/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

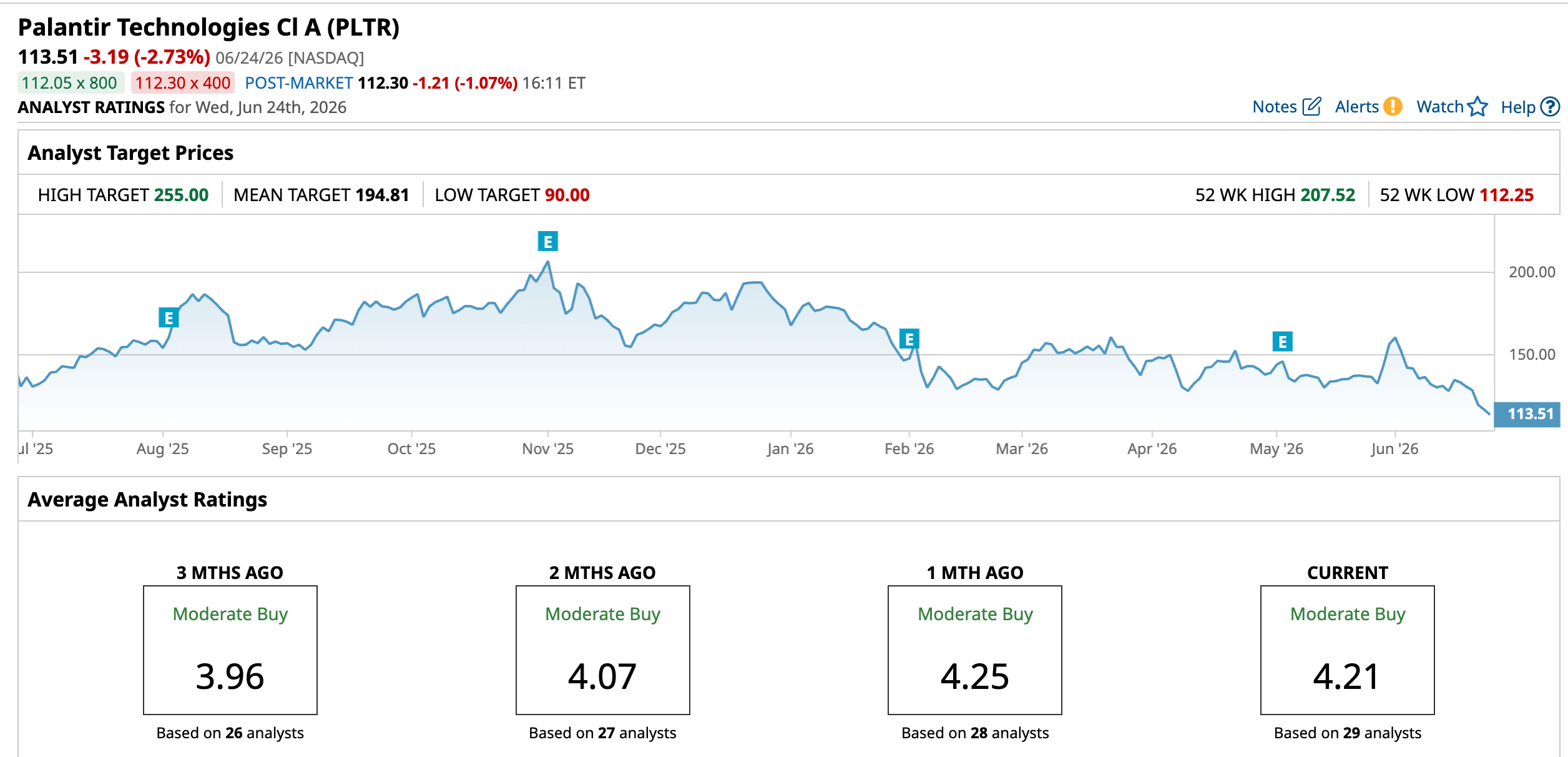

Palantir Technologies' (PLTR) stock has been under significant selling pressure for quite some time now. It recently crashed to a 52-week low, extending its year-to-date (YTD) decline to 36.03% and pushing it 45.3% below its previous 52-week high.

The sell-off has largely been driven by concerns surrounding valuation. For much of the past year, Palantir traded at a substantial premium to both traditional software companies and several large-cap technology peers.

In addition, investors began reassessing the competitive landscape for Palantir as new AI-focused companies, especially Anthropic, intensified competition in enterprise artificial intelligence (AI). As a result, the market became less willing to support Palantir's elevated valuation multiple despite continued operational execution.

While the stock price has weakened significantly, Palantir's underlying business fundamentals remain strong. Demand for the company's AI Platform (AIP) continues to accelerate as enterprises increase investments in AI-driven solutions. Customers are adopting Palantir's software to deploy and scale AI applications, strengthening the company's position within the rapidly expanding enterprise AI market.

Importantly, Palantir’s stock decline has helped address valuation concerns. While Palantir may still command a premium relative to many software peers, the recent pullback has improved Palantir’s risk-reward profile.

Palantir Maintains Its Explosive Growth Rate

Despite ongoing debates around valuation and competition, Palantir continues to deliver exceptionally strong growth. The company delivered another strong quarter, with Q1 revenue rising 85% year-over-year (YOY) to $1.63 billion. Q1 marked PLTR’s 11th consecutive quarter of accelerating revenue growth, highlighting the rapidly expanding adoption of Palantir’s AIP across its customer base.

