Happy Easter market watchers! He is Risen!

It is the beginning of a new month, and new quarter and calendars are getting busier by the day! Corn planting is underway and some soybean planting is starting further north.

Rains this week have been very welcome but were not as widespread as hoped. The areas that got rain received a lot while other areas were quite limited. There are a few more chances ahead and fingers crossed that we are blessed with more moisture, minus the severe weather. It already feels like it could be an active weather season ahead. In fact, it looks like the dry spell could be turning into a wet spell starting towards the end of this week. NOAA's 6-10 and 8-14 day outlooks are both showing above average rainfall for much of the Southern Plains.

It was a busy week in markets despite all US exchanges being closed for Good Friday. Usually, the energy and metals markets remain open on such holidays, but they were also closed on Friday while the banks were open. Go figure.

Daily headlines out of the White House and the Iranian regime whipsawed markets every which way this week. At one point this week, President Trump said that Iran was desperate to make a deal and then Iran did, in fact, acknowledge that they wanted the war to end if the right conditions were met. Then, President Trump made a national address, which I was expecting to continue with the theme of working towards a compromise to end the conflict and it turned out to be just the opposite.

The markets quickly interpreted Trump’s comparison of the current skirmish with the lengthy wars of the past, drawing attention that 32 days up to now was nothing as compared to the years of prior wars. The lack of any reference to an impending wind down spiked crude oil markets and plunged equity markets. However, markets managed to stabilize by the end of the day on Wednesday and finished the week on Thursday on much firmer footing that the preceding 24 hours.

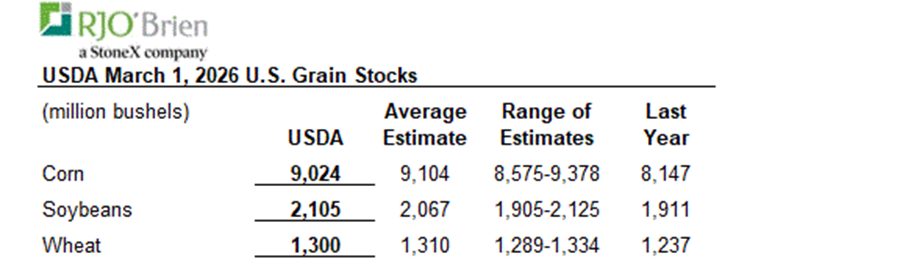

Grain markets followed the swings in crude oil as well as the fresh data provided by the USDA Prospective Plantings and Grain Stock reports released on Tuesday, March 31st at 11 AM CDT. USDA March 1st US corn stocks came in at 9.024 billion bushel versus expectations at 9.104 billion bushels average trade guesses and above last year’s 8.147 billion bushels. US soybean stocks came in at 2.105 billion bushels versus average trade guesses of 2.067 billion bushels versus last year’s 1.911 billion bushels. Wheat ending stocks came in at 1.30 billion bushels versus average trade guesses of 1.31 billion bushels versus last year’s 1.237 billion bushels.

