What a week it has been in wheat. It isn’t often the market known as Poverty Grass – for both those who produce it and those who try to trade it – takes the spotlight in the Grains sector, but that’s what we saw this past week. After I wrote my thoughts on the new generation of “trader” being introduced to wheat, and natural gas, via predictive market websites like Kalshi a couple weeks ago, and followed that piece with a discussion on wheat as a good long-term investment last week, I’ve had the opportunity to talk wheat with Michele Steele in a StocktwitsTV interview and Michelle Rook on Thursday’s Markets Now. For someone who grew up on a small wheat farm in south-central Kansas, and spent the early part of his career trading to merchandise the Cockroach of Grains (another nickname for wheat), it’s always fun to return to my roots. It reminded me of when I used to appear on the Iowa Public Television program Market to Market, and the hosts – first Mark Pearson, then my friends Mike Pearson and Delaney Howell – would start our conversations by saying something to the effect of, “Darin, since you are a wheat guy, let’s start there…”.

As we head into Friday’s session, what has changed with the wheat sub-sector, particularly the hard red winter and soft red winter markets?

- Beginning with the July HRW issue (KEN26), because HRW is the largest wheat crop grown in the US:

- The contract is up 30.0 cents from the close on Friday, April 17 through Thursday, April 23

- Due to the contract closing 29.25 cents higher Thursday

- Meanwhile, total open interest increased by 3,737 contracts during that same time frame

- Also, the July issue was up 19.5 cents for the Tuesday-to-Tuesday positioning week

- While the carry in the July-September futures spread saw its carry weaken from 12.75 cents on Tuesday, April 14 (55% calculated full commercial carry) to 12.0 cents on Tuesday, April 21 (52%).

- The same spread closed Thursday, April 23 at a carry of 11.5 cents (49.5% cfcc)

- Telling us support came from both commercial and noncommercial traders

- The commercial side still held a neutral view of supply and demand, as would be expected from those who understand wheat isn’t dead until combines prove it to be the case

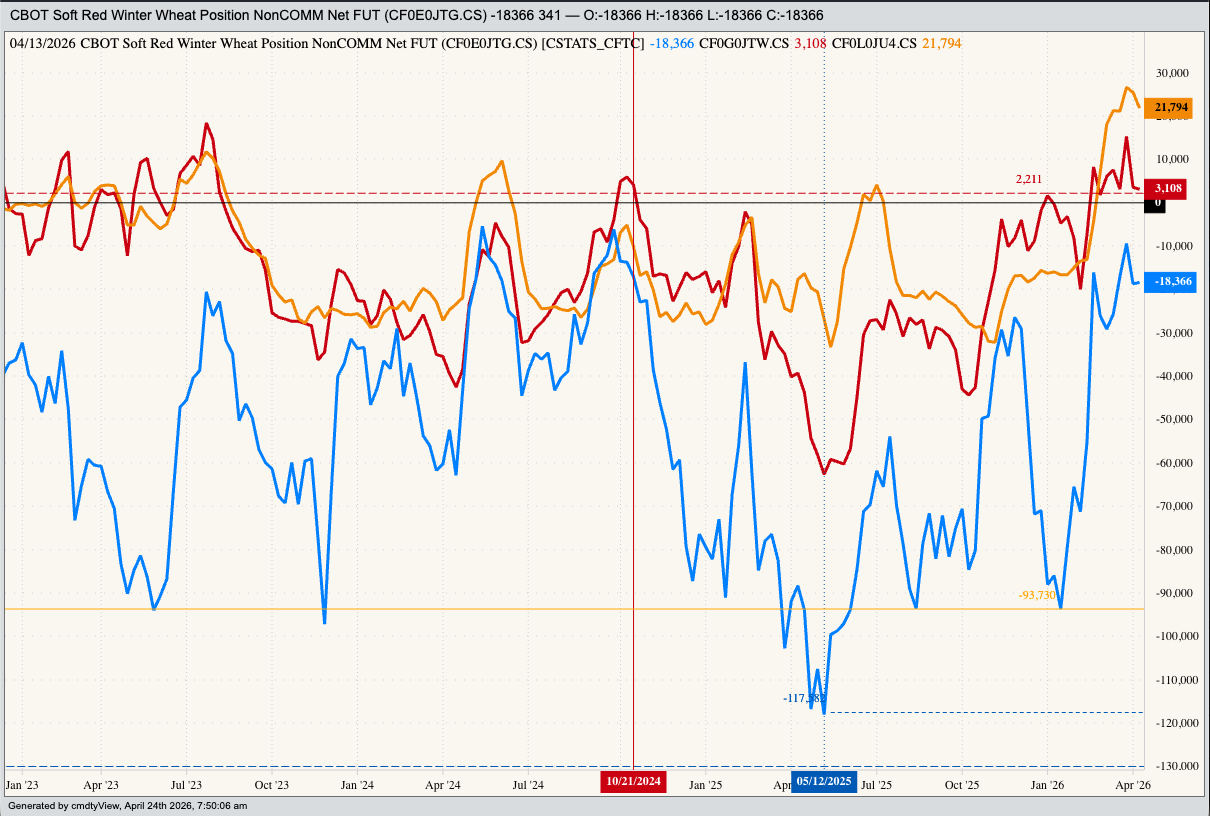

- The noncommercial side held a net-long futures position of 3,108 contracts as of Tuesday, April 14

- The contract is up 30.0 cents from the close on Friday, April 17 through Thursday, April 23

This brings us to the Question of the Day: Is HRW wheat rallying due to weather concerns, increased interest from newbie “traders”, or both?

As mentioned, those who understand a wheat crop isn’t officially dead until combines find it to be the case, the commercial side of the market, continue to take a wait and see approach. HRW futures spreads are not bearish, but neither are they bullish. Beyond the near straight up neutral 50% July-September spread, the September-December was covering a neutral-to-bullish 40% at Thursday’s close with the December-March covering a bullish 28.5%. While this tells us there is a concern over supplies in relation to demand later in the 2026-2027 marketing year, we have to keep in mind trade volume and open interest is light in those deferred futures contracts. For the record, though, this week last year saw the Dec25-Mar26 futures spread cover 55% calculated full commercial carry telling us the commercial side is more concerned than it was a year ago.

Those who don’t understand wheat, the noncommercial side looking to bring back the Wild West days of meme stocks, this time in commodities, have likely been adding to their net-long futures position. As mentioned, the previous Commitments of Traders report showed funds held a net-long futures position of 3,108 contracts, down from the recent high of 15,315 contracts the week of Tuesday, March 31. A look back to a year ago at this time and we see Watson (my name for the algorithm-driven noncommercial side) was on its way to a net-short futures position of 62,690 contracts the week of May 12, 2025. At the same time, total open interest in the HRW market was 262,000 contracts as compared to this past Thursday’s reported figure of 298,200 contracts. Doing the math:

- The noncommercial net-futures position has seen a switch of 65,800 contracts this past year

- While total open interest has increased by 36,200 contracts

What’s my conclusion, then? Is this traditionally viewed weather derivative market being driven by concerns adverse weather (drought, freeze, etc.) has reduced production potential or by the latest round of Wild West meme stock “traders” looking for a quick buck? For now, I continue to lean toward the latter but acknowledging there is at least some concern over crop potential being registered by the commercial side. That being said, and as I discussed with Michelle Rook this week, the world isn’t going to be running out of wheat anytime soon. We can see that in the SRW July 2026-May2027 forward curve leaning bearish, covering 67% cfcc. Though this comes with the asterisk of the CME’s Variable Storage Rate. So we’ll see.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)