/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)

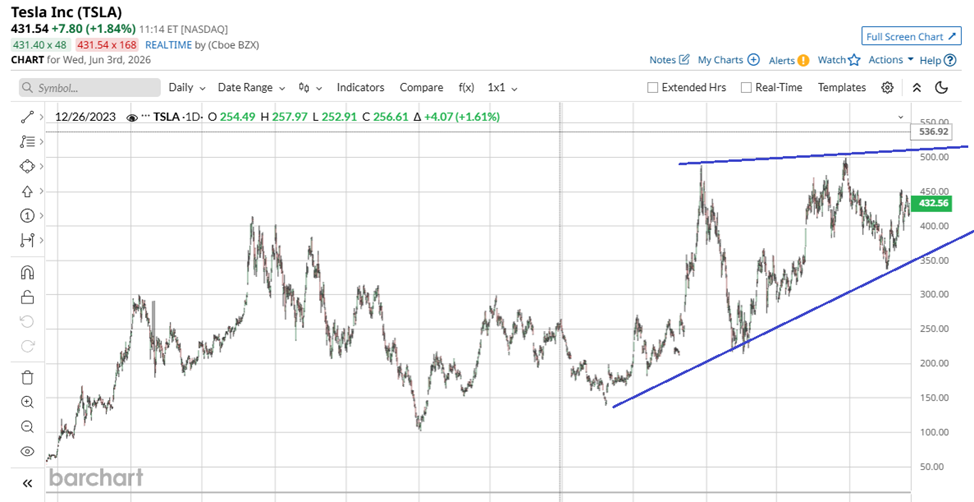

Since late 2024, Tesla (TSLA) shares have been stuck in a horizontal trading range. The stock is currently hovering near its 2021 peaks. Yet, the market values this prolonged three-year consolidation at a staggering $1.6 trillion in market capitalization.

Tesla’s current valuation seems downright absurd to any analyst digging into core fundamentals and traditional valuation multiples, at least if one views the company strictly as a car manufacturer.

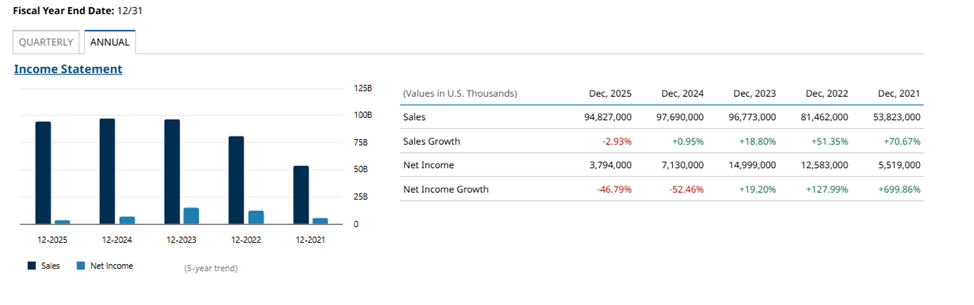

See for yourself: Revenue is simply treading water just below the $100 billion threshold, lingering somewhere in the $90 billion range. Profits are moving at a snail’s pace, and net automotive margins are continuously eroding under the weight of ongoing price wars. Meanwhile, the price-earnings ratio consistently skyrockets past 200x.

Evidently, the legacy automotive business is physically incapable of generating an operational cash flow that justifies such a massive valuation.

When buying at a P/E north of 200x, investors are not paying for existing factories, Model 3/Y sales volume, or even the relatively recently launched Cybertruck. This astronomical price tag is nothing more than a hefty call option on the future — a premium for projected dominance in AI and robotics.

Right now, the market is holding its breath, waiting for the Tesla Optimus project to materialize into something tangible. Investors desperately need a firm, concrete answer to the ultimate question: When will the first production-ready units roll out, and what exactly will this machine be capable of doing?

The ‘Couch Problem’: Dismantling Consumer Myths

There is still a prevailing, and in my view, flawed, narrative among investors that is heavily fueled by pop culture and sci-fi movies. The average person, and by extension the herd of inexperienced retail investors, firmly believes that a humanoid robot is destined to be a universal home assistant. Their imaginations paint a flawless picture: Optimus walks into an apartment, gracefully steps over scattered children’s toys, pours a fresh cup of coffee, settles onto a plush couch, and engages in casual small talk.

In my previous Barchart article regarding the “couch problem,” I detailed the fundamental physical and algorithmic barriers that make such a scenario completely unrealistic within the next decade.

Our chaotic everyday domestic environment is an absolute nightmare for computing systems governing embodied AI. Consider a soft couch changing its geometry under physical weight, a slippery rug, or a family dog suddenly darting across the room. In real time, every single one of these minor domestic variables triggers an endless cascade of critical processing errors.

