/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

After years of frustrating investors and slipping further behind in the artificial intelligence (AI) race, Intel Corporation (INTC) is suddenly emerging as one of the stock market’s most remarkable turnaround stories. The legendary chipmaker spent much of the past few years battling manufacturing setbacks, strategic execution issues, and intensifying competition from AI powerhouses like Nvidia (NVDA) and Advanced Micro Devices (AMD). Conditions deteriorated so badly that Intel was forced to slash its dividend in 2023 before suspending it altogether in 2024, while the stock sank deeper and billions of dollars in market value vanished.

But in 2026, the narrative surrounding Intel has changed dramatically. Over the past year, Intel shares have delivered a stunning triple-digit rally as the company rolled out aggressive cost-cutting measures, broad restructuring plans, leadership changes, and an ambitious expansion of its foundry business, all of which helped revive investor confidence. The comeback story gained even more momentum after the U.S. government acquired nearly a 10% stake in Intel last year, reinforcing the company’s strategic importance to the global semiconductor supply chain and strengthening its position as a critical national technology asset.

Still, Intel’s recovery story is far from complete. Even as the company rebuilds credibility on Wall Street, it continues losing ground in one of the semiconductor industry’s most important growth markets: server central processing units (CPUs). According to analysts at UBS, Intel’s server CPU market share fell sharply to 54.9% in the first quarter of 2026 from 64.4% a year earlier, as AMD and Arm Holdings (ARM) aggressively expanded their presence amid surging AI infrastructure demand. The latest data highlights the complicated reality facing Intel investors.

While the company’s broader turnaround efforts are clearly gaining traction, rivals continue making significant inroads into the very markets expected to drive the next wave of AI growth. So, with Intel fighting to reclaim its footing while AMD and Arm continue capturing server CPU share, where does Intel stock go from here?

About Intel Stock

Founded in 1968 and based in Santa Clara, Intel has spent decades cementing itself as one of the most important players in the global semiconductor industry. While the company built its reputation on the processors powering millions of PCs and enterprise systems around the world, Intel has steadily expanded far beyond its traditional computing roots.

Today, the chipmaker operates across several high-growth areas, including client computing, AI and data center chips, networking and edge infrastructure, as well as Intel Foundry Services (IFS), its fast-growing semiconductor manufacturing division aimed at competing directly with the world’s top contract chipmakers. As AI and advanced computing reshape the technology landscape, Intel is aggressively reinventing itself as both a next-generation chip designer and a global manufacturing powerhouse.

What was once viewed as one of the market’s biggest underperformers has rapidly turned into one of Wall Street’s most surprising recovery stories. Renewed optimism surrounding Intel’s AI strategy, manufacturing roadmap, and broader turnaround initiatives has sparked a dramatic shift in investor sentiment, helping the company regain momentum after years of setbacks.

