Shares of Super Micro Computer (SMCI) have surged more than 85% over the past month. The rally in SMCI stock reflects growing investor confidence in the company’s strong positioning in the booming artificial intelligence (AI) infrastructure market.

The AI spending wave continues to gain momentum, and recent results from industry peers suggest demand is accelerating. Dell Technologies (DELL), for example, reported first-quarter revenue growth of 88% year-over-year, driven by exceptionally strong demand for AI servers. Dell generated $24.4 billion in AI-related orders and $16.1 billion in AI server revenue, highlighting the enormous opportunity across the AI infrastructure ecosystem.

As a leading supplier of high-performance AI servers and storage solutions, Supermicro appears well-positioned to capitalize on this trend. The company is benefiting from a strong product portfolio, improving profitability, and expanding opportunities through its Data Center Building Block Solutions (DCBBS) platform.

However, after such a strong rally, does SMCI stock still have meaningful upside ahead?

Strong AI Demand Positions Supermicro for Sustained Revenue Growth

Supermicro appears well-positioned to deliver strong growth going forward, as demand for AI infrastructure remains robust across enterprises, cloud providers, and government-backed AI initiatives.

In the third quarter of fiscal 2026, Supermicro generated revenue of $10.2 billion, representing an impressive 123% increase from the prior year. While customer deployment delays and global component shortages weighed on sequential growth, management indicated that much of the delayed revenue is expected to be recognized in the coming quarters.

Notably, demand remains exceptionally strong. Orders and backlog continued to expand during the quarter as organizations accelerate investments in AI infrastructure. AI GPU platforms now account for the majority of the company's revenue, reflecting Supermicro's growing share within the rapidly expanding AI ecosystem.

One of the most encouraging developments is the company's growing traction with enterprise customers. Enterprise revenue reached $2.8 billion during the quarter, accounting for approximately 28% of total revenue, up from 15% in the previous quarter. The segment grew 46% year-over-year and 45% sequentially, suggesting that AI adoption is broadening beyond hyperscale cloud providers and becoming increasingly widespread across enterprises.

Meanwhile, revenue from OEM appliances and large data center customers totaled $7.4 billion, representing 72% of quarterly revenue. Although this business experienced a sequential decline due to deployment timing, revenue still surged 183% year-over-year. The performance highlights that demand for AI infrastructure remains exceptionally strong.

The rising contribution from enterprise customers could become an increasingly important driver of long-term value creation. A broader customer base helps diversify revenue streams and reduces dependence on a relatively small group of hyperscale customers, potentially making future growth more balanced and resilient.

Beyond revenue growth, Supermicro is also focused on expanding profitability through its DCBBS strategy. By delivering complete data center solutions, including liquid cooling infrastructure, networking, management software, and related services, SMIC is moving beyond hardware sales and increasing its share of customer spending. This integrated approach strengthens customer relationships and creates opportunities for higher-margin revenue streams.

At the same time, Supermicro continues to strengthen partnerships with major suppliers, particularly Nvidia (NVDA), while improving factory automation, manufacturing efficiency, and product mix. These investments should support faster production, better yields, and improved profitability.

Is SMCI Stock Still a Buy?

Supermicro Computer remains one of the top beneficiaries of the AI infrastructure boom. The company is expected to deliver robust growth as enterprises and hyperscale data center operators continue ramping up investments in AI servers and related hardware.

Demand for Supermicro's high-performance servers and storage solutions remains strong, helping fuel impressive revenue growth. However, investors should not overlook customer concentration risk.

In its most recent quarter, a significant portion of revenue came from two customers. One large data center customer accounted for 27% of total revenue, while a single enterprise customer contributed another 10%. Although management is actively working to broaden its customer base, heavy dependence on a few major clients could create revenue volatility if spending patterns change.

Competition is another factor to watch as it could increase pricing pressure and potentially weigh on margins over time.

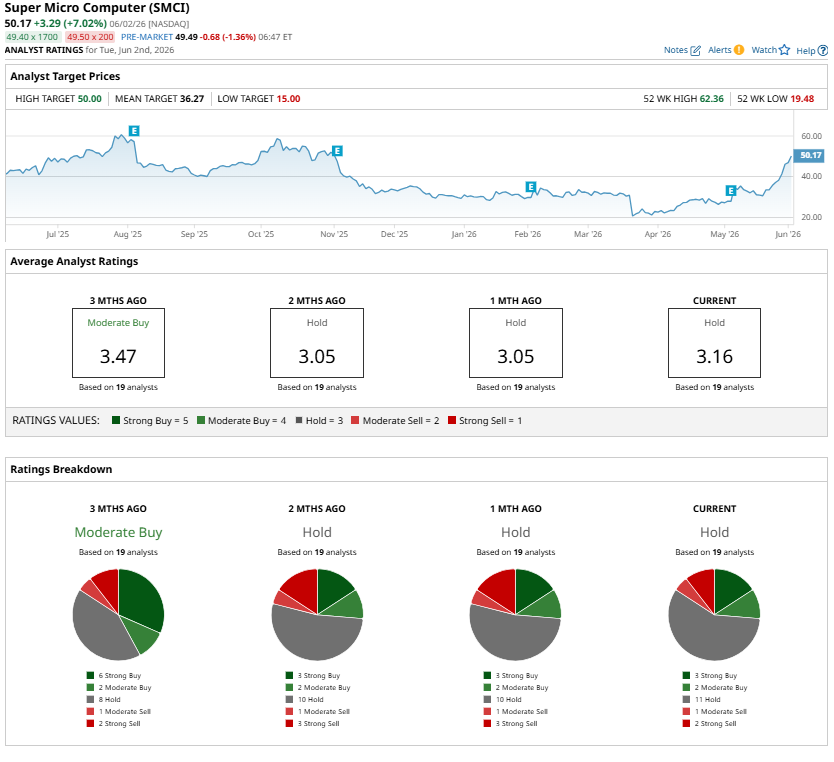

Investors should also consider valuation. SMCI stock has delivered substantial gains, indicating that positives are already priced in. Wall Street analysts currently maintain a “Hold” consensus rating, suggesting that while the company's long-term growth prospects remain attractive, the stock is offering a less favorable risk-reward at current levels.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Palo%20Alto%20Networks%20headquarters%20campus%20exterior%20of%20cybersecurity%20company%20By%20MichaelVi.jpeg)