“Trump Accounts” – custodial investment accounts that allow newborn Americans and their parents a chance to start investing early – officially launched for deposits on July 4. One of the biggest draws is that children born in 2025 through 2028 are eligible for a $1,000 initial deposit from the U.S. government.

American families who jump to take advantage of these new accounts have a handful of ETF options to pick from:

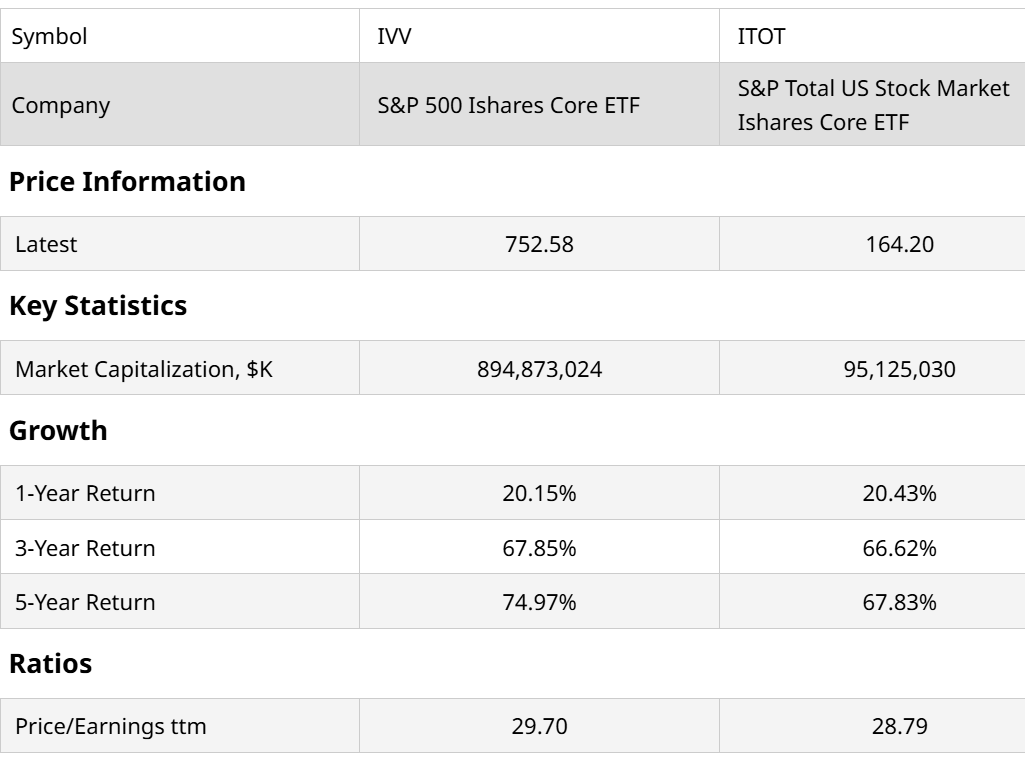

- iShares Core S&P 500 ETF (IVV)

- iShares Core S&P Total U.S. Stock Market ETF (ITOT)

- SPDR Portfolio S&P 500 ETF (SPYM)

- SPDR Total Stock Market Portfolio ETF (SPTM)

- Vanguard Total Stock Market ETF (VTI)

The existing set of ETFs are all focused on the US stock market.

To be clear, I am 10,000% in support of helping kids save for their education. But why not include access to U.S. Treasurys within Trump Accounts?

In a historic twist of fate, the Treasury market sorely needs the automated demand that the S&P 500 Index ($SPX) has received for years.

It is what they call the “passive bid.” People pop money into S&P 500 funds through their 401(k) plans, thinking of nothing other than their long time horizons.The funds themselves do not make active decisions. They buy “the market” as the index weightings direct them to.

As it is, there’s minimal difference between IVV and ITOT, the two iShares funds on the list, since the U.S. market is so dominated by large-cap stocks. So the top 500 stocks make the next 2,000 that ITOT adds to IVV quite irrelevant.

Stepping Back to the Basics

These newly launched Trump Accounts are a federal child-savings program created under the One Big Beautiful Bill Act. Millions of American kids get an automatic $1,000 government seed deposit, and parents can now chip in up to $5,000 a year in tax-deferred savings.

On paper, it sounds like a historic win for the next generation. My concern stems from a recent mandate issued by the Treasury Department.

At launch, the government announced that 100% of all initial contributions to Trump Accounts will automatically default into one of the above index funds. With an estimated 6 million accounts already open, and millions more coming, this setup means billions of dollars are about to programmatically slam directly into the S&P 500.

Because the index is market-cap weighted, that money won’t be spread out evenly. Instead, a massive chunk of this public cash is going to funnel straight into the top 10 mega-cap tech stocks that are already trading at historical, hyperextended valuations. The rich get richer, speaking in market cap terms.

For these multitrillion-dollar tech giants, the wave of automated buying is going to act as another dollop of cash inflows. In fact, these corporations are so incredibly huge already that their executive suites might not even notice how big the incoming pile of cash actually is.

