/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

Memory stocks slipped on Wednesday, March 25, even as the broader technology sector held steady, and the pressure showed up in Micron Technology (MU). The stock fell 3.4% after Google introduced TurboQuant, a compression algorithm designed to reduce memory consumption in artificial intelligence (AI) systems.

TurboQuant directly targets inefficiencies in the key-value cache, a critical component that stores frequently accessed data in AI workloads. The algorithm also demonstrated up to an 8x performance improvement over unquantized keys on NVIDIA Corporation (NVDA) H100 GPU accelerators, highlighting a meaningful leap in efficiency.

Investors moved quickly to interpret the implications for Micron. If AI systems can deliver more output with less memory, the long-term demand trajectory for memory chips could moderate. The concern triggered a broader sell-off across memory stocks, with Micron at the center of the reaction given its direct exposure to AI-driven demand.

Against this backdrop, let us discuss whether the decline points to emerging weakness in Micron’s story. Or does it present a window for long-term investors to step in while sentiment cools?

About Micron Stock

Best known for its memory chips, Micron designs and manufactures dynamic random-access memory (DRAM), NAND flash memory, and storage solutions that sit at the heart of data centers, personal computers (PCs), smartphones, and automobiles.

The company commands a market cap of approximately $400.9 billion and operates at the center of the AI infrastructure buildout, where high-performance memory has become indispensable.

The stock has delivered a remarkable run. Shares of the Boise, Idaho-based company have skyrocketed 293.6% over the past 52 weeks and gained 128.2% in the last six months.

Still, momentum rarely moves in a straight line. The stock fell 15.15% in just the last five trading days as a series of volatile developments weighed on investor sentiment.

From a valuation standpoint, MU stock is currently trading at 6.89 times forward adjusted earnings. The figure is trading below both the industry average and its own five-year average multiple. The gap signals a discount and hints at a more measured entry point.

On the income front, Micron currently pays an annual dividend of $0.60 per share, which translates to a dividend yield of 0.16%. On March 18, the company raised its quarterly dividend by 30% to $0.15 per share, payable on April 15, to shareholders on record as of March 30.

Micron Surpasses Q2 Earnings

Micron delivered a standout fiscal 2026 Q2 performance on March 18. Revenue rose 196.3% year-over-year (YOY) to $23.9 billion, beating the $19.9 billion Street forecast. The growth came from record performance across DRAM, NAND, and high-bandwidth memory, all supported by strong AI demand and firmer pricing.

The company translated that demand into profitability. Non-GAAP operating income grew 719.9% from the year-ago value to $16.5 billion, while non-GAAP net income rose 686.4% from the previous year’s quarter to $14 billion. Non-GAAP EPS climbed 682.1% YOY to $12.20, surpassing analyst estimates of $8.80.

Adjusted free cash flow totaled $6.9 billion, showing that earnings strength flowed directly into cash generation. Micron closed the quarter with $16.7 billion in cash, marketable investments, and restricted cash, giving it flexibility to fund expansion.

Management plans to increase spending to meet persistent demand, with construction-related costs expected to exceed $10 billion this year. Additionally, the company is building capacity in the U.S., including fabrication plants in Idaho and New York. Its $100 billion New York campus remains on track for operations in the second half of 2028.

In terms of guidance, Micron’s management projects Q3 fiscal 2026 non-GAAP revenue of about $33.5 billion, with a possible variation of $750 million on either side. Non-GAAP EPS is projected at roughly $19.15, with a potential swing of $0.40.

Analysts largely track the outlook. They forecast Q3 fiscal 2026 EPS of $18.97, reflecting a 996.5% YOY increase. For the full fiscal year 2026, estimates call for 651% growth to $57.70, followed by another 67% rise to $96.55 in fiscal year 2027.

