Alphabet’s (GOOGL) introduction of TurboQuant, a new compression algorithm designed to reduce memory requirements in large language models (LLMs), has created uncertainty for memory chip manufacturers, including SanDisk (SNDK). The technology improves efficiency by reducing the memory required to run artificial intelligence (AI) workloads, raising concerns about the future trajectory of demand for high-performance memory components.

Memory stocks, which have already witnessed a very strong run, came under pressure on the news. SanDisk, a key beneficiary of the AI-led demand, fell 11% on March 26. Notably, SNDK stock has delivered exceptional gains so far this year, rising 158% year-to-date (YTD) and surging 530% in the past six months. This rally has been driven primarily by strong demand linked to the rapid expansion of AI data centers, where memory products play a critical role in supporting compute-intensive applications.

However, the emergence of more efficient algorithms, such as TurboQuant, introduces a potential structural shift. If AI systems require less memory to operate at scale, demand growth for memory chips could moderate over time.

Despite these risks, near-term fundamentals for memory chip companies remain supportive. Industry-wide supply constraints, combined with sustained demand from AI infrastructure buildouts, are expected to support strong financial performance in the short term. While efficiency gains may influence long-term demand dynamics, current market conditions suggest that memory producers like SanDisk are still positioned to benefit from ongoing AI-driven investment cycles.

SanDisk to Sustain Growth Momentum

SanDisk is positioned to sustain strong growth, supported by accelerating investment in AI infrastructure. Hyperscale cloud providers are increasing capital expenditures to expand AI-focused data-center capacity, driving a parallel rise in demand for high-performance storage.

Moreover, SanDisk is experiencing strong demand from a broad range of end markets, including enterprise data centers, edge infrastructure providers, OEMs, and system integrators developing AI-ready systems. This diversification enhances revenue visibility while reducing customer concentration risk. Management expects the data center segment to remain a key growth driver, supported by durable, structural demand trends.

In edge and consumer markets, supply-demand dynamics remain favorable. Replacement cycles in PCs and mobile devices, combined with the integration of AI-enabled features, are pushing device configurations toward higher storage capacities. Demand has outpaced supply in recent quarters, enabling SanDisk to benefit from both increased shipment volumes and stronger pricing. At the same time, a shift toward premium products and higher-value configurations is supporting margin expansion alongside revenue growth.

Looking ahead, SanDisk anticipates demand will continue to exceed available supply through at least calendar year 2026. This sustained imbalance is expected to support favorable pricing conditions and improved operating leverage, positioning the company for meaningful revenue and earnings expansion in fiscal 2026 and 2027.

For the upcoming third quarter, SanDisk forecasts revenue between $4.4 billion and $4.8 billion, implying sequential growth of 45% to 58%. Profitability is also expected to improve significantly, with adjusted gross margins projected in the range of 65% to 67%. Adjusted EPS is estimated between $12 and $14, with the midpoint indicating the potential for more than a doubling of earnings on a sequential basis. These projections support a constructive outlook for the company’s near-term financial performance.

Is SNDK Stock a Buy, Sell, or Hold?

Google’s TurboQuant introduces uncertainty into long-term memory demand by improving AI workload efficiency, but it does not immediately disrupt the current upcycle benefiting memory manufacturers like SanDisk. Near-term fundamentals remain firmly intact, supported by tight supply conditions, sustained hyperscaler spending, and broad-based demand across data center, edge, and consumer segments.

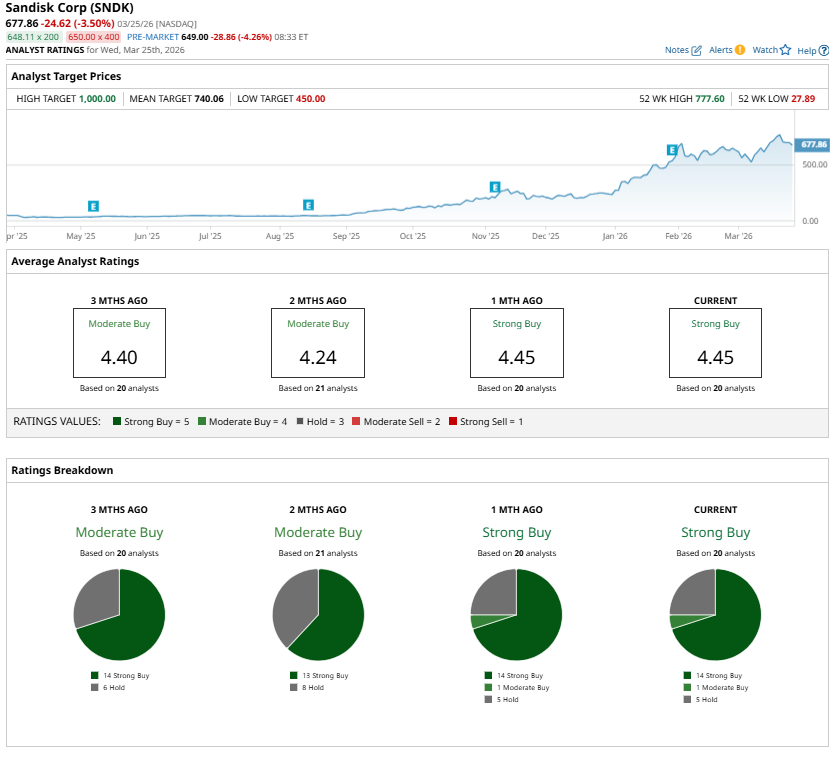

Overall, SanDisk appears well-positioned to sustain momentum in the near to medium term. Analysts remain optimistic and maintain a “Strong Buy” consensus rating, reflecting confidence in the firm’s ability to expand margins and deliver strong earnings.

However, as SNDK stock has rallied significantly, investors sitting on substantial gains may choose to book profits.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)