/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

With reports coming out that Alphabet (GOOG) is delaying the release of its updated flagship AI model, it was inevitable that GOOG stock suffered a sizable loss in response. Fundamentally, the concern is that with myriad companies pushing ahead with their AI initiatives, Google will fall further behind. As such, the options market has responded with pessimism, with the smart money prioritizing downside protection.

Still, there’s good reason to hold the line with GOOG stock, especially with Alphabet scheduled to release its second-quarter earnings report (on July 22 after the market close). Primarily, Google enjoys the “everywhere moat.” Because the tech giant’s services — Search, YouTube, Gmail, Android, Maps and Docs — are deeply embedded in the daily lives of billions of users, this ubiquity provides a unique, unparalleled data advantage that competitors struggle to replicate.

In other words, Google isn’t focused on trying to build a new audience; rather, it has the arguably easier job of integrating AI into these existing platforms to drive engagement and monetization. Through features like AI Overviews and AI Mode, Google has reportedly increased user engagement and search queries, allowing for more precise ad targeting and monetization opportunities for complex queries that were previously difficult to address.

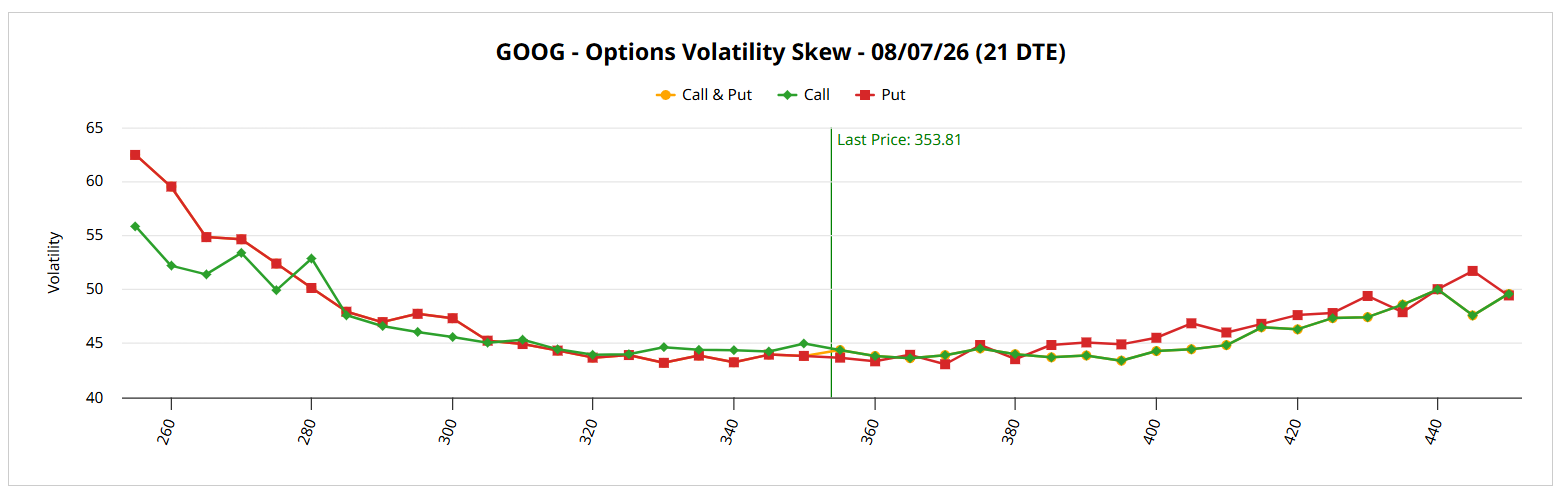

Still, the smart money doesn’t seem all that convinced that the broader narrative undergirding Alphabet stock is enough to overcome the AI latency concerns. If you look at the volatility skew for the options chain expiring Aug. 7, the screener is shaped like a “smirk” — demand is concentrated on far out-the-money (OTM) puts (or the left side of the chart) more so than far OTM calls.