This is precisely why long-term investors must execute a rigorous paradigm shift. The Optimus project is not yet a consumer gadget designed for the smart home. It is not a companion meant to stroll down public streets, and it is certainly not a universal humanoid operating with human-level general intelligence.

I view this project as a strictly industrial, B2B asset. Personally, I see the architecture of this venture as follows: for its first 10 years of commercial deployment, the market must evaluate Optimus exclusively as an anthropomorphic general-purpose machine tool. Expecting “domestic omnipotence” from it anytime soon is premature and economically illiterate. Tesla will win not because it is trying to make a robot smarter than a chaotic universe, but because it is radically simplifying the workspace environment to match the current thresholds of the technology.

The Concept: A Local ‘Cerebellum’

Where exactly is it supposed to work if Optimus cannot be let loose into our messy everyday lives just yet? The answer is straightforward: inside a structured “aquarium.” By this, I mean the highly standardized environment of a factory floor or a logistics terminal.

An assembly-line robot does not require full artificial general intelligence (AGI) to carry out repetitive tasks. It simply needs a predictable habitat that neutralizes the structural blind spots of modern neural networks. Take spatial geometry, for instance — a factory floor with an entirely flat surface, no door thresholds, fixed industrial lighting, and a total absence of sudden dynamic obstacles.

The robot navigates this environment using a localized navigational “cerebellum,” a computer vision framework that leverages the same algorithmic baseline as the vehicle-based full self-driving (FSD) autopilot. In a factory setting, the AI constructs a highly accurate 3D vector space map of a specific workstation just once. From that point forward, the robot memorizes the unchanging coordinates of the workbench, the storage rack, and the conveyor belt with absolute, unyielding precision.

Modern computing silicon is already fully capable of handling such a predictable spatial configuration. The operational demands placed on the “brain” drop to a strictly practical level: identify the component, adjust the hand trajectory by a couple of millimeters, and execute the grip.

Why then bother creating a bipedal humanoid instead of deploying a traditional industrial robotic arm? This boils down to a fundamental economic trade-off. Traditional hard automation — like the signature orange robotic arms from KUKA or Fanuc — requires massive upfront capital expenditures. Deploying them requires completely re-engineering the factory layout, erecting physical safety barriers, and ensuring hyper-rigid component feeding systems.

The humanoid form of Optimus was engineered with a singular objective: to deliver flexible automation within pre-existing human infrastructure. Our entire industrial world — from workbench dimensions to machine tool handles — was designed specifically around human anatomy. Optimus is built with two legs and two arms so that it can be plugged into an ordinary workstation right where a human laborer used to stand, without requiring any costly, disruptive overhauls of the factory floor.

The key takeaway here is that Tesla is building a commercial means of production. The primary objective of this hardware is the ability to replicate the baseline hand movements of a manual laborer at a workbench. For us as investors, the exact number of micro movements the robot can execute this calendar year is largely irrelevant. Our only objective is to see that it is conceptually fit to man an assembly line. If it can reliably stand at a workbench, assemble a Barbie doll, or stitch a pair of jeans, Tesla is golden. The technical framework to achieve this is already locked in.

The Ultimate Economic Duel: Optimus vs. Cheap Labor

When evaluating commercial viability, all technological enthusiasm must ultimately bend to cold financial arithmetic. In the global marketplace, Optimus’s primary adversary is not a high-tech rival from Boston Dynamics or a legacy industrial manipulator. Its true competitor is a living, breathing worker standing at an assembly line in Indonesia, India, Vietnam, or China.

For decades, Western corporations outsourced manufacturing to Asia driven entirely by the cost of labor per hour. Manufacturing apparel or assembling consumer electronics in the United States was economically unfeasible due to taxes, regulatory overhead, labor unions, and minimum wage mandates. Optimus has the genuine potential to upend this equation completely. It could morph into a hyper-profitable means of production.

Let us sketch out the financial model. Suppose that at its commercial B2B rollout, the unit cost of a single robot lands between $30,000 and $50,000. For a large-scale factory enterprise, this represents a perfectly acceptable capital expenditure (CapEx). Factoring in a conservative 10-year operational lifecycle with a standard 10% annual depreciation rate, the baseline hardware cost to the firm would amount to a mere $3,000 to $5,000 annually per unit.

Unlike a human employee, a robot can grind through three consecutive shifts, operating 24/7, pausing only for routine battery recharges and preventative maintenance. When translated into actual operational uptime (roughly 8,000 hours per year), the hourly cost of running an Optimus drops to a jaw-dropping $0.50 to $1.00. Even when layering in electricity costs and software licensing fees, this cost structure physically undercuts the price of manual labor in the most cost-competitive regions of Asia. This machine does not call in sick, go on parental leave, demand salary bumps, or file grievances, all while guaranteeing 100% quality replication.

