/PulteGroup%20Inc%20phone%20and%20website%20by-%20T_Schneider%20via%20Shutterstock.jpg)

Founded in 1950 and headquartered in Atlanta, Georgia, PulteGroup, Inc. (PHM) has spent more than seven decades helping Americans find a place to call home. What started with founder Bill Pulte building a single house has grown into one of the nation's largest homebuilders, delivering more than 875,000 homes across the U.S.

Today, with a market capitalization of $26.3 billion, the company operates in over 40 major markets, serving everyone from first-time buyers to luxury and active-adult homeowners through well-known brands including Pulte Homes, Centex, Del Webb, DiVosta, and John Wieland Homes. Backed by a disciplined land acquisition strategy and a diversified customer base, PulteGroup has built a reputation for steady execution in the housing market.

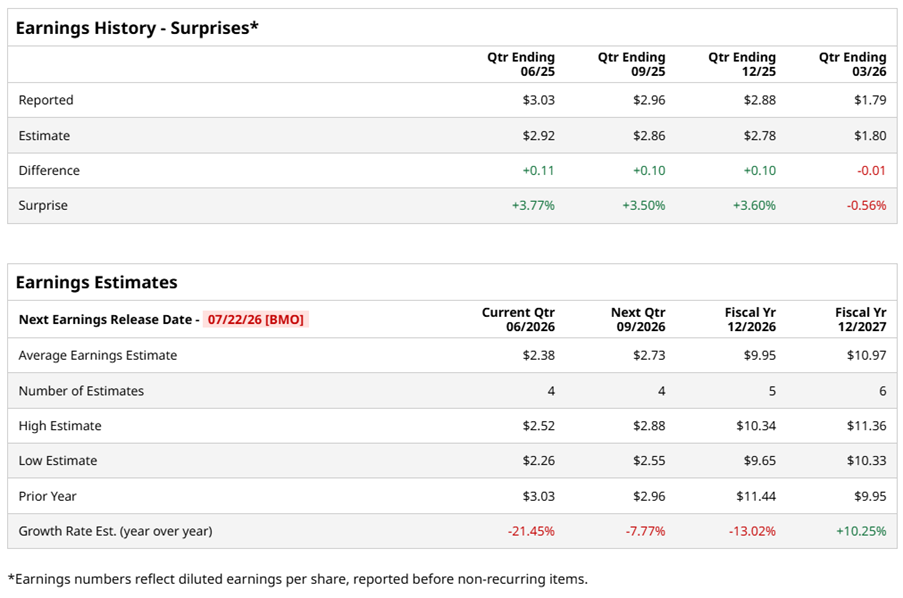

Investors will get a fresh look at its quarterly financial performance when the company reports its second-quarter earnings on Wednesday, July 22, before the market opens.

Wall Street is not expecting fireworks this quarter. Analysts forecast PulteGroup to earn $2.38 per share in the second quarter, which would represent a 21.5% year-over-year (YOY) decline.

Even so, the company has built a solid track record of delivering results, beating analysts’ earnings estimates in three of the past four quarters. Last quarter was the exception, with earnings slipping 30.4% YOY to $1.79 per share, narrowly missing expectations. Looking further ahead, analysts see fiscal 2026 EPS easing by 13% to $9.95 before rebounding by 10.3% annually to $10.97 in fiscal 2027.

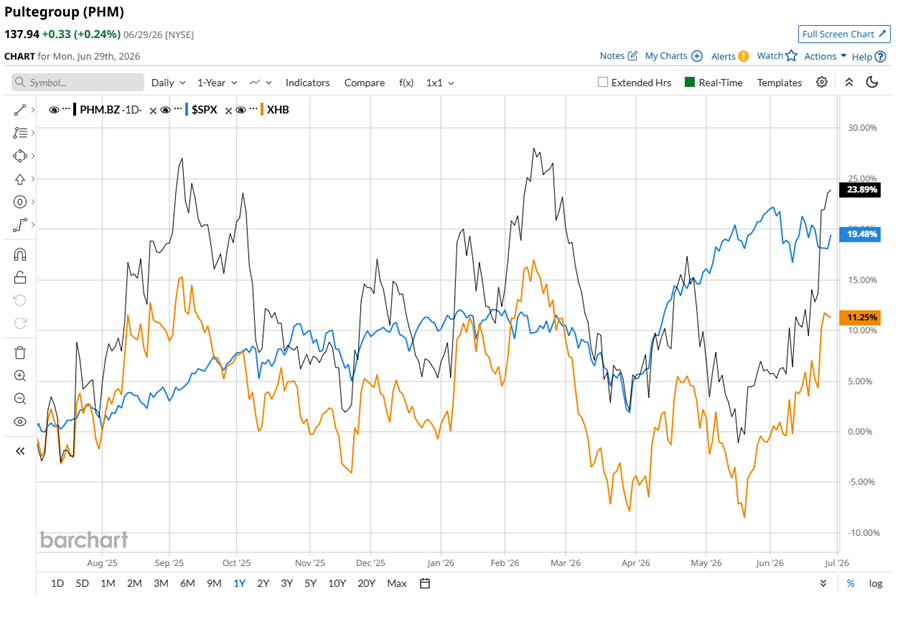

Despite the softer earnings outlook, investors have largely stayed in PHM’s corner. The stock has climbed 30.7% over the past year, comfortably outpacing the S&P 500 Index’s ($SPX) 19.9% gains and State Street SPDR S&P Homebuilders ETF’s (XHB) 16.4% return. The momentum has carried into 2026, with PHM up 17.9% on a year-to-date (YTD) basis, well ahead of the broader market’s 8.7% advance and XHB’s 11.4% gain.

PHM’s strong run in 2026 has not happened by chance. A friendlier macro backdrop has helped reignite investor optimism toward homebuilder stocks. The biggest catalyst came from the Federal Reserve, which kept its benchmark interest rate unchanged at 3.5% to 3.75%, easing concerns that borrowing costs would climb even higher.

At the same time, mortgage rates edged lower, with Freddie Mac reporting the average 30-year fixed rate slipping. While those moves may seem modest, they improved affordability at the margin and fueled hopes that homebuying activity could gradually pick up, giving investors another reason to warm up to builders like PulteGroup.

The consensus opinion on PHM stock is a “Moderate Buy” rating. Of the 16 analysts covering the stock, seven have a “Strong Buy,” one advises a “Moderate Buy,” seven play it safe with a “Hold,” and one is outright skeptical, with a “Strong Sell” rating.

PHM is trading slightly below its average price target of $138.36, but the Street-high target of $162 indicates a potential upside of 17.7% from current price levels.

On the date of publication, Sristi Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)