/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

I recently covered how the market was waking up to Advanced Micro Devices’ (AMD) Agentic AI potential and how the company’s CEO was proactive in developing the underlying supply chain to fulfill the rising demand. It is worth looking deeper into how AMD got into a position to benefit from the agentic AI boom and started directly threatening Nvidia (NVDA). There are two main reasons why Nvidia should feel threatened by Lisa Su’s company as artificial intelligence buildout progresses.

Reason #1: Taking CUDA Out of the Equation

Nvidia’s moat isn’t the GPUs or the networking equipment it sells. Its moat is the CUDA software, which locks customers in and forces them to use Nvidia’s hardware. The company has been at it for nearly two decades now, so it’s hard for enterprises to trust another hardware vendor when the accompanying software was nonexistent. AMD is changing that, and it is changing it fast. The company’s Radeon Open-Compute (ROCm) open-source software is directly comparable to Nvidia’s CUDA and has been in development for 10 years now. It was always a distant second to CUDA, which is why Nvidia’s moat has remained so strong over the years. However, that gap is narrowing, and Nvidia bulls know it.

Things have changed in the last year or so. First, companies are looking at ways to diversify away from their reliance on Nvidia. ROCm offers a way out. It is portable across different accelerators as the code written on ROCm can be cross-compiled to run on different hardware, even on Nvidia’s. For customers locked into Nvidia’s CUDA ecosystem, this could offer a potential way out while also keeping the door open for the deployment of the best hardware at any point. It would only be a tailwind in the beginning, and it would be up to the AMD engineers to ensure this opportunity turns into a long-term success.

Moreover, ROCm has already received a vote of approval for mass deployment from Microsoft (MSFT) and Oracle (ORCL), with Meta (META) about to follow. If AMD’s ROCm ecosystem is being deployed at this scale, it is great news, especially since AMD already has the advantage of cost and availability.

Reason #2: AMD’s Rack-Scale Solutions

AMD has also been waging a war on the rack-scale solutions front. Previously, the company was just focused on being a component vendor. Its Helios rack-scale solution is now directly challenging Nvidia, even though it is at an early stage.

The upcoming Verano CPUs, built specifically for AI workloads, could further boost Helios’ profile as the rack-scale solution of choice. Managers across enterprises will also keep a keen eye on this. Even though Nvidia’s chips offer the lowest cost per million tokens, they are expensive. AMD could offer a lower entry point, and once its products gain traction, it could expand to larger customers, especially those that are already using its products.

About Advanced Micro Devices Stock

Advanced Micro Devices is a semiconductor company operating through the Embedded, Data Center, and Client & Gaming segments. The company’s product portfolio includes graphics processing units (GPUs), artificial intelligence (AI) accelerators, system-on-chip (SoC) products, and microprocessors. It supplies products and services to public cloud service providers, distributors, original equipment and design manufacturers, system integrators, and add-in-board manufacturers.