The Macroeconomic Tsunami: Reshoring and Total Addressable Market

If the microeconomics of the robot hold up, it will spark a structural shift capable of rewriting the global division of labor. We are likely standing on the precipice of a massive reshoring wave — the wholesale repatriation of manufacturing capabilities back to developed economies.

Why would a multinational corporation bother shipping cargo containers full of electronics or footwear across entire oceans, exposing itself to geopolitical chokepoints and paying import tariffs? Assembling Barbie dolls or stitching garments via an army of Optimus units becomes fundamentally cheaper to execute directly inside Germany, Japan, or the United States, allowing factories to sit immediately adjacent to their core consumer markets. Supply chain transit times effectively drop to zero.

The addressable market size here quite literally defies imagination. Global macro demand for low-skilled, repetitive physical labor is practically bottomless. Over a 10- to 15-year horizon, the realistic global industrial demand could scale into tens, if not 100 million of these automated machines. Because a single robot operating around the clock physically replaces three distinct human shift workers, scaling production to tens of millions of units is mathematically equivalent to injecting hundreds of millions of optimized workers into the global labor force. Replacing 200 million factory floor workers over the next decade would allow the United States to systematically rebuild a domestic manufacturing engine equivalent to the entire industrial output of modern China.

What Could Go Wrong

Despite these breathtaking macro prospects, investors must immediately detach themselves from ungrounded hype. Optimus’s evolutionary path will be exceptionally grueling. Right now, Tesla is wading through its most perilous phase yet — a literal manufacturing hell.

To aggressively clear floor space for the third-generation assembly lines, the company took the drastic step of completely dismantling its legacy Model S and Model X production lines at the Fremont facility. Scaling will not happen overnight. The robot is an intricate assembly of more than 10,000 bespoke components. As Elon Musk pointed out, the overall velocity of a production line is dictated entirely by its slowest and “dumbest” component. Consequently, near-term output scaling will track a painfully slow S-curve.

Beyond initial manufacturing bottlenecks, the commercial B2B model faces two major engineering hurdles that institutional capital will be monitoring closely over the coming quarters. The first is Mean Time Between Failures (MTBF). The physical chassis relies on a highly complex network of dozens of actuators and mechanical cabling. If these components suffer from mechanical wear or snap every 40 hours under continuous 24/7 stress, factory operators will face financial ruin from maintenance overhead and assembly line downtime. Tesla must demonstrate flawless industrial-grade reliability.

The second core risk is the “gray area” software problem. A standardized factory floor is highly controlled, but what happens when a component arrives warped or a bin slips out of alignment? A human worker intuitively corrects the anomaly by hand. A robot operating on rigid, brittle algorithms under identical circumstances could freeze entirely or force a mechanical failure, damaging its tooling. This is precisely the operational gap that the Cortex 2.0 supercomputer is currently rushing to bridge. It is training neural networks to autonomously navigate minor, unscripted edge cases without forcing a hard shutdown of the entire production line.

Investment Summary

In my previous piece, when evaluating Optimus’s near-term odds of lounging on a living room sofa as a domestic sidekick, I maintained a highly skeptical posture. The market’s obsession with an illusory consumer rollout left Tesla shares highly vulnerable to repricing.

However, after a granular analysis of the company’s latest industrial adjustments and its decisive strategic pivot toward hard-nosed B2B commercial deployment, I believe a comprehensive structural re-evaluation is warranted. If one views Optimus strictly as a disruptive leap forward in universal industrial machinery, this venture possesses an authentic, monumental runway.

For long-term capital allocations, there is an immense, underappreciated growth vector embedded within the business model: SaaS (Software-as-a-Service). In the enterprise B2B space, no operator simply sells unmonetized hardware. Tesla’s primary margin capture will likely flow not from the point-of-sale hardware invoice, but from high-margin monthly recurring software subscriptions. These will govern ongoing neural network optimization, the deployment of newly learned industrial workflows, and the centralized fleet management of entire robotic workforces. The gross margins of enterprise software historically dwarf legacy automotive manufacturing. This dynamic alone could transform Tesla into the largest B2B platform on the globe.

For investors who are fully cognizant of the operational head-winds, understand the brutal complexities of this manufacturing curve, and possess the patience to wait out the initial S-curve ramp-up at Fremont, my stance is clear: Tesla stock can be cautiously purchased at these levels.

The ongoing multi-year consolidation tracked on the TSLA chart is very likely the quiet before a massive tectonic breakout. This is no longer a speculative wager on a sci-fi consumer miracle walking our streets. It is a calculated, pragmatic bet that Tesla will be the first to commercialize general-purpose anthropomorphic machines that will permanently reshape global macroeconomics. They are poised to transform manual labor into a highly accessible, commoditized utility — as cheap and ubiquitous as standard grid electricity.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)