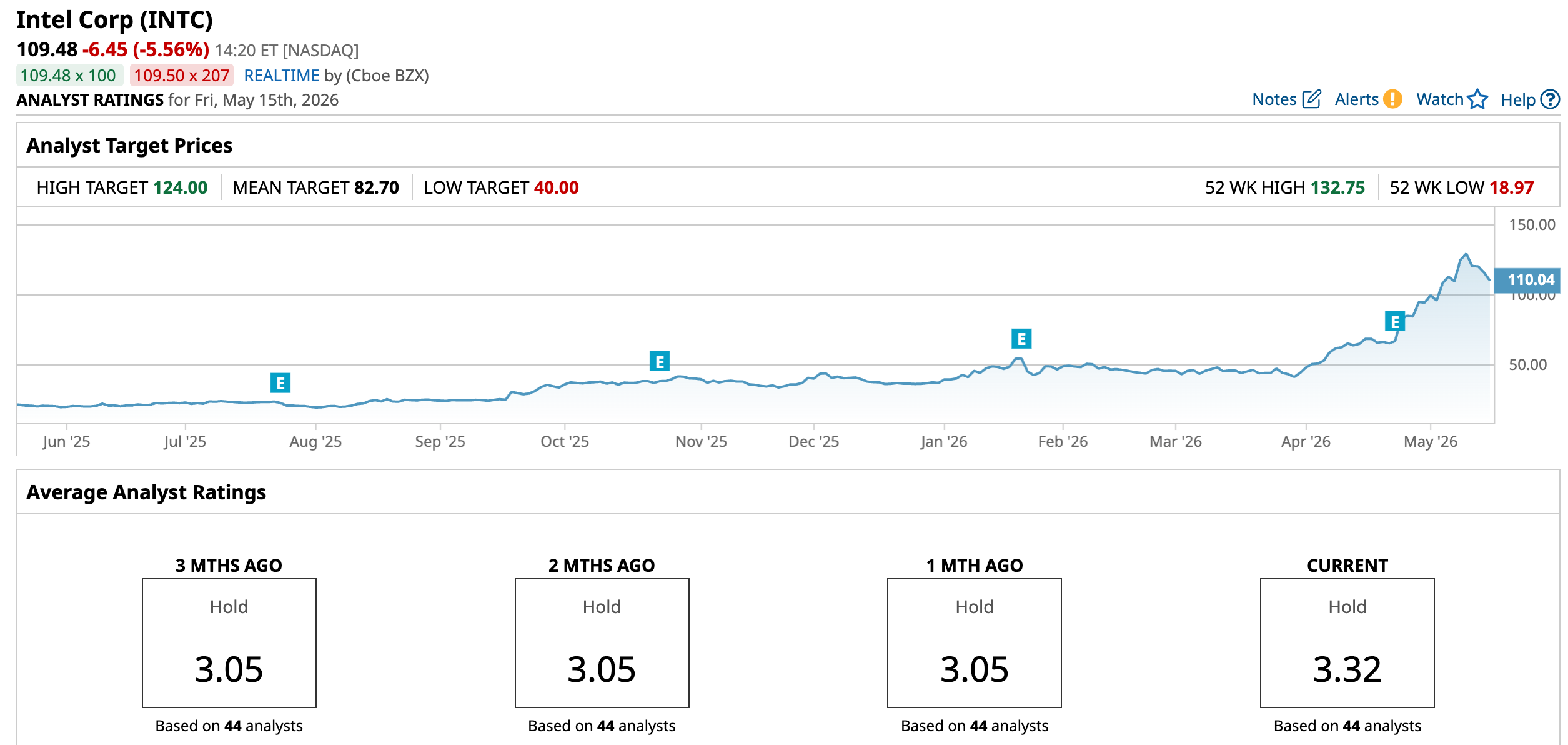

That renewed confidence has translated into a stunning stock market rally. Intel now commands a market capitalization of $582.67 billion, with shares skyrocketing an eye-catching 408.24% over the past year, massively outperforming the broader S&P 500 Index ($SPX), which gained 25.89% during the same period.

The momentum has only accelerated in 2026, with Intel stock surging 196.82% year-to-date (YTD), far ahead of the broader market’s modest 8.81% return. The rally recently pushed Intel shares to a fresh 52-week high of $132.75 on May 11. Although the stock has since slipped about 21%, as investors appear to be digesting growing concerns from UBS about Intel’s weakening server CPU market share and rising competitive pressure from rivals benefiting from the AI infrastructure boom.

A Look Inside Intel’s Q1 Performance

Intel’s improving financial results are giving investors more reason to believe the company’s turnaround story is becoming real. On April 23, the chipmaker released a much stronger-than-expected fiscal 2026 first-quarter earnings report, beating Wall Street estimates across nearly every key metric and triggering a powerful 23.6% surge in the stock during the following trading session. Revenue, gross margin, and earnings per share all exceeded the upper end of management’s own guidance range, marking the sixth straight quarter in which Intel outperformed its internal forecasts.