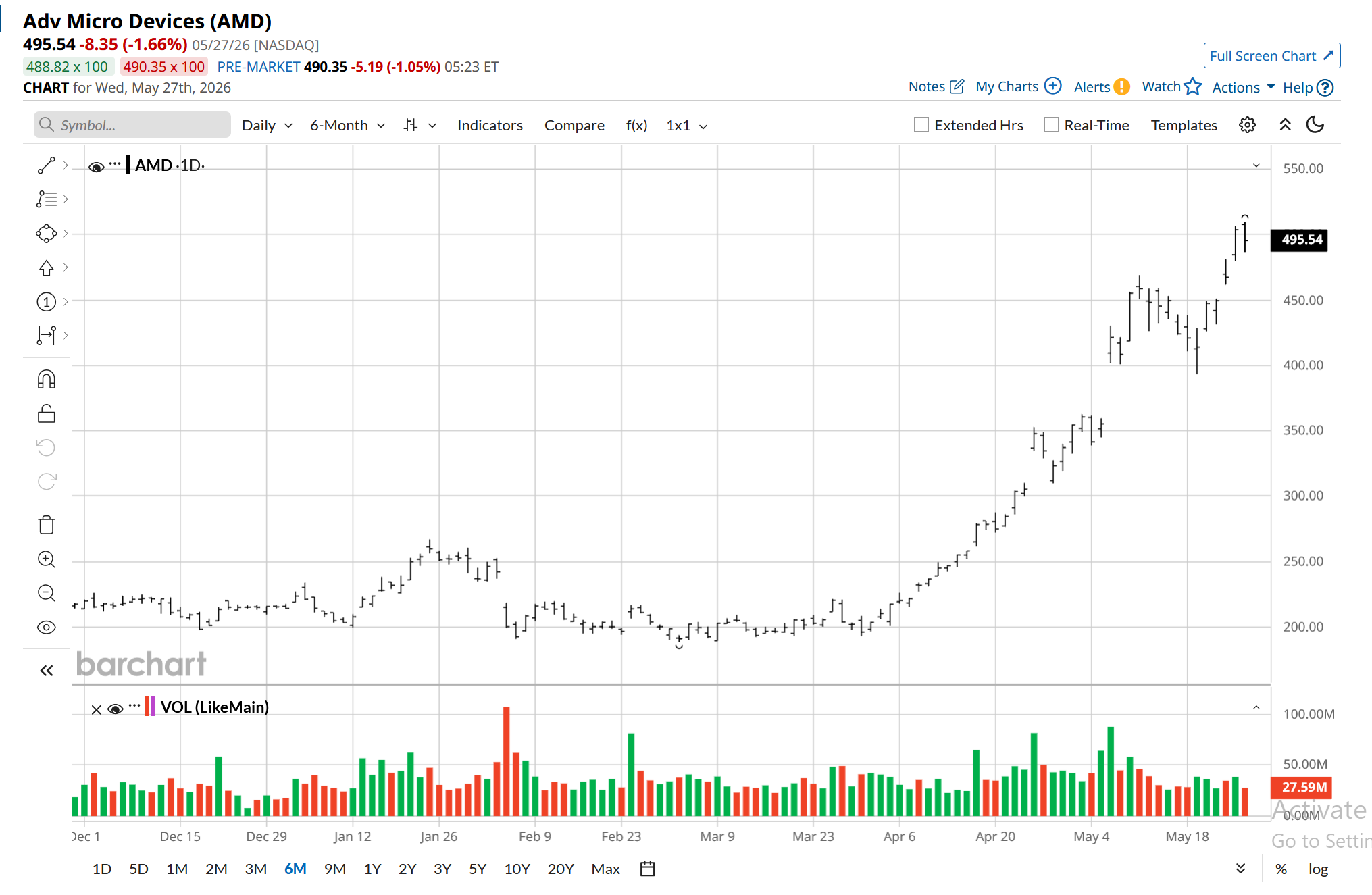

Over the past year, the stock surged more than fourfold, gaining around 345%. It remained relatively stable for much of the year before rallying sharply again in recent weeks. In comparison, the iShares Semiconductor ETF (SOXX) gained about 170% during the same period. Advanced Micro Devices has maintained strong upward momentum this year as well, with the stock more than doubling year-to-date, while the iShares Semiconductor ETF is up approximately 80%.

Advanced Micro Devices Reports a Strong Quarter

As reported on May 5, Advanced Micro Devices delivered a strong start to the fiscal 2026. Data center revenue grew 57% year-over-year, serving as a key growth driver. Total revenue for the quarter came in at $10.3 billion, reflecting a 38% year-over-year increase. Cash generation also remained strong, with $3 billion from continuing operations and a record $2.6 billion in free cash flow, representing 25% of revenue. At the end of the quarter, it had $12.3 billion in cash, cash equivalents, and short-term investments.

Looking ahead, the company expects strong growth in the server CPU market. It sees the total addressable market growing at more than 35% each year and expects it to cross $120 billion by 2030. For the second quarter, server CPU revenue is projected to grow by over 70% year-over-year. To meet rising demand, the company is increasing capacity with its supply chain partners. It is expanding both wafer and back-end production to support higher server CPU demand.