Palantir is also growing its customer base at a solid pace. Its total customers increased 31% YOY to 1,007, while spending from existing clients continued to scale significantly. Revenue from Palantir’s top 20 customers averaged $108 million over the trailing 12 months, up 55% YOY. Notably, Palantir is acquiring customers fast and deepening relationships with its largest accounts.

The U.S. remains a high-growth market. Domestic revenue surged 104% YOY to $1.28 billion, driven by growing demand from both commercial enterprises and government agencies.

The commercial business was particularly impressive, with U.S. commercial revenue jumping 133% YOY as more organizations adopted AI-powered solutions. Meanwhile, U.S. government revenue grew 84%, supported by new contract wins and continued execution of existing programs.

Demand indicators remain exceptionally strong. Total contract value bookings increased 135% YOY, while net dollar retention reached 150%, showing that customers are expanding their spending significantly over time. Palantir finished the quarter with $11.8 billion in remaining deal value, up 98%, and $4.5 billion in remaining performance obligations, up 134%, providing strong visibility into future growth.

Palantir’s Upbeat Guidance Reflects Confidence in Sustained Momentum

Following the strong quarterly performance, management significantly increased its outlook for the remainder of 2026. Palantir now expects full-year revenue of approximately $7.66 billion, implying roughly 71% annual growth and representing a notable increase from its prior forecast of around $7.19 billion.

The company raised guidance for U.S. commercial revenue growth, adjusted operating income, and adjusted free cash flow. The upward revision indicates that the demand for its AI platform remains exceptionally strong.

Palantir Is a Compelling Buy

Palantir’s solid operational performance suggests that the underlying growth story remains intact. With revenue growth accelerating, customer spending expanding, and management raising guidance, Palantir continues to strengthen its position in the enterprise AI market. While competitive risks and valuation concerns have not disappeared, the recent decline has made its risk-reward profile attractive.

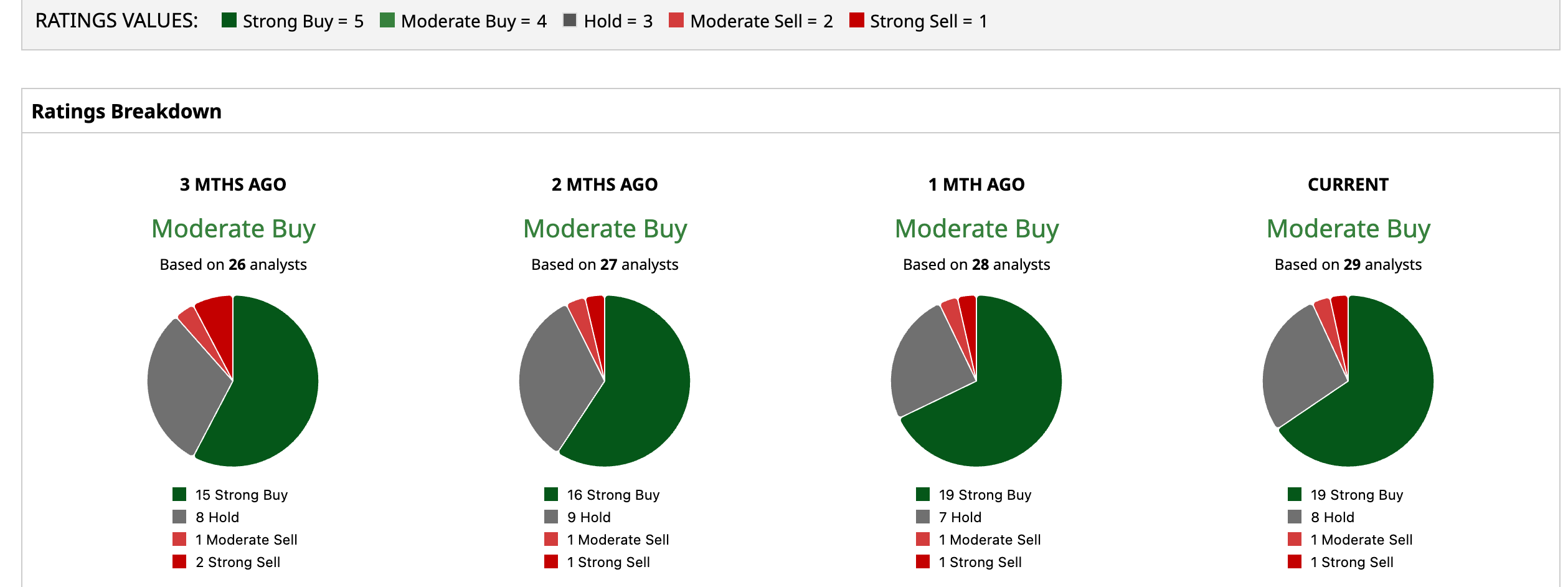

Among the 29 analysts covering PLTR, the consensus rates it a “Moderate Buy," with 19 giving a “Strong Buy,” eight giving a “Hold,” one providing a “Moderate Sell,” and the remaining one analyst placing a “Strong Sell."

While Palantir still trades at a relatively high price-to-sales ratio of 64.01 times, the company’s rapid revenue growth and expanding margins help support this premium valuation.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.