The Energies sector was quietly lower overnight through early Thursday morning, mostly, though it will not be surprising to see markets find renewed buying interest.

US stock index futures were mixed, following the lead of foreign markets, giving us a reason for another round of the Chicken and the Egg Debate.

The Grains sector was under pressure again, the spotlight on HRW wheat and a possible 11th consecutive lower daily close Thursday.

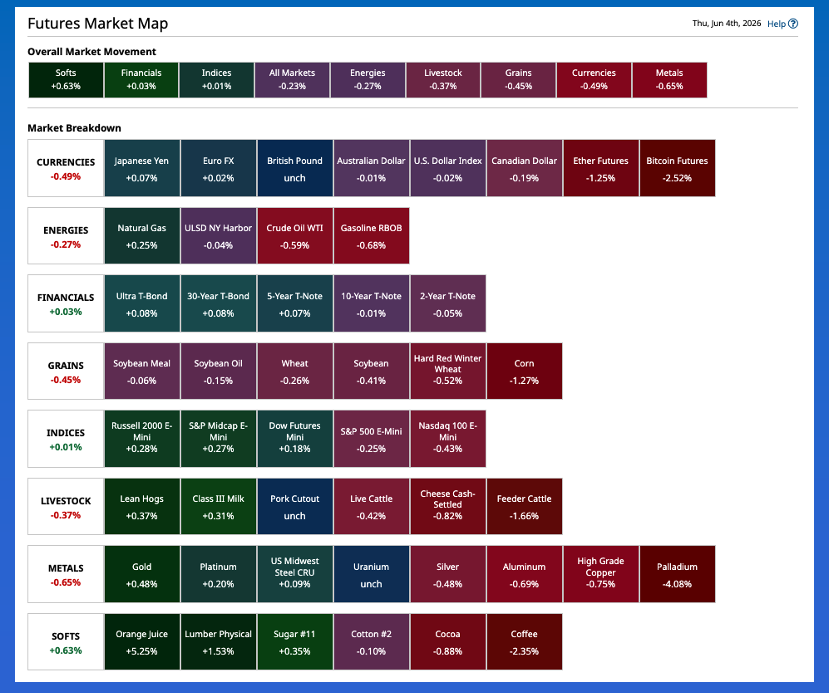

Morning Summary: A look at the Barchart Futures Market Heat Map early Thursday morning shows us what happens these days when headlines don’t happen. The commodity complex is about as exciting as watching The America’s Cup sailboat race[i] when there is no wind. The boats just sit, dead in the water. The race would be made better if the Discovery Channel’s Shark Week was introduced into the event. As for markets, most sectors were within fractions of unchanged pre-dawn. The high end of the scale finds Softs with a gain of 0.63% and the low end led by Metals with a loss of 0.65%. It should be noted Softs were heavily influenced by two markets that don’t trade overnight: Orange juice with its leftover 5.25% rally and lumber’s 1.5% gain from Wednesday. Energies were mostly lower, albeit quietly, at this writing, with the situation in the Middle East unchanged. The Financials (US Treasury futures) sector has been busy this week, unusual for a typically staid set of markets. Indices (US stock index futures) were quietly mixed, reflecting the lower close to Asian markets and higher early trade in Europe[ii]. It will be interesting to see what happens in Livestock Thursday following yesterday’s noncommercial led selloff in both cattle markets.

Corn: Speaking of Watson, the corn market crumbled overnight through early Thursday morning on what looked to be continued fund long liquidation. As of this writing, all issues from July 2026 through May 2027 were down 5.5 cents with the first three (July, September Dec26) showing an uptick in overnight trade volume. A look back at Wednesday’s session and we see July (ZCN26) closed 9.0 cents lower followed by the National Corn Index coming in near $3.9650, down about 8.5 cents for the day. This put national average basis at 35.0 cents under July futures as compared to the previous 10-year low weekly close for this week of 39.75 cents under. The previous 5-year low weekly close is 23.0 cents under July. We’ll get the latest round of weekly export sales and shipments numbers later Thursday morning, with the previous set putting US corn’s export pace projection at 3.32 bb, up 22% from the 2024-2025 marketing year reported shipments of 2.72 bb. However, this pace projection extended the downtrend it has been in since early November. Over in new-crop, December (ZCZ26) posted a low of $4.5350 as of this writing, its lowest mark since February 2. Wednesday saw the Dec-March futures spread close covering a straight-up neutral 50% calculated full commercial carry.

Soybeans: After settling mixed Wednesday, the oilseed sub-sector was quietly lower early Thursday morning. July soybean oil (ZLN26) slipped as much as 0.53 cent on trade volume of fewer than 10,000 contracts but was down only 0.18 at this writing. A quick look at the Energies sector shows us the spot-month distillates (diesel fuel) contract (HON26) was down 2.4 cents (0.6%) after sliding as much as 4.6 cents overnight. It will not be surprising if diesel fuel finds enough buying to close higher later today. As for soybeans, the July issue (ZSN26) dropped as much as 7.0 cents through Thursday’s early morning hours on trade volume of about 13,000 contracts and was only 1.0 cent off its session low. This after July stumbled to a 11.25-lower close yesterday. Last night saw the National Soybean Index come in near $10.9425, down about 10.75 cents from Tuesday and putting national average basis at 59.75 cents under July futures as compared to the previous 10-year average weekly close for this week of 57.0 cents under July. New-crop November (ZSX26) was sitting 4.75 cents in the red pre-dawn after losing as much as 5.5 cents overnight. From a technical point of view, Nov26 has taken out its previous 4-week low of $11.67 this week.