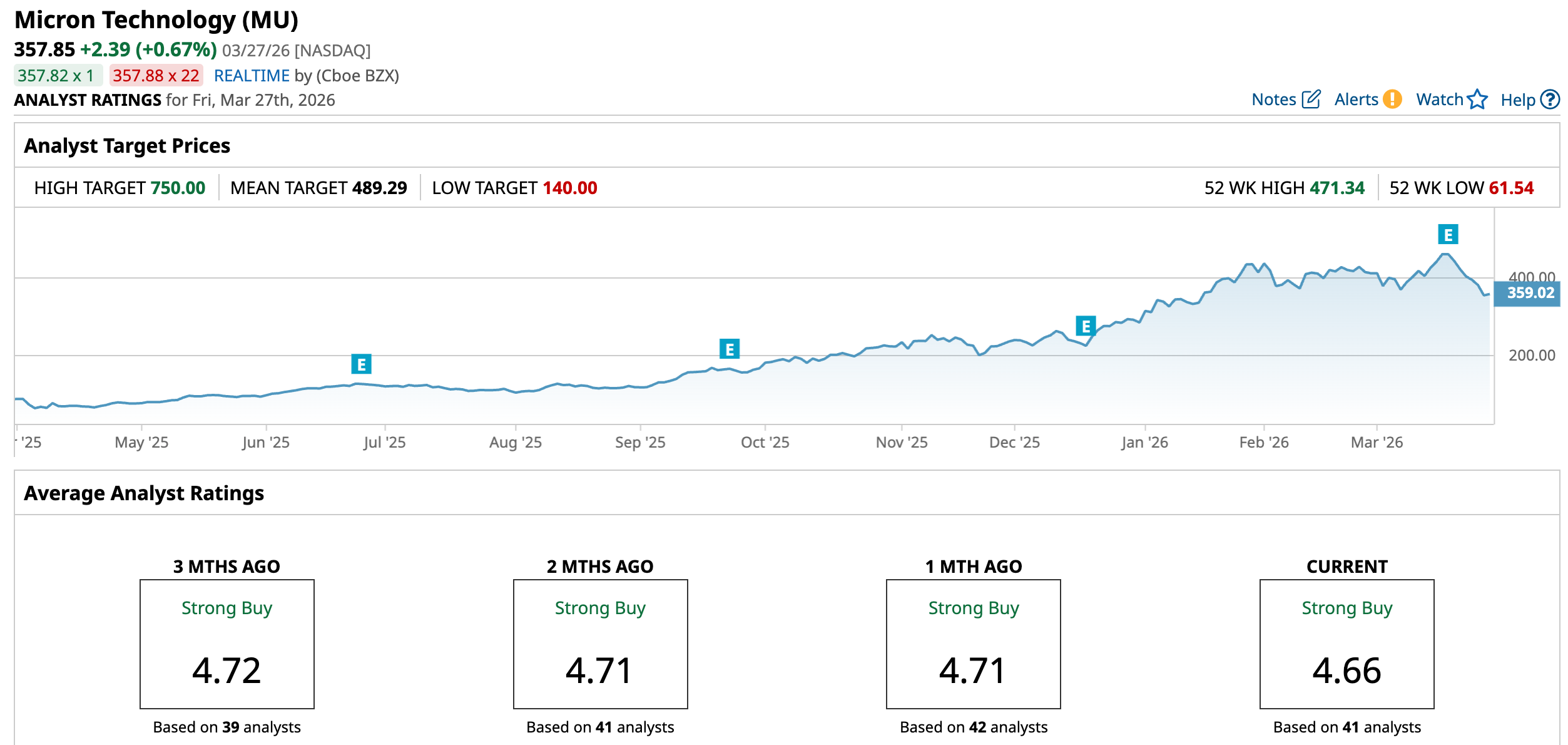

What Do Analysts Expect for Micron Stock?

Wall Street continues to show conviction in Micron, and recent analyst moves underline that stance. Bank of America raised its price target to $500 from $400 after the latest quarterly results, signaling stronger confidence in the company’s trajectory.