For the quarter, Intel posted non-GAAP revenue of $13.58 billion, representing 7% year-over-year (YOY) growth and coming in well above analysts’ consensus estimate of $12.39 billion. However, the biggest surprise came from profitability. The company delivered non-GAAP earnings of $0.29 per share, dramatically ahead of Wall Street expectations for just $0.01 per share. The strong earnings performance was fueled largely by aggressive cost-reduction initiatives and a richer mix of higher-margin products.

Still, Intel’s recovery remains far from complete. Despite the strong adjusted results, the company reported a GAAP net loss of $3.7 billion, driven mainly by one-time goodwill impairment charges and ongoing restructuring-related expenses. Even so, several parts of the business showed meaningful signs of improvement, particularly Intel’s data center operations, where the company is beginning to benefit from rising AI-related demand for central processing units. Revenue in the segment climbed 22% YOY to $5.1 billion.

Intel’s Client Computing Group (CCG), home to its PC processor business, generated $7.7 billion in revenue during the quarter, reflecting a modest 1% increase compared to the prior year. Meanwhile, the company’s foundry ambitions continued gaining traction. Revenue from Intel Foundry rose 16% YOY to $5.4 billion, signaling growing interest in Intel’s semiconductor manufacturing capabilities from both internal and external customers.

Also, the foundry division showed incremental operational improvement. Operating losses in the segment narrowed slightly to $2.4 billion, improving by $72 million sequentially as stronger production yields across Intel 4, Intel 3, and Intel 18A technologies helped lift gross margins. However, some of those gains were offset by higher operating expenses tied to increased investments in Intel 14A, which the company is using to support ongoing evaluations from internal teams as well as prospective outside customers.

Looking ahead, Intel struck a notably confident tone for the second quarter. The company guided for revenue between $13.8 billion and $14.8 billion, comfortably ahead of previous Wall Street expectations. And, Intel forecast a non-GAAP gross margin of roughly 39% as it continues navigating the expensive buildout of its manufacturing footprint while ramping production of next-generation AI-focused and consumer-oriented chips.

What Do Analysts Think About Intel Stock?

On May 14, shares of Intel came under pressure, declining about 3.6% after analysts at UBS warned that the company continues to lose market share in the highly competitive server processor market as rivals gain momentum from the ongoing AI infrastructure boom. Analysts led by Timothy Arcuri noted that total server CPU shipments climbed roughly 6% quarter-over-quarter and 19% YOY during the first quarter of 2026, significantly outperforming typical seasonal trends as hyperscalers sharply increased spending on AI-related infrastructure.

Yet despite the strong industry growth, Intel captured little of the upside. UBS said Intel’s server CPU market share fell by approximately 370 basis points sequentially to 54.9%, a steep decline from 64.4% a year earlier. At the same time, AMD continued expanding its foothold in the market, with its share rising to 27.4% from 24.1%, while Arm Holdings saw its market share jump sharply to 17.7% from 11.5%.

The pressure was equally visible on a revenue basis within the x86 server CPU market. Intel’s share declined another 490 basis points to 53.8%, while AMD strengthened its position further by climbing to 46.2%. UBS also pointed out that Intel’s server unit shipments declined 1% sequentially during the quarter, compared to a strong 15% increase for AMD. The latest report highlights one of the biggest obstacles still facing Intel’s broader turnaround story.

Although the company has made progress in stabilizing its operations through restructuring efforts, aggressive cost reductions, and the expansion of its foundry business, rivals continue gaining traction in the fast-growing AI data center market. UBS believes Arm-based processors are benefiting from rising hyperscaler adoption due to their power-efficient architecture, while AMD’s industry-leading core counts and multithreading capabilities are making its chips increasingly attractive for complex agentic AI workloads.

Still, UBS believes Intel could become more competitive over time with the launch of its upcoming Coral Rapids server platform. The firm noted that Intel may benefit in the long term as more AI workloads begin running locally on personal computers, potentially boosting demand for the company’s client processors.

