June WTI futures prices are slowly moving higher, over $99 late Monday (May 11). Two ways to play oil are to sell short out-of-the-money (OTM) one-month expiry Chevron Corp (CVX) calls or short OTM CVX puts.

I discussed this last month in a Barchart article for the May 15 expiry $220 call option contract. It has worked out well. This article discusses a new short-call play for expiration on June 18.

CVX closed at $184.74 on Monday, May 11, up 1.72%, but well off its recent peak of $211.15 on March 27. However, it's up from a recent 4-month trough of $181.62 last Friday (May 8).

Note also that oil futures prices are starting to move higher after hitting a trough on April 17 ($82.93) and peaking at $106.65 on April 29. This can be seen in Barchart's chart on the June 2026 WTI futures contract below.

Tensions in the Iran war are not over, and it's possible that oil could remain elevated until U.S. warships leave the Persian Gulf area.

The point is that CVX stock is a good proxy for the one-month futures contract. So, it's a lot easier to short one-month expiry out-of-the-money (OTM) puts and calls in CVX than speculating in the oil futures.

Shorting OTM CVX Calls

I discussed this play in an April 7 Barchart article, “Oil Futures Keep Rising, and Shorting Chevron Covered Calls and Cash-Secured Puts Works.”

I discussed selling May 15 expiry covered calls at the $220 call option strike price when CVX was at $198.86. The midpoint premium received by short-sellers at the time was $1.85.

That means the short-sellers made a covered call yield of about 1%:

$1.85 / $198.96 = 0.0093 = 0.93% for a strike price 10.63% over the spot price (i.e., $220/$198.86)

The $210 call option, i.e., 5.60% over the trading price, had a higher yield:

$3.97 / $198.96 = 0.02 = 2.0% yield

Today, those premiums have fallen to just 3 cents and 1 cent, respectively. So, this has been an attractive and profitable play.

Now, the June 18 expiry call option has attractive short-call plays. For example, the $200.00 strike price call option has a $1.76 midpoint premium. That represents a covered call yield of almost 1% for an 8.26% higher sale price (i.e., $200/$184.74):

$1.76 / $184.74 spot price = 0.0095 = 0.95% one-month yield

Moreover, for investors willing to sell their shares at a lower price, i.e., $195.00 or 5.55% over the spot price, the yield is higher:

$2.64 / $184.74 = 1.43%

So, on average, if an investor owned at least 200 shares and sold 2 covered calls at each strike price, the total income would be $440, or $2.20 per call with an average strike of $197.50:

$2.20 avg income / $197.50 avg call strike = 0.01114 = 1.114% yield over the next month

Note that the average delta ratio is almost 0.24, implying less than a 24% chance that CVX will rise to these strike prices. As a result, this is an attractive way for existing investors to generate income from their CVX shares.

Shorting OTM Puts

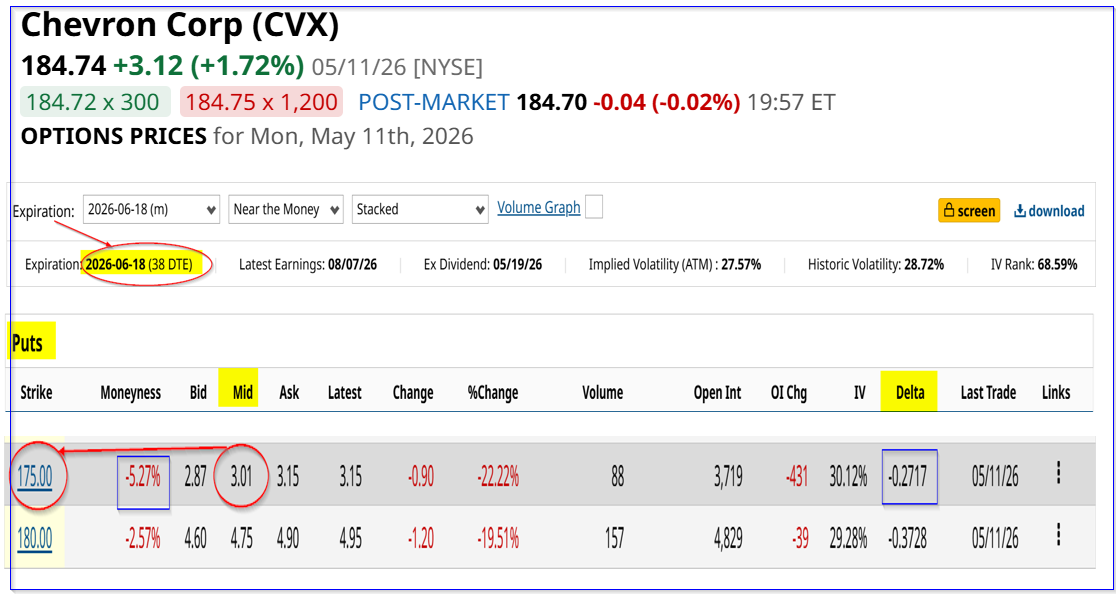

Another play, especially for investors who don't already own CVX shares, is to sell short out-of-the-money CVX puts. For example, the $175.00 strike price put option has a midpoint premium of $3.01. That provides a 1.72% income yield to the short-seller:

$3.01/ $175.00 = 0.0172 = 1.72%

Note that this strike price is 5.27% lower than the spot price. However, it has a higher yield than the $190 call option, which is 5.55% higher than the trading price and has a 1.43% one-month yield (see above).

That is why it could make sense for some investors to sell short CVX OTM puts rather than covered calls. In any case, whether shorting OTM calls or OTM puts, it's much easier and a more efficient oil play compared to trading WTI futures contracts.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.