/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

Chip giant Intel Corporation (INTW) is all set to report its second-quarter results for fiscal 2026 on July 23, after the market closes. Ahead of the results, the market is bullish on the company amid heightened demand for its AI servers and CPUs.

The company has also been propped up by its partnerships with large hyperscalers. The company is building upon its partnership with Alphabet's (GOOG) (GOOGL) Google. Recently, the company announced it will use Google’s Gemini to automate silicon development. This is supposed to harness Intel’s “AI-powered transformation,” as it’s expected to help the company move beyond isolated pilot projects and deploy some capabilities across its entire organization.

Intel’s backing from the United States government (holding a 10% stake in the firm) has reportedly helped it land a deal with Apple (AAPL). According to a report, Apple might be planning to have Intel fabricate chips for both Macs and iPhones.

We take a closer look at Intel ahead of its earnings release…

About Intel Stock

Intel is a major semiconductor producer undergoing a broad operational reset centered on manufacturing, AI, and foundry scale-up. The company is actively expanding its fabrication footprint in the U.S. and Europe, advancing new process technologies, and tightening ownership and control of critical fabs to secure leading-edge capacity.

At the product level, Intel is ramping next-wave Xeon server CPUs, AI-enabled Core Ultra PCs, and end-to-end AI infrastructure from chips to rack-scale systems, often delivered through ecosystem partnerships. Intel’s global headquarters is located in Santa Clara, California. The company has a market capitalization of $487.42 billion.

Investors have been buying into Intel’s turnaround led by AI and foundry execution, as the company’s data center and AI businesses are growing rapidly. Intel’s high‑profile AI partnerships, plus government and strategic capital, have boosted confidence that it can fund and deliver its multi-year manufacturing roadmap.

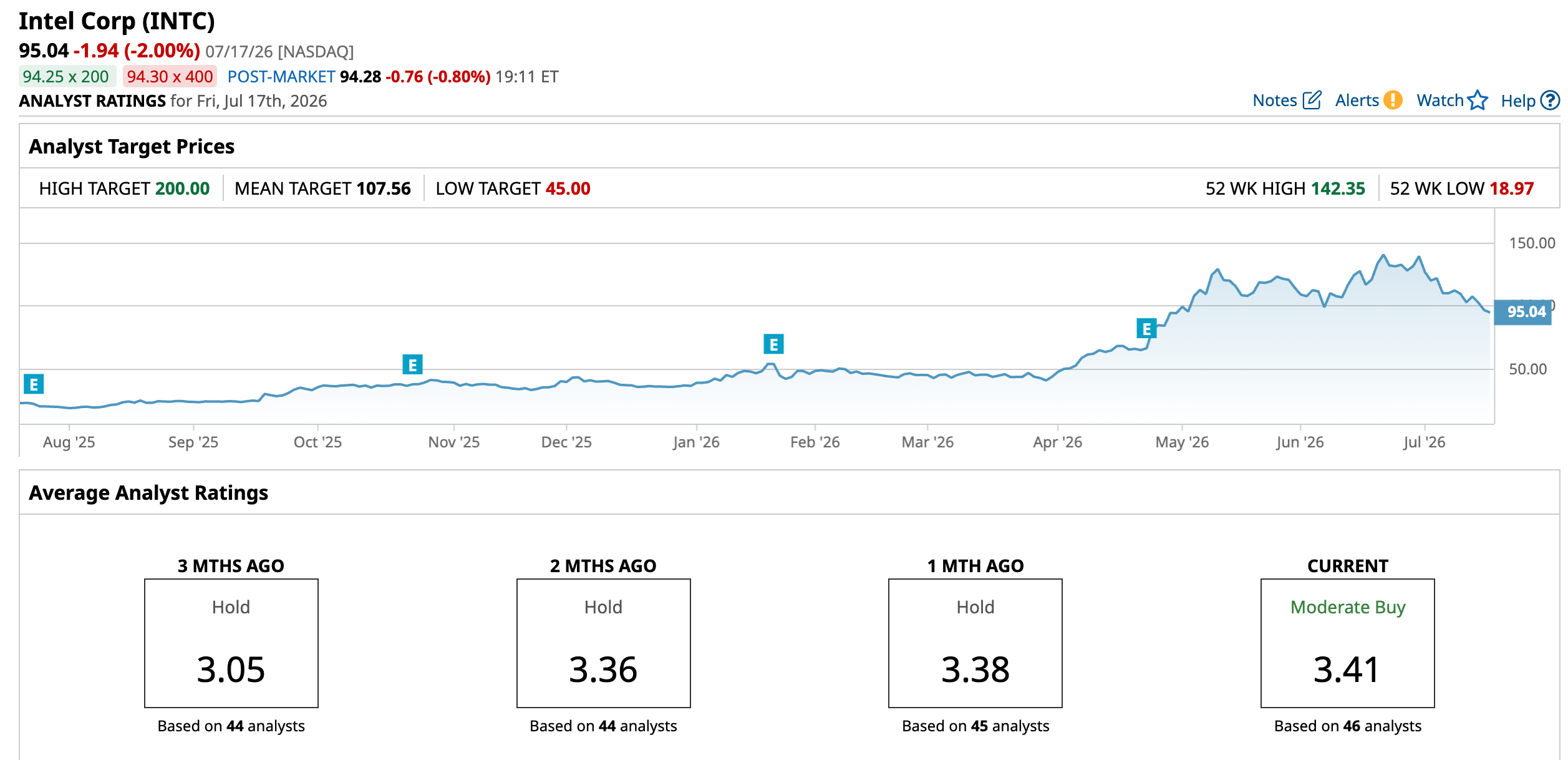

Over the past 52 weeks, Intel’s stock has gained 315.8%, while it is up 157.6% year-to-date (YTD). The company’s shares reached a 52-week high of $142.35 on June 30, but are down 33% from that level.

