/The%20sign%20for%20Marvell%20Technology%20out%20front%20of%20a%20corporate%20office%20by%20Valeriya%20Zankovych%20via%20Shutterstock.jpg)

I previously wrote how Marvell Technology (MRVL) gained from the custom chip boom brought on by large language model training (LLM). For most of 2025, this was the company’s bull thesis. The more the hyperscalers spent, the more custom chip makers like Broadcom (AVGO) and Marvell (MRVL) benefited. With increasing investments in data centers, new bottlenecks started to emerge. The memory bottleneck, which caused stocks like Micron (MU) and SanDisk (SNDK) to surge higher and higher, is well known to investors. What some may not realize, however, is that the memory chip alone isn’t the issue. A lot of things need to come together to build that memory chip, and optical interconnects are one of them. Why am I pointing out the interconnects specifically? Because they’re what’s driving Marvell’s bull thesis now, not the custom chips.

Why Optical Networking?

The memory bottleneck didn’t just mean there weren’t enough memory chips around. The electrical connections that make these chips possible had hit their physical limit. Copper works well at lower speeds and shorter distances. AI now requires vast amounts of data to travel as fast as possible, giving rise to the need for optical interconnects. These transmit the data via light through fiber, making it possible to work with less latency and higher speeds. They have been around for some time, but artificial intelligence has helped spur their demand to unprecedented levels, and we're still at an early stage.

The emergence of optical interconnects means that when AI training and inference clusters are working, they can be kept busy at all times and do not have to wait for the data to arrive. This, in turn, removes a critical bottleneck. Marvell makes these optical interconnects and had previously forecast a 30% growth in their interconnects segment. They recently raised it to 50% for fiscal 2027. This has also confirmed that the company’s optics business isn’t just tied to cloud demand. Rather, it is dependent on the deployment cycles of the accelerators.

Gaining Strength Through Acquisitions

Marvell is also expanding its long-term optical networking ambitions through acquisitions. The Polariton acquisition was all about gaining exposure to plasmonic-based modulation technology that would become relevant once photonics moves from a niche infrastructure requirement to an everyday need for high-performance computing.

The Celestial AI acquisition was intended to fulfill the same ambition. The company will start contributing to MRVL’s bottom line in the second half of fiscal 2028, with management expecting $1 billion in revenue by Q4 of fiscal 2029.

About Marvell Stock

Marvell Technology offers data infrastructure semiconductor solutions for the networking, data center, storage, and communications markets. Its product portfolio includes interconnect, processors, networking, storage, and optical solutions. The company operates across the United States, Taiwan, India, Japan, China, Argentina, Singapore, Israel, South Korea, Vietnam, and international markets. It was founded in 1995 and is based in Wilmington, Delaware.

Over the last year, Marvell Technology delivered strong performance, generating returns roughly five times higher than the broader market. The stock climbed about 177%, while the S&P 500 gained around 27% over the same period. The strong rally has continued this year, with the stock more than doubling year to date. In comparison, the index gained about 9% only.

Marvell Beats Analysts Estimates

The company reported its fourth quarter FY26 earnings on March 5, beating both revenue and earnings estimates. Revenue for the quarter came in at $2.22 billion, representing 7% sequential and 22% year-over-year growth. Non-GAAP operating margin was 35.7%, while the non-GAAP gross margin was 59%. During the quarter, Marvell returned $200 million to shareholders through buybacks and $51 million in dividends.

The company increased its fiscal 2027 revenue guidance to $11 billion from $10 billion, driven by stronger demand in the data center segment. For FY27, data center revenue is expected to grow by 40% year-over-year, while the interconnect business is projected to grow by more than 50%. For the first quarter of FY27, revenue is estimated at around $2.4 billion.

The company is trading at a forward P/E of 48x, which is understandable considering it is expected to grow earnings at an average of around 40% over the next three years. On the May 27 earnings call, management will be able to give a better idea about the possibility of this growth rate increasing. If the optical interconnects segment of the business gets another mention, more and more traders could flock to the stock, benefitting the existing shareholders.

What Are Analysts Saying About Marvell Stock

Recent updates point to increasingly bullish sentiment among analysts on the stock. On May 13, RBC Capital analyst Srini Pajjuri raised the firm’s price target on the stock from $170 to $200 and maintained a “Buy” rating. On the same day, Bank of America Securities also increased its price target on the shares from $125 to $200 while reaffirming a “Buy” rating.

