/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Memory stocks have had a horrible few days since Alphabet (GOOGL) came out with its TurboQuant algorithm. If the memory bottleneck problem is solved, it could spell trouble for all the investors and analysts who were pricing in unprecedented memory demand. However, one research firm believes the market is overreacting and that the TurboQuant development will have little impact on memory demand.

Analysts at Bernstein believe HDD demand won’t budge as a result of Google’s new algorithm, while NAND memory demand may only be slightly impacted. In the past few days, people have adopted a “sell first, ask questions later" approach. This has created an attractive valuation for those willing to take a position in memory stocks, especially SanDisk (SNDK). Bernstein now has a $1,000 price target on SNDK stock.

About SanDisk Stock

SanDisk is a multinational company headquartered in Milpitas, California that specializes in developing, manufacturing, and selling data storage technologies. The firm uses NAND flash technology for this purpose, providing solid-state drives for gaming consoles, desktops, and PCs, with core offerings spanning USB drives, flash-based embedded storage products for various wearable and portable devices, home applications, automotive applications, and more.

SNDK stock has returned 1,371% over the last 12 months, mainly due to restricted supply and massive demand for memory products because of AI workloads. However, the stock saw a drawdown in March, which is what created the recent buying opportunity.

SNDK stock should continue to grow through the end of 2027, with earnings growth of 133% expected in fiscal 2027. This is on top of the 2,000% earnings growth expected in fiscal 2026. The question, however, is where will the company go once memory demand settles down?

Investors currently pay a forward earnings multiple of 15.6 times for the stock, which is a fair valuation and reflects that the market isn’t as optimistic on memory demand continuing as many might suggest. Looking at the expected earnings growth numbers and memory demand, though, one is likely inclined to buy SNDK at whatever the market values it right now.

Another reason in favor of the bulls is SanDisk's healthy free cash flow. The company reported free cash flow of $1.45 billion in the last 12 months.

SanDisk Continues to Post Strong Earnings

SanDisk announced its second-quarter fiscal 2026 earnings on Jan. 29. Revenue came in at $3.03 billion, beating the company’s early guidance and representing a 31% increase from the previous quarter and a 61% year-over-year (YOY) rise. Segment performance included $1.68 billion in edge revenue, $907 million in consumer revenue, and $440 million in data-center revenue. Data-center revenue also grew 64% sequentially.

Non-GAAP gross margin rose to 51.1% from 29.9% in the prior quarter, while non-GAAP operating margin increased to 37.5% from 10.6% in the prior quarter. The company closed Q2 with $1.54 billion in cash and $603 million in debt, following a $750 million reduction in its debt.

For Q3, SanDisk expects revenue to be in the range of $4.4 billion to $4.8 billion. This projection is supported by management's view that the market is more undersupplied compared to the second quarter. Non-GAAP operating expenses are forecast to range from $450 million to $470 million, while non-GAAP gross margin is projected at 65% to 67%. Non-GAAP EPS is anticipated to range from $12 and $14. The company will report fiscal Q3 earnings on April 30.

What Are Analysts Saying About SanDisk Stock?

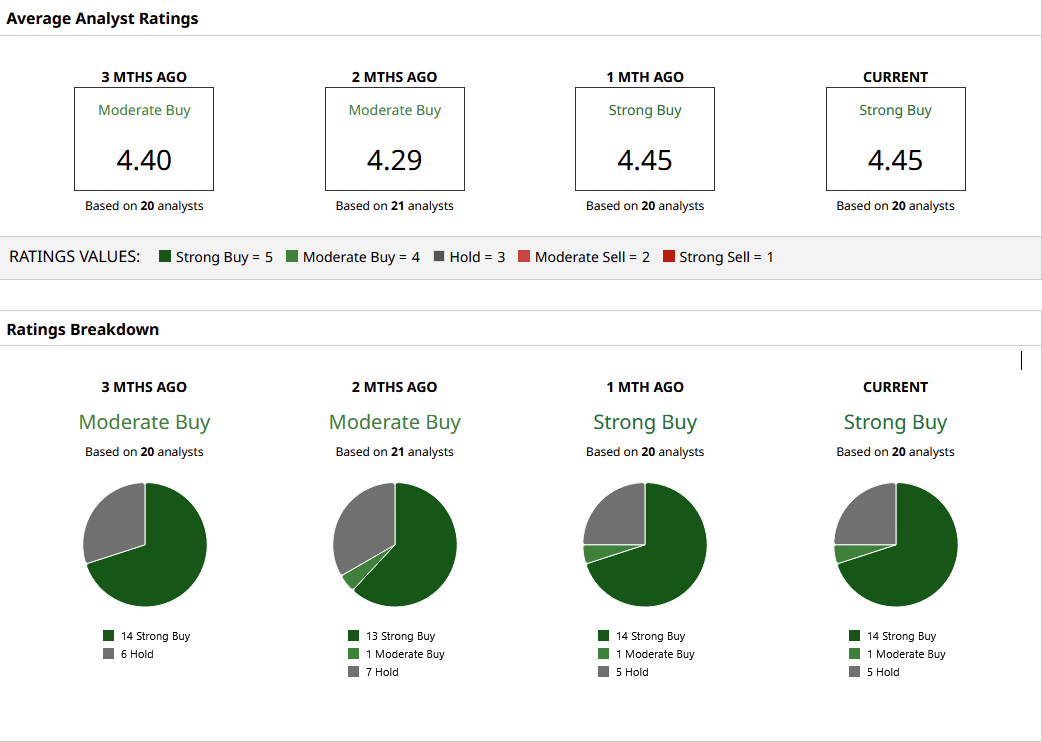

Like Bernstein, Citi also assigned a “Buy” rating on SanDisk shares along with a price target of $875. Of 20 analysts covering SNDK stock on Wall Street, 14 have a “Strong Buy” rating, one has a “Moderate Buy," and five analysts have a “Hold.”

The mean target price of $752.24 offers only 7% potential upside from current levels. However, Bernstein’s Street-high price target of $1,000 suggest the stock could rise as much as 43% from here. If Bernstein analysts are right, SNDK stock is clearly a buy.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)