/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom is creating a massive race for computing power, and that is turning semiconductor foundries into some of the most important businesses in the world. Some companies may design the chips powering AI. But foundries are the companies that actually manufacture them at scale. And right now, no company dominates that space more than Taiwan Semiconductor ADR (TSM).

TSM builds the world’s most advanced chips for the biggest tech companies, which is why investors have closely watched rising fears around the foundry industry lately. Some worry competitors could slowly catch up as governments pour billions into domestic chip manufacturing. Others fear aggressive industry expansion could eventually create oversupply.

But TSM’s management sounds far more confident than worried, still betting heavily on the AI boom. They forecast the global semiconductor market to top $1.5 trillion by 2030, driven largely by AI and high-performance computing demand. To keep pace with demand, TSM is rapidly expanding its advanced chip and packaging capacity, while expecting AI accelerator wafer demand to surge dramatically over the next few years.

That confidence is also why Bank of America believes recent fears around TSM’s foundry dominance are overdone. The bank argues TSM’s technology lead, manufacturing scale, and superior yields still keep rivals well behind.

With TSM stock continuing to show strong momentum across both the long and short term, many on Wall Street still view the company as one of the clearest and most reliable AI winners to own for the years ahead.

About Taiwan Semiconductor Stock

Founded in 1987, Taiwan Semiconductor redefined the industry by pioneering the pure-play foundry model and has dominated ever since. Now valued at $2.1 trillion by market cap, it stands as the world’s leading chipmaker, producing around 12,682 products in 2025 for 534 global clients.

From smartphones to data centers, TSM’s cutting-edge 3nm and 5nm chips fuel the AI revolution, powering Nvidia (NVDA), Apple (AAPL), Advanced Micro Devices (AMD), and countless others. With operations stretching from Asia to North America, TSM is shaping the future of computing.

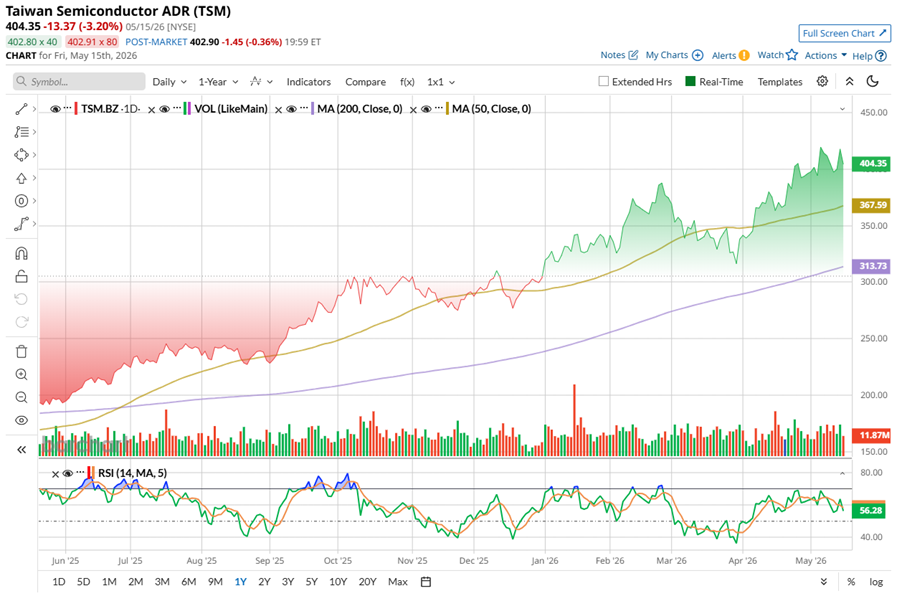

TSM stock has been on a powerful run, and the chart still tells a bullish story. Shares remain well above the 200-day moving average, a classic sign that the long-term uptrend is still intact. Over the past 52 weeks, TSM stock has skyrocketed 103.6%, massively outperforming the S&P 500 Index ($SPX), which gained 23.93% during the same stretch. The rally also pushed the stock to a fresh high of $421.97 on May 14.