On a forward-adjusted basis, Intel’s stock has a price-to-earnings (non-GAAP) ratio of 87.34 times, which is higher than the industry average of 24.29 times.

Intel’s Q1 Results Showed Resilience

Reflecting the growing role of CPUs in the AI era, Intel reported solid results in its first quarter. The company’s revenue increased by 7% year-over-year (YOY) to $13.60 billion. Its non-GAAP operating margin grew by 6.9 percentage points over the same period to 12.3%. Its non-GAAP EPS grew 123% from the prior-year period to $0.29.

Street analysts are robustly optimistic about Intel’s bottom-line trajectory. For the current fiscal year, EPS is projected to surge 641.7% annually to $0.65, followed by a 53.9% increase to $1.00 in the next fiscal year. The company is expected to report its second-quarter 2026 results on July 23, after the market closes. Ahead of that, analysts expect its EPS to grow by 138.5% to $0.10.

What Do Analysts Think About Intel’s Stock?

Recently, Susquehanna analyst Christopher Rolland maintained a “Neutral” rating on the stock but raised the price target from $80 to $115 ahead of Intel’s second-quarter earnings. Rolland highlighted stronger-than-expected server CPU demand and modestly better PC ODM builds in the near term. The analyst also believes the server-chip supply-demand imbalance will persist through 2028.

KeyBanc analysts maintained an “Overweight” rating on Intel and raised the price target from $110 to $155. Analysts at the firm cited strong demand for server CPUs led by agentic AI trends. Intel has increased capacity at its INTC 3 fab to accommodate 25%-30% growth in server units this year and exceed 50% growth next year. At the same time, yields on its 18A node have risen sharply, climbing from about 65% in the previous quarter to above 85% now.

Expecting a “beat-and-raise” quarter from Intel, analysts at UBS raised the price target from $83 to $121, while maintaining a “Neutral” rating on the stock. UBS analysts believe that server CPU demand remains very strong, allowing Intel to push through higher prices.

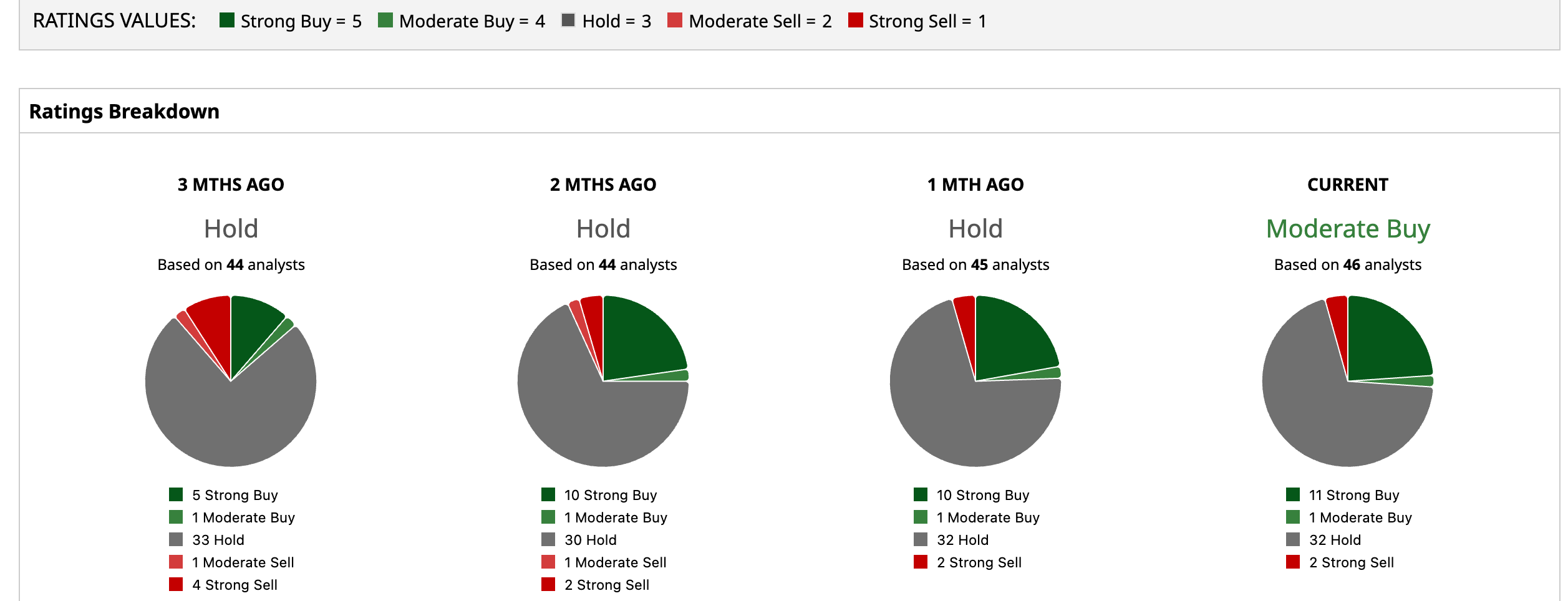

Intel has long been a stalwart on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 46 analysts rating the stock, 11 have given it a “Strong Buy” rating, one a “Moderate Buy,” 32 a “Hold,” and two a “Strong Sell.” The consensus price target of $107.56 represents a 13.2% upside from current levels. Moreover, the Street-high price target of $200 implies a 110.4% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)