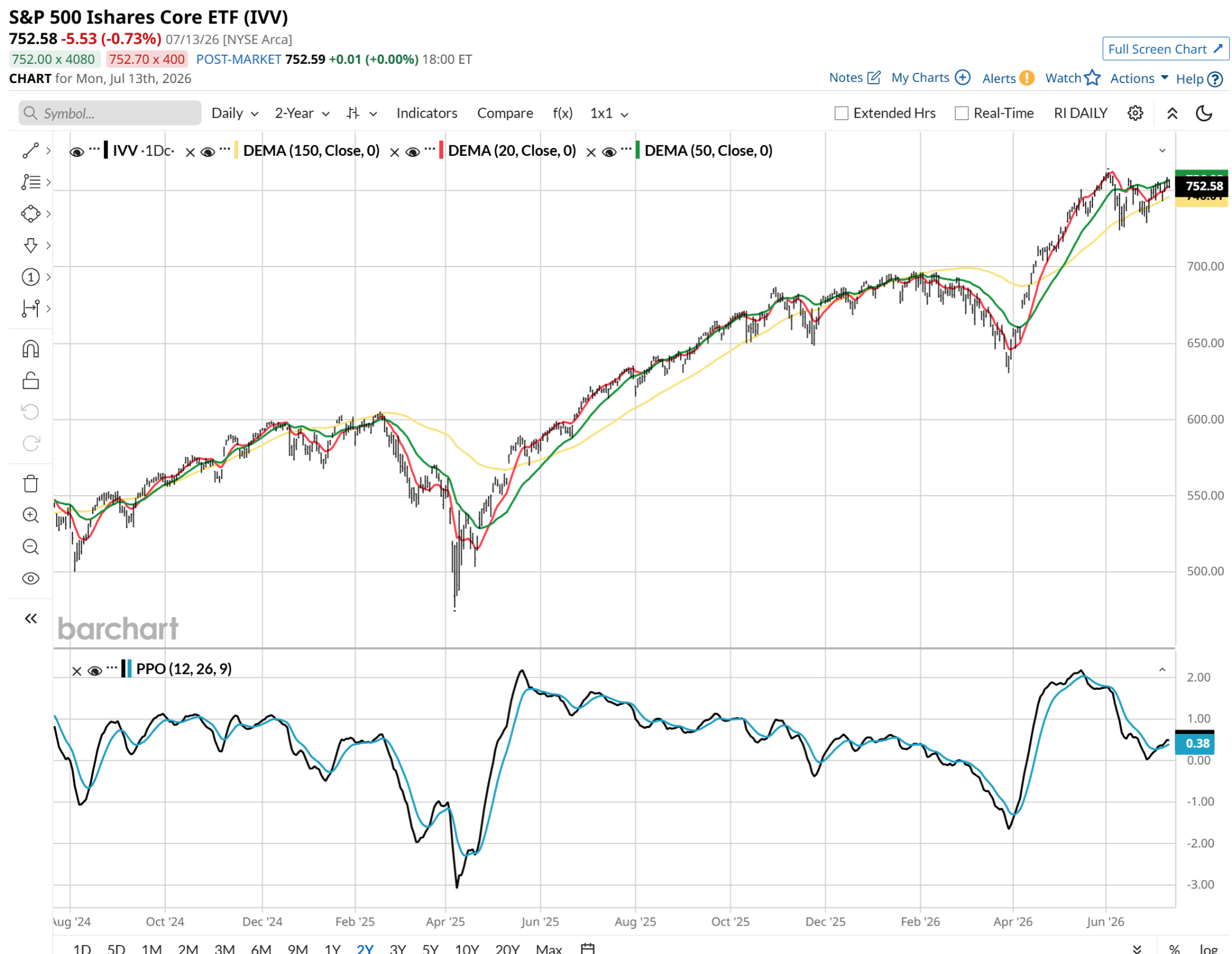

But forcing millions of children’s retirement nest eggs to buy into an expensive, tech-heavy index when broad market indicators are flashing signs of severe exhaustion is a dangerous late-cycle move. I cannot measure the impact precisely, but this could end up being a somewhat technical factor that keeps S&P 500 ETFs (like the one shown above) treading water, instead of falling under their own weight. The latter will occur, just later than if nature had taken its course.

Why U.S. Treasurys Might Be the Smarter Long-Term Choice

If the true goal of this legislation is to insulate and build generational wealth for young Americans over an 18-year growth period, we need to pay close attention to what these funds are investing in.

