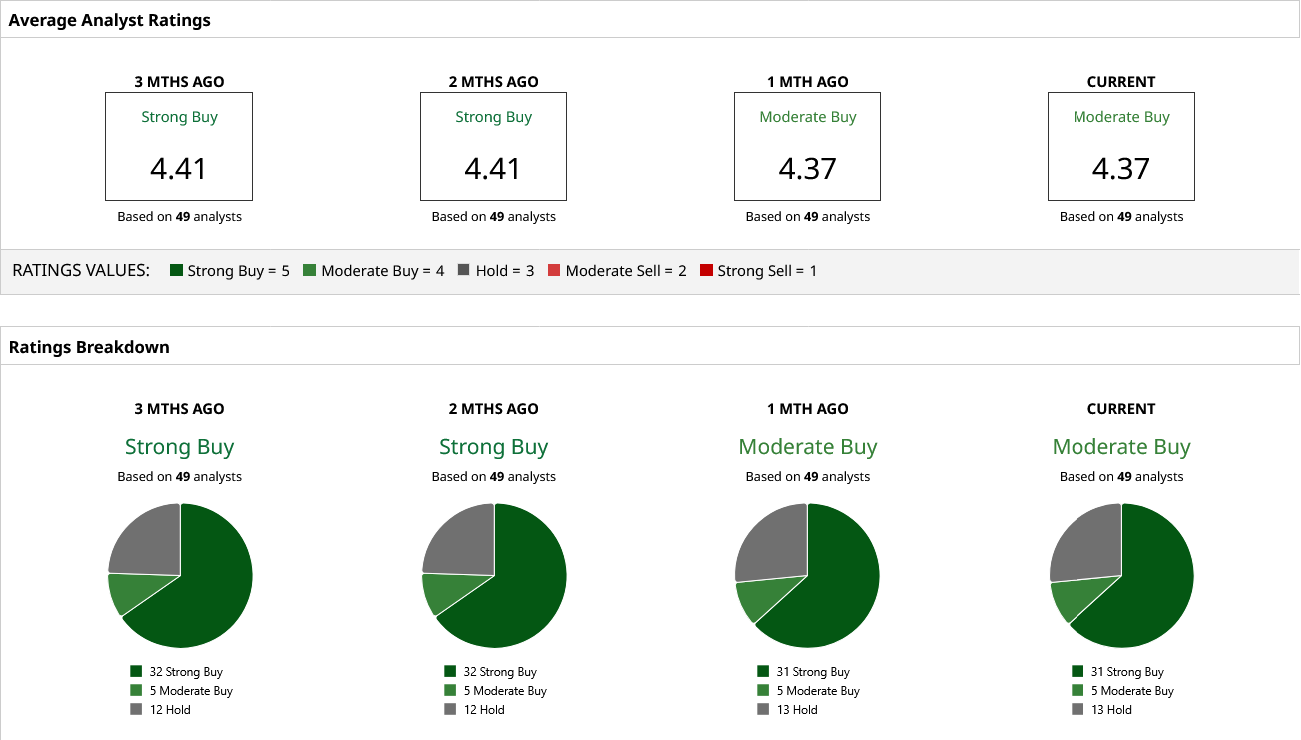

Analysts seem to agree. NFLX holds a consensus “Moderate Buy” from the 49 analysts that cover the name.

On the date of publication, Mohit Oberoi had a position in: NFLX. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)