/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

Netflix’s (NFLX) revenue growth continues to be driven by three core factors, including expanding membership, higher subscription pricing, and growing advertising revenue. Recently, the company raised prices across all its subscription plans in the U.S., a move expected to strengthen both revenue and earnings.

A key factor behind this pricing flexibility is Netflix’s extensive and continually refreshed content portfolio and higher engagement. High-quality programming drives engagement on the platform, helps retain subscribers, and enables the company to raise prices while keeping churn relatively low.

Management highlighted this momentum during the fourth-quarter conference call, noting that total view hours in the second half of 2025 increased 2% year-over-year (YoY). This represented an acceleration compared with the 1% growth recorded in the first half of the year, suggesting that engagement on the platform continues to trend upward.

Netflix also maintains one of the strongest retention rates in the streaming industry. In the most recent quarter, the company reported a YoY improvement in churn. At the same time, membership growth remained strong, strengthening the platform’s competitive positioning.

Netflix’s ability to increase prices while keeping churn low shows Netflix’s pricing power. Moreover, Netflix’s focus on growing content spending at a slower pace than revenue growth will help expand margins, supporting NFLX’s investment case.

Netflix’s Pricing Power and Advertising Push Support 2026 Outlook

Netflix is set to deliver another year of solid earnings growth, even as the company continues investing in content and product development. The streaming giant’s underlying fundamentals remain strong, supported by steady pricing power, expanding membership, and the rapid growth of its advertising business.

A recent price increase is expected to contribute meaningfully to both revenue and earnings. At the same time, viewer engagement remains high on its platform, driven by a robust slate of original programming and an expanding mix of licensed content.

Notably, strong content will likely translate into sustained subscriber growth and improved retention, strengthening Netflix’s long-term revenue potential. Pricing continues to be an important lever for the company. With a loyal global audience and consistent demand for its content, Netflix has demonstrated the ability to raise prices without significantly affecting user growth, thereby supporting higher revenue and profitability.

Advertising is also becoming an increasingly important contributor to the company’s growth strategy. Netflix’s ad-supported tier has gained traction since its launch, helping broaden the platform’s revenue base. Advertising revenue reached $1.5 billion in 2025, and management is targeting around $3 billion in ad sales for 2026, highlighting the rapid expansion of this segment.

While pursuing new growth opportunities, Netflix is also focusing on improving profitability. Management is targeting operating margins of roughly 31.5% in 2026, up 200 basis points from the previous year. This margin expansion is expected to be supported by disciplined cost management, including content spending that will grow slower than overall revenue.

Looking ahead, Netflix forecasts 2026 revenue between $50.7 billion and $51.7 billion, representing growth of 12% to 14%. Analysts expect Netflix’s EPS to increase by more than 24% in 2026. Moreover, this will be followed by another 23% growth in 2027, reflecting revenue growth, advertising expansion, and improving margins.

Is NFLX Stock a Buy Now?

Netflix has shown that it can implement subscription price increases without significantly weakening consumer demand. This ability to raise prices while maintaining subscriber engagement supports the company’s revenue growth and strengthens the durability of its earnings trajectory.

The streaming giant is expected to deliver strong earnings in the coming years. Moreover, NFLX stock trades at 29.7 times forward earnings, which is reasonable and provides an entry point for investors. Netflix’s steadily growing global membership base, increasing traction in the ad-supported subscription tier, and improving operating leverage are expected to support earnings and share price.

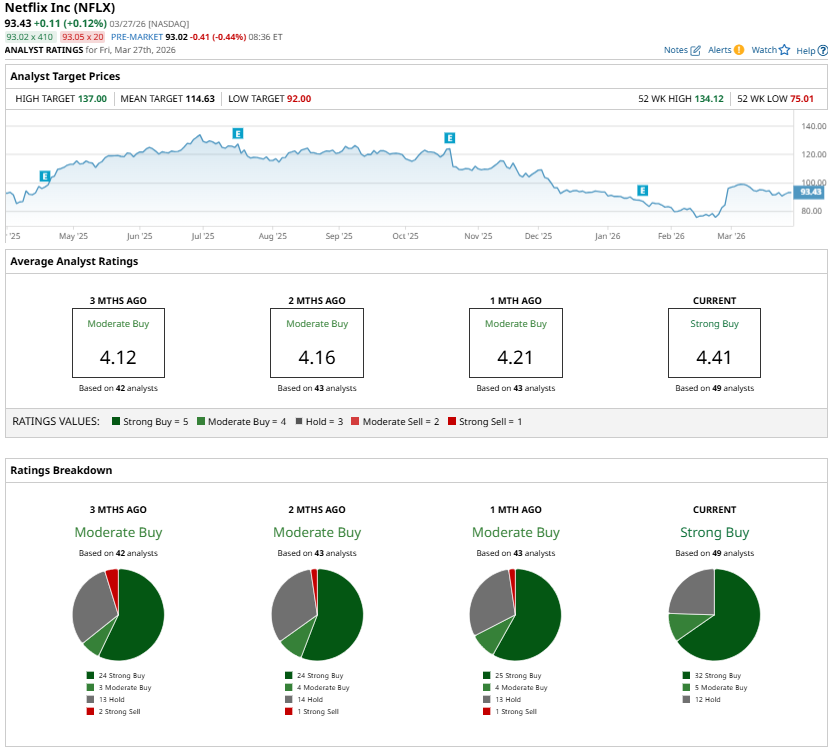

Analysts broadly maintain a “Strong Buy” consensus rating on NFLX stock, reflecting confidence in the company’s growth outlook.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)