Mizuho Financial Group also lifted its price target from $480 to $530, pointing to robust profitability and a clear roadmap across DRAM and NAND. The firm kept an “Outperform” rating on the shares. Meanwhile, JPMorgan Chase took an even more optimistic view, increasing its target from $350 to $550 while maintaining an “Overweight” rating.

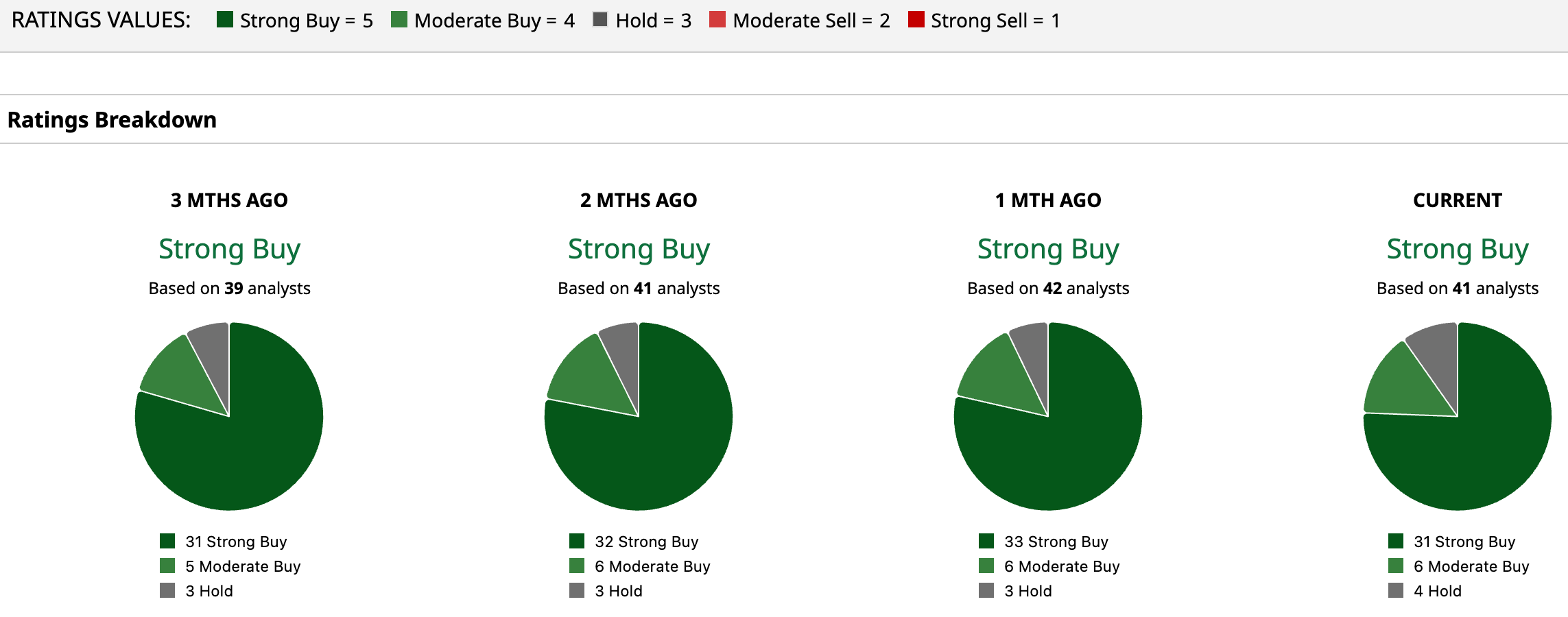

Currently, Wall Street has assigned MU stock an overall rating of “Strong Buy.” Among 41 analysts covering the stock, 31 rate it a “Strong Buy,” six have issued a “Moderate Buy,” while four recommend “Hold.”

To that end, the average price target of $489.29 implies potential upside of 36.7%. Meanwhile, the Street-high target of $750 points to a possible gain of 109.6% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)