/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

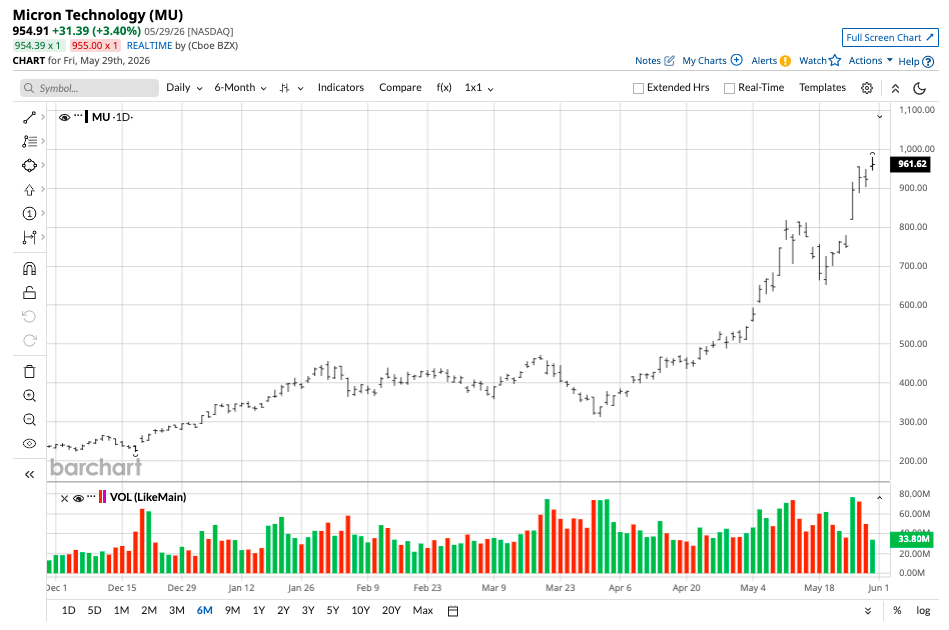

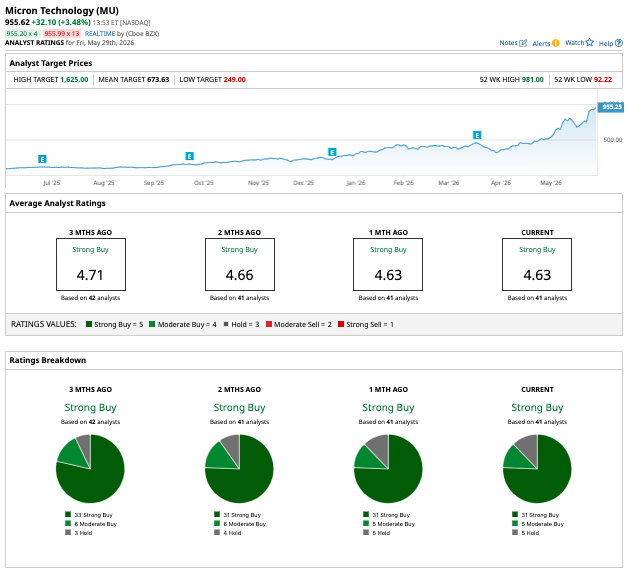

Last October, I recommended buying Micron (MU) shares. At that time, the stock was trading around $200. My thesis was built on the fact that a memory deficit for AI infrastructure was approaching, and the company was at the very beginning of a structural transformation. Since then, the shares have grown more than fourfold, and the company's capitalization crossed a historical milestone of $1 trillion. My forecast came true, and those who listened received an excellent profit. But right now, when euphoria reigns on Wall Street, and money is pouring into the stock, I want to say the main thing: It's time to take your foot off the gas.

The market is committing a classic mistake. First, it undervalues the company for a long time, and then falls into a stage of mad revaluation, extrapolating a temporary success into infinity. Today, they are buying Micron as if it were the new Nvidia (NVDA), but this is a fundamental delusion.

What Is the Difference Between Micron Today and Nvidia Three Years Ago

Investors look at the explosive growth of Micron and compare it with that moment three years ago when Nvidia hit its first $1 trillion valuation. The charts indeed are similar. But in my view, this is where the similarity ends. When Nvidia took off, it had an indisputable trump card — the software ecosystem CUDA. This technological moat tied developers tightly to the architecture of the company. It was impossible to pull out a chip from Nvidia from a server, to insert an analog from a competitor, and to continue work — the whole software environment would collapse. This second trump card provided the company with total dominance on the market and allowed analysts to build into models the prospects of domination over the next decade.

Micron Does Not Have Such a Trump Card

Memory — be that super-fast HBM3E or server DDR5 — is, by its essence, "hardware.” This is a standardized product (JEDEC). Memory chips have no software armor, protecting the manufacturer from the transition of a client to a competitor. If tomorrow another manufacturer offers memory with a similar bandwidth and energy efficiency at a better price, Alphabet (GOOG) (GOOGL) and Microsoft (MSFT) could replace Micron.

Illusion of a Technological Lead

Yes, today Micron is in a prime position. The company won the current round with its release of the needed HBM3E chips, and right now, the customer queue is booked for a couple of years in advance. But this effect, it is temporary. Nobody has canceled competition, and the main rivals of Micron — South Korean giants Samsung (SMSN.L.EB) and SK Hynix — do not intend to surrender their positions. It is important to understand the physics of this market: Technologically, all three players are approximately equal.

None of them has an exclusive, secret weapon in the production of chips. They all purchase lithographic EUV-scanners from the exact same Dutch company, ASML (ASML). They all work on similar nanometer tech processes and use fundamentally similar base technologies. The fact that Micron has torn ahead right now, this is a half-step advantage. In the scales of the technological race, half a step, this is half a year, maximum a year. This gives an excellent margin in the moment, but it is impossible to project this advantage a decade forward. Korean competitors will not sit idly by. And as soon as they reach their planned volumes, the deficit will begin to smooth out.

Trees Don't Grow to the Sky

Micron's current valuation of $1 trillion implies that the company will preserve an anomalously high margin and avoid harsh competition for long years. But without a software lock-in, this is mathematically impossible in the memory market. Sooner or later, competitors will catch up, market supply will grow, and clients will force manufacturers to lower prices, which will unavoidably hit the margin.

A backlog of orders for two years is excellent, but it's not 20 years. Micron remains a valuable company with strong management, but to buy it at its current, overheated to the limit multiples means to ignore the laws of competition. Growth to the sky, this is always dangerous. It is necessary to look with a cool head at how competitors will return to the game.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)