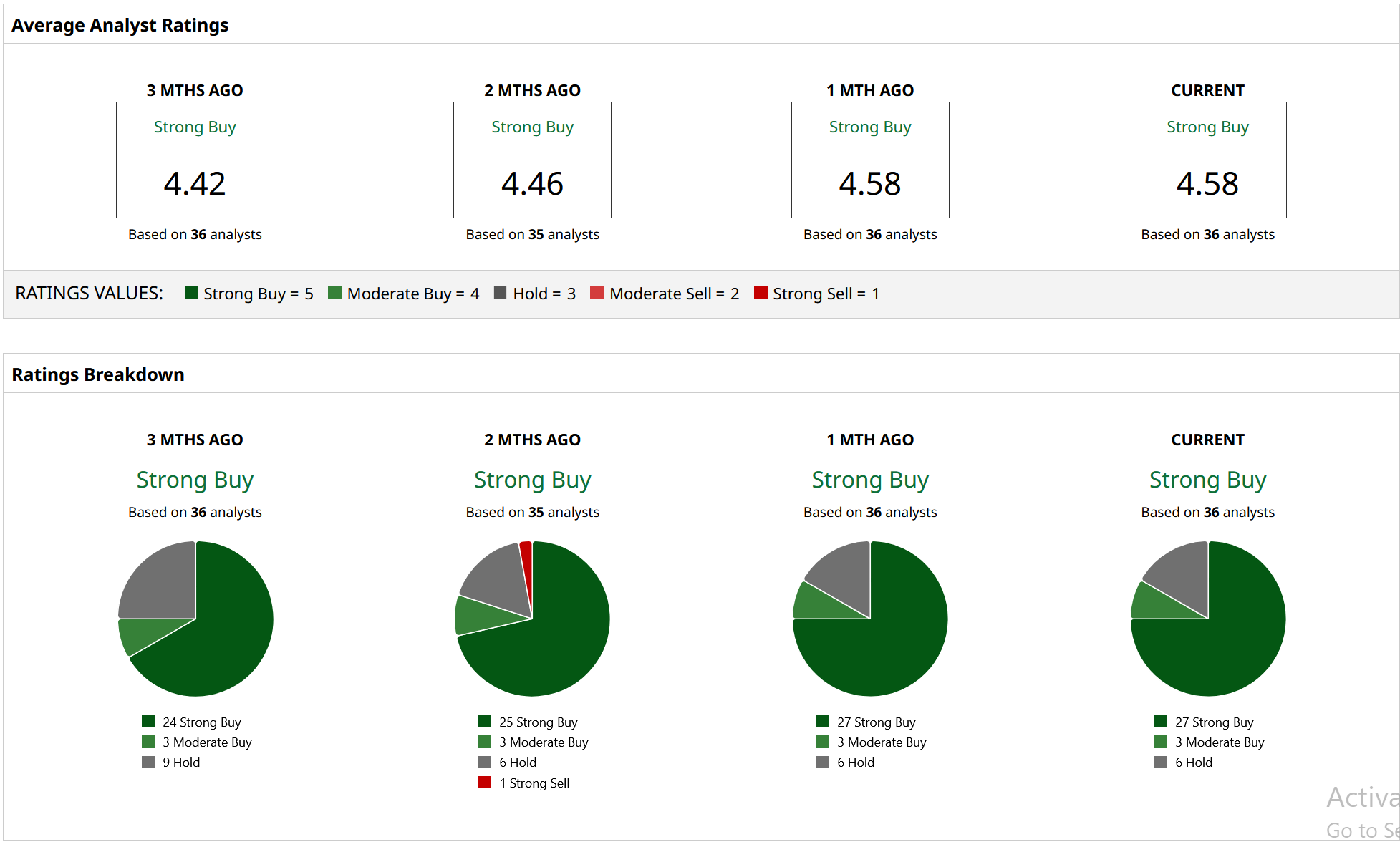

According to 36 Wall Street analysts covering the stock, it holds a consensus “Strong Buy” rating. Analysts’ estimates show a mean price target of $133.74, which has already been reached. However, the highest price target of $205 still implies 14% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)