Naturally, the classic interpretation of this skew is bearish or at least cautious. However, if you have good reason to be bullish on GOOG stock, it may be a shrewd opportunity because you would be paying for a relative discount on volatility.

Justifying the Mispricing Argument for GOOG Stock

Mechanically, the reason that short-term options traders should consider the bullish case for Alphabet stock is the dominance of algorithmic, rules-based protocols. In the modern equities market, as soon as information becomes public, the news is immediately digested and acted upon. Such engagement occurs in nanoseconds — a paradigm that is simply inaccessible to human traders.

As such, there may be more benefit in anticipating how the machines may react versus how humans may respond. Frankly, the latter may be impossible to decipher given the diversity of incentives and various psychological pressures. However, while I wouldn’t say the former is easy, deciphering this category may be more viable because of the structural footprints left behind.

For example, when a quality name like GOOG stock suffers an extended downturn, I believe it’s reasonable that trading algorithms will view the ticker as a relative discount. Because they’re operating on quantitative rules, these bots could be the first ones in and the first ones out.

Here’s what’s interesting. In the last 10 weeks, GOOG stock has only printed three up weeks, leading to a downward slope. This 3-7-D sequence is rare, having only materialized 11 times on a rolling basis since January 2019. When this signal occurs, GOOG historically leaves a structural footprint — something that we can measure.

When conditioned for this signal, the expected forward 10-week distribution is between $343 and $390 (assuming a starting price of $353.81), which is a very similar distribution relative to the random baseline. However, the interesting part is that the performance variance between the two distributions is not orderly and linear.

Specifically, on week 3 following the flashing of the aforementioned signal, Alphabet stock tends to rise about 4.29% relative to the starting price as a median outcome. In contrast, buying GOOG randomly would only be expected to see a 2% rise by that time period.

Essentially, then, options trades for week 3 — which approximately corresponds with an expiration date of Aug. 7 — could be underpriced relative to the historical risk that traders typically absorb.

Pinpointing a Contrarian Options Spread

As I mentioned earlier, the volatility skew for the Aug. 7 expiration date leans toward downside protection (higher demand for OTM puts) probably because of the AI latency issue. However, if that earnings release contains surprisingly positive data, there’s a chance that Alphabet stock could swing to the upside. Moreover, extended downturns in GOOG stock have historically generated above-average performances over the next three weeks.

With those factors in mind, I’m interested in the aggressive 365/370 bull call spread expiring Aug. 7. Featuring a relatively low net debit of $235, there’s only a limited margin for error. Basically, GOOG stock must rise through the $370 strike at expiration to trigger the max payout of 112.77%. But for me, what makes this trade enticing is the breakeven price of $367.35.

Right now, the market is assigning a probability of profit (the chance that GOOG stock will reach break even at expiration) of only 36.5%. That’s using the Black-Scholes model, which takes the variable input of implied volatility and runs it through a risk-neutral, lognormal formulation. The implied probability stems from the distance (in standard deviations) the target price is from the current spot price.

However, my data — which operates on a what-you-see-is-what-you-get methodology — shows that of the 11 times that the 3-7-D signal flashed, GOOG stock rose above the equivalent of the $367.35 breakeven price six times on week 3. Setting aside the glaring issue of extremely small sample sizes, there’s a case to be made that the conditionally observed probability of profit is 54.5%.

What does a gap of 1,800 basis points of “free probability” look like? Consider the 310/370 bull spread for the same expiration date — the probability of profit is 54.4% and traders must pay a net debit of $3,955! I don’t know about you but if I’m getting the same probability, I’d rather pay a little over 200 bucks than nearly 4,000 bucks.

Of course, because of the small sample size, I don’t have as much confidence in GOOG stock as I might in other trades. However, if the implications are to be trusted, there are a lot of free odds that aggressive speculators may be able to exploit.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/A%20corporate%20office%20for%20IBM%20by%20HJBC%20via%20Adobe%20Stock.jpeg)