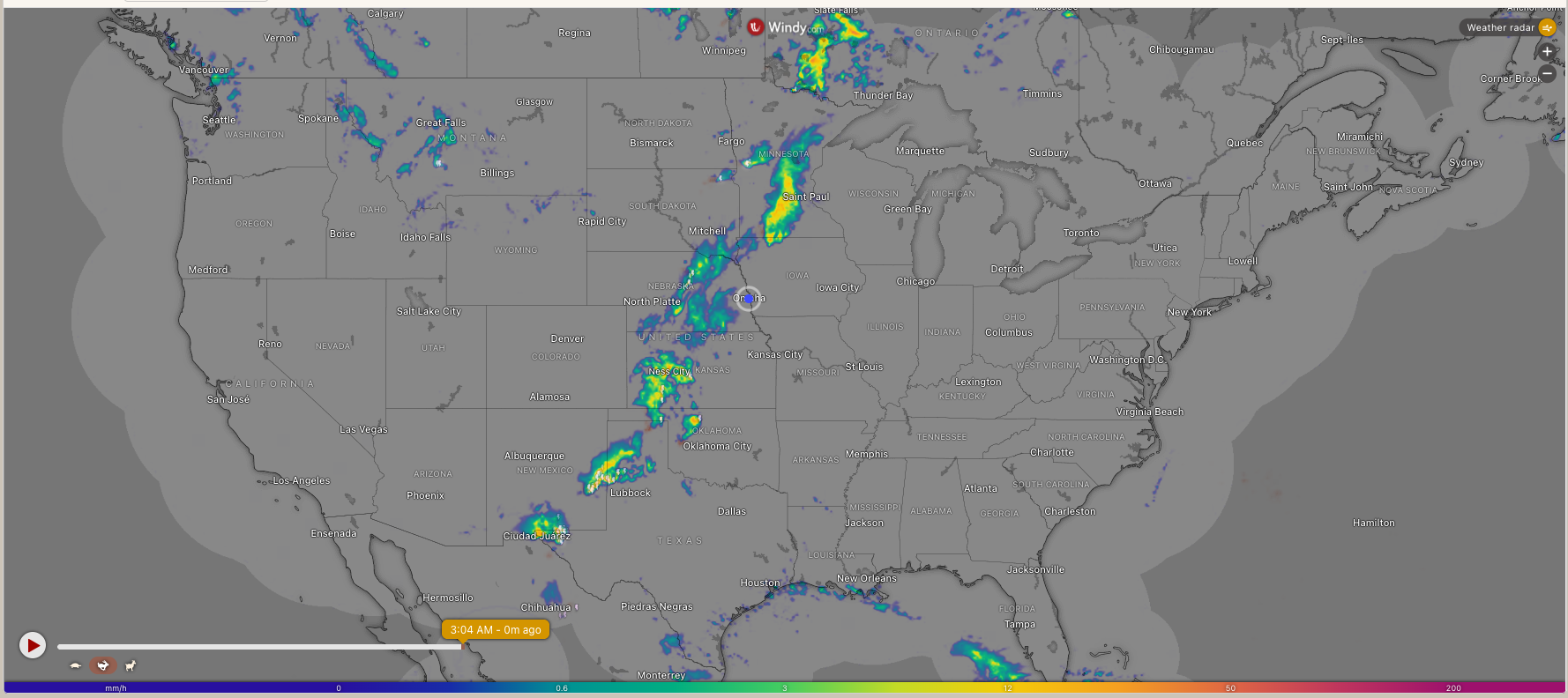

Wheat: A look at the radar map early Thursday morning shows more rains have moved into the US Southern Plains, stretching across the western parts of Texas, Oklahoma, and Kansas. As I’ve mentioned recently, this is too much too late for the 2026 HRW crop in the area, with insurance companies having zeroed out production in some cases. We’ll get the latest US Drought Monitor map later Thursday morning, but for HRW winter wheat it is a moot point as harvest struggles to move north out of Texas. Still, the overnight session saw the July HRW issue (KEN26) lose as much as 8.5 cents, pushing its 11-day loss to 88.25 cents. I’ll let that sink in for a moment. While much of the pressure has come from Watson, as indicated by the latest Commitments of Traders report showing funds switched to a net-short futures position of 1,730 contracts, the commercial side has been content to sit back and watch the carnage. The latest national average basis calculation came in at 60.25 cents under July as compared to the previous 5-year low weekly close for this week of 60.25 cents under July. Meanwhile, the July-September futures spread covered a neutral 52% calculated full commercial carry at Wednesday’s close.

[i] This takes me back to my early days as a commodity broker in Wichita, Kansas. I was part owner in a small business – Pinnacle Futures – with one of the other partners from New Zealand. He took the America’s Cup race seriously, along with rugby and cricket.

[ii] This brings to mind the Chicken and the Egg Debate: Do Asian and European markets follow or lead US markets? Almost as fun of a discussion as Great Taste versus Less Filling (IFKYK).

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Amazon_com%20Inc_%20%20package%20by%20-%20AdrianHancu%20via%20iStock.jpg)

/Salesforce%20Inc%20HQ%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

/Dell%20Technologies%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Intel%20Corp_%20Santa%20Clara%20campus-by%20jejim%20via%20Shutterstock.jpg)