In his public remarks, President Donald Trump talked about how these initial investments could grow substantially by the time a kid reaches age 18. That is certainly one possibility. This is another:

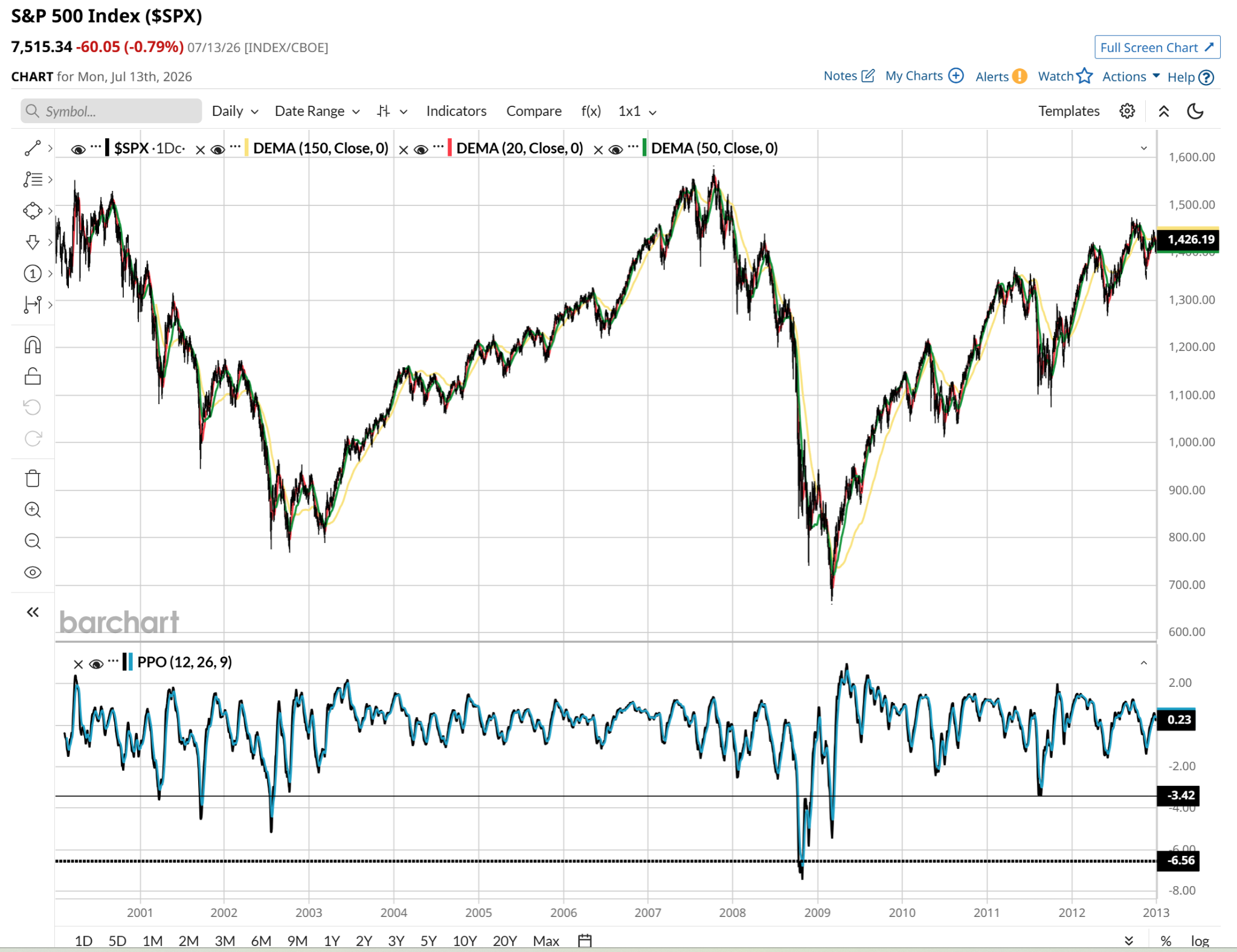

I point to that 13-year period above not to be a doomer, but to make the point that limiting these contributions to the stock market might one day be looked back on as part of the market top. Meanwhile, look at what’s going on in the bond market. I used 20-year bond rates here as a proxy.

It has been about 20 years since bonds of this maturity length have yielded 5%, as they do now. What’s a 5% compounded return for 18 years? That creates a 240% return during that span. The only risk is that the U.S. government can’t pay its debt.

And let’s face it, that’s an issue. I can’t help but think that the government has a much more urgent need for a “passive bid” in the Treasury market than in the stock market.

What’s the Irony Here?

If the Treasury had designed Trump Accounts to default into Treasurys instead of index funds, it would have accomplished two vital macro goals at once:

- It would protect millions of children from buying into a potential stock market bubble.

- It would provide the U.S. government with the exact same reliable, permanent passive bid on its sovereign bonds that Wall Street has safely enjoyed for decades.

As the program goes live, self-directed parents need to watch the investment menus closely. Trusting the default stock pipeline at a time when the broad market looks heavily overextended might mean your child’s financial headstart begins right at the wrong side of the market cycle.

Rob Isbitts is a semi-retired CIO, former fiduciary investment advisor, and Barchart columnist. Check out his other work at ETFYourself.com (featuring the Fresh Charts weekly trading post), and ROAR.PiTrade.com, helping investors to better-manage their own portfolios.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)