A big reason behind the move is TSM’s growing confidence in the future of semiconductors. Management now believes the global chip market could top $1.5 trillion by 2030, with AI and HPC expected to drive more than half of that demand.

The stock is trading above its 50-day moving average, showing that shorter-term momentum remains healthy. Shares are up 30.13% year-to-date (YTD) and 6.74% over the past month as investors continue piling into AI leaders. Friday’s red volume bar likely points to some short-term profit-taking after the recent rally rather than a major shift in trend. Technically, the 14-day RSI sits at 51.97, suggesting the stock still has room to run without looking overheated yet.

TSM is not cheap, priced at 27.40 times forward adjusted earnings and 11.37 times forward sales, both above its historical averages and sector medians. But investors are paying up for a reason. With AI demand climbing and TSM dominating advanced chip production, the premium valuation still looks justified for long-term bulls.

Meanwhile, the company is rewarding long-term investors. On May 12, TSM declared another quarterly dividend, taking the annualized payout to $3.51, offering a 0.87% yield. With a lean 6.25% payout ratio, there is plenty of room for future hikes. TSM blends innovation and shareholder returns, positioning itself as both a growth and income powerhouse.

Taiwan Semiconductor’s Stellar Q1 Earnings Report

The world’s largest foundry delivered a blockbuster Q1 report in April. Revenue jumped 35% year-over-year (YOY) to $35.9 billion, beating Wall Street estimates, while EPS surged 58.3% annually to $3.49. The real engine was AI demand.

High-performance computing made up 61% of revenue, far ahead of smartphones at 26%. IoT, automotive, consumer electronics and other segments contributed the rest. The company’s most advanced chips kept dominating too, while the 3-nanometer technology accounted for 25% of wafer revenue, 5nm for 36%, and 7nm for 13%. Altogether, advanced nodes below 7nm made up 74% of total wafer revenue.

Management said AI-related demand remains “extremely robust,” with hyperscalers and chip designers racing for leading-edge silicon. That is why TSM still sits at the center of the AI buildout.

Cash flow stayed massive as well. As of March 31, the company generated $105.5 billion in cash, cash equivalent balances and investments in marketable financial instruments, while free cash flow amounted to NT$348.2 billion ($11 billion). Capital expenditures totaled $11.1 billion in Q1.

CEO C. C. Wei emphasized that customers rely on TSM for a steady pipeline of cutting-edge chip technology, and demand is not slowing. For Q2, TSM expects revenue between $39 billion and $40.2 billion. For full-year 2026, management still sees revenue growing by more than 30% in U.S. dollar terms.

That momentum continued into April. The company reported monthly revenue of NT$410.73 billion ($13.1 billion), down 1.1% from March but still up 17.5% YOY. For the first four months of 2026, revenue climbed 29.9% annually to NT$1.54 trillion ($48.9 billion). While the month-over-month dip suggests growth is starting to normalize, TSM still appears firmly on track to hit its Q2 guidance. That slowdown is not necessarily a red flag either. The company is already running its advanced nodes at near-full capacity while pouring billions into capex to keep up with the AI-driven demand cycle.

Wall Street is bullish, eyeing $39.9 billion in revenue and 48.2% annual EPS growth to $3.66 in Q2. Looking ahead, analysts expect profits to rise 43.2% annually to $15.25 per share this year and climb another 24.4% YOY to $18.97 per share in fiscal 2027, supported by AI demand, advanced-node ramps, and packaging expansion.

Wall Street’s Bullish Bet on Taiwan Semi Stock

Bank of America is still firmly bullish on TSM stock. After TSM's technology symposium in Taiwan, the bank reiterated its “Buy” rating and kept its NT$2,560 price target, arguing that fears about rising foundry competition are largely overblown.

Analyst Haas Liu said TSM’s scale and technology lead in advanced chips are actually widening the gap against rivals. On the key 3nm and 5nm nodes, TSM is targeting 25% annual capacity growth between 2022 and 2027, with 3nm production expected to ramp sharply over the next two years.