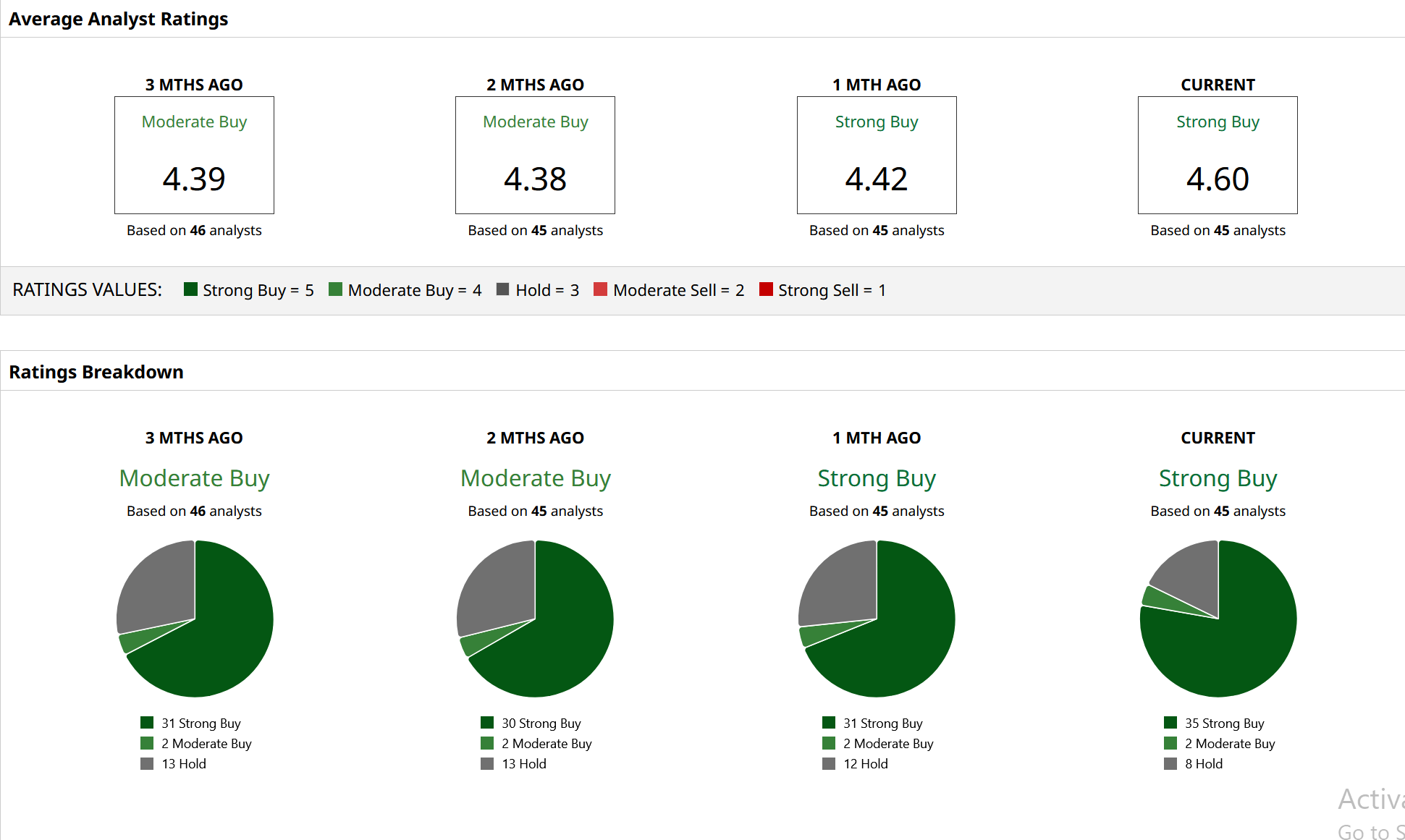

What Are Analysts Saying About Advanced Micro Devices Stock?

Since the May 5 earnings report, almost every analyst has revised their price target on AMD stock upward. The stock has reacted accordingly and now sits comfortably above the average Wall Street price target of $460.40. Even though the highest price target of $625 already looks attractive enough, it too could be a conservative estimate if the bull thesis I have pointed out above materializes.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)