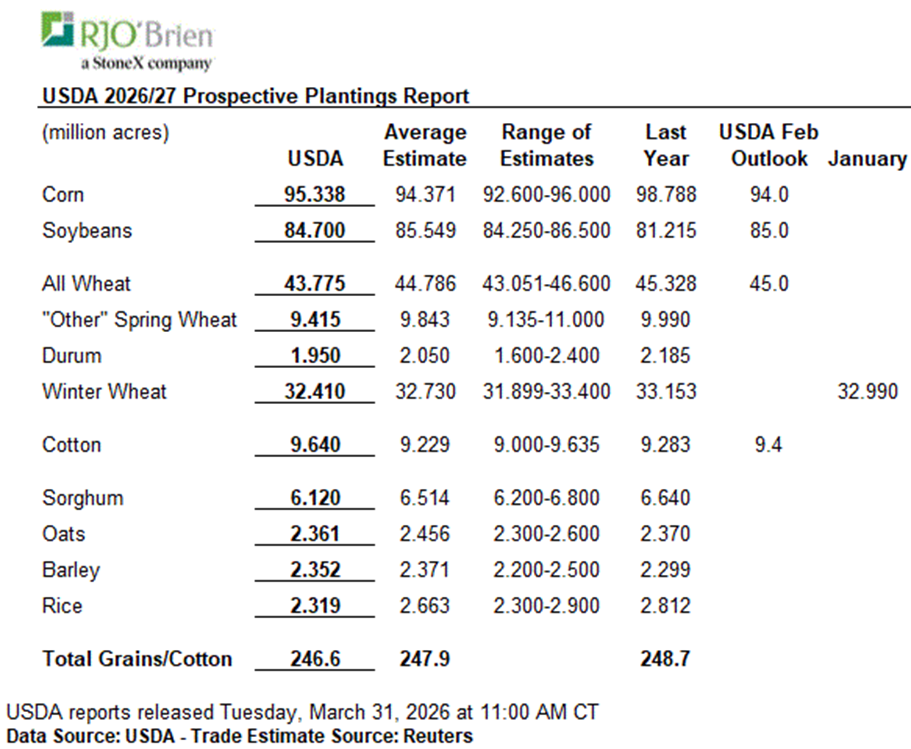

The acre numbers held more surprises with corn coming in at 95.338 million acres versus 94.371 million acres and last year’s 98.788 million acres. The USDA’s February Outlook guesstimate was 94.0 million acres. US soybean acres came in at 84.70 million acres versus expectations of 85.549 million acres and last year’s 81.215 million acres. The USDA’s February Outlook was 85.0 million acres. The all wheat class acreage number was 43.775 million acres versus average trade guesses 44.789 million acres. The winter wheat acreage number was 32.410 million acres versus average trade guesses of 32.730 million acres and last year’s 33.153 million acres and was one of the lowest on record. The USDA’s January Outlook number was 32.990 million acres.

Ultimately, the wheat acreage number, in particular, leans bullish. Rains in the Southern Plains this week brought some relief, but more is needed. The hotter than normal temperatures since the beginning of the year have matured wheat faster than usual and enhanced moisture demands. There is a lot of wheat in Texas, Oklahoma and parts of Kansas that is heading out and stunted due to the higher temperatures. We are in a critical period over the next 10 days for much of Western Kansas to get rain and still have potential for a sizable crop while Oklahoma and Texas are largely past this point. We will get national wheat condition ratings this next week that will bring more attention to the matter while only state-level reports so far have shown stress increasing.

The cattle market has absolutely been on fire in recent weeks. Fed cattle cash trade exploded this week with last week’s higher $238 level reaching $246 this week! As a result, feeder and live cattle futures traded near to filling the chart gap from October 13th last year.

With the strong US jobs report on Friday, I believe we will see equity markets rally early next week and the cattle markets continue to press higher to reach the chart gap and then we will see if we have enough momentum to make a new, all-time high or stall. If fed cattle cash trade is able to make additional highs, we could see futures march on.

We haven’t heard anything on the US-Mexican border in awhile and Secretary Rollins this week said that there is discussion about opening the crossing point in Arizona that is furthest from the New World Screw Worm cases. Follow this link to hear Secretary Rollin's commentary: Brooke Rollins: USDA Signals Potential Shift on Mexican Cattle Imports While Battling Screwworm Threat - Oklahoma Farm Report. While there is no timeline of the opening, it is an indication that the consideration is picking up again for something to happen with the reopening of the border. However, with the resurgence in fed cattle cash trade and boxed beef, I expect we will see slaughter numbers pick up as will the demand for cattle and in turn, prices.

Depending on the situation in the Middle East and how crude oil prices react, the headwinds or tailwinds will be important to gauge to keep the cattle markets running on fundamentals.

If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.