The bank also highlighted strong momentum at TSM’s next-gen N2 process, where capacity is expected to grow 70% annually from 2026 to 2028. TSM is building five fabs at once and has reportedly reached key defect targets ahead of schedule. Advanced packaging remains another big edge. TSM plans to aggressively expand CoWoS and SoIC capacity through 2027, while BofA said the company’s packaging yields are already significantly ahead of Intel’s competing technology.

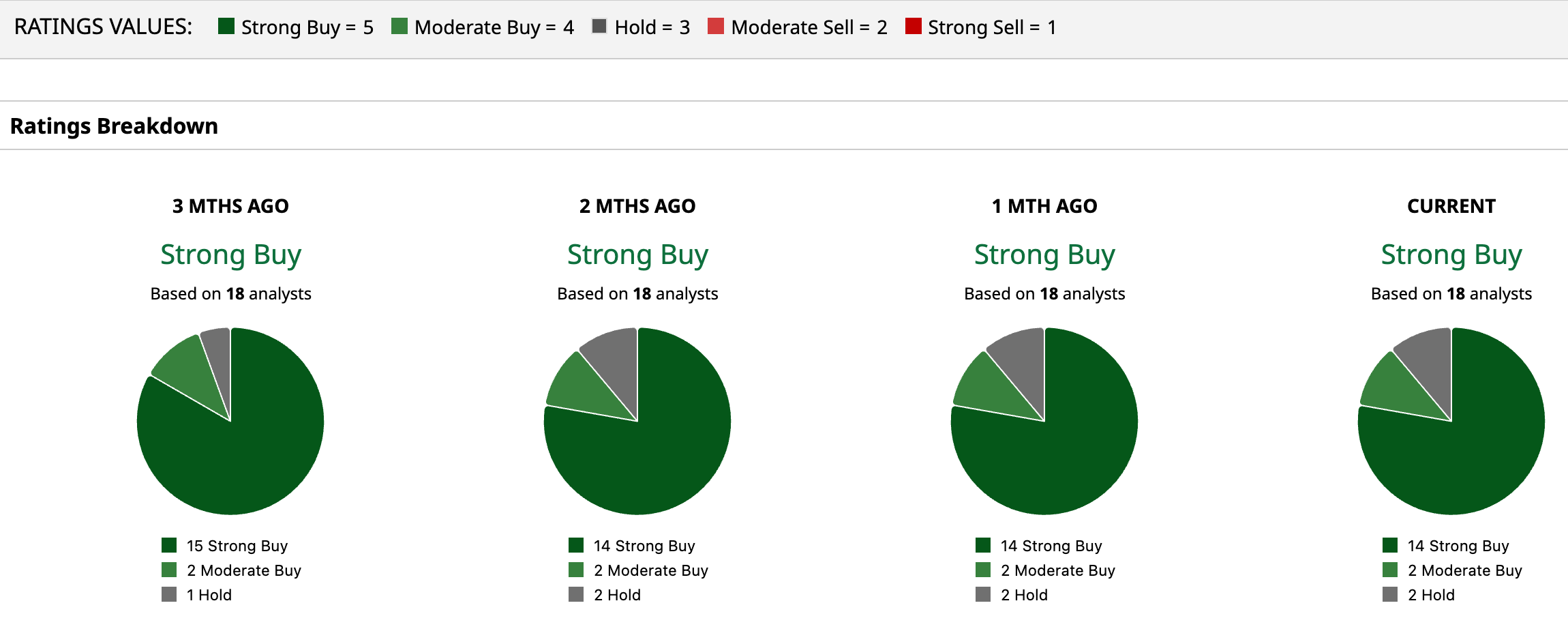

Analysts overall remain overwhelmingly bullish on TSM, with a solid “Strong Buy” consensus rating, reflecting strong confidence in its growth trajectory. Out of the 18 analysts with coverage, 14 recommend a “Strong Buy,” two advise a “Moderate Buy,” and two analysts maintain a “Hold” rating.

Based on Friday’s closing, the mean price target of $444.38 suggests that the stock has an upside potential of 12.5%. Meanwhile, the $600 Street-high target, set by Aletheia Capital in April, indicates that the stock could rally as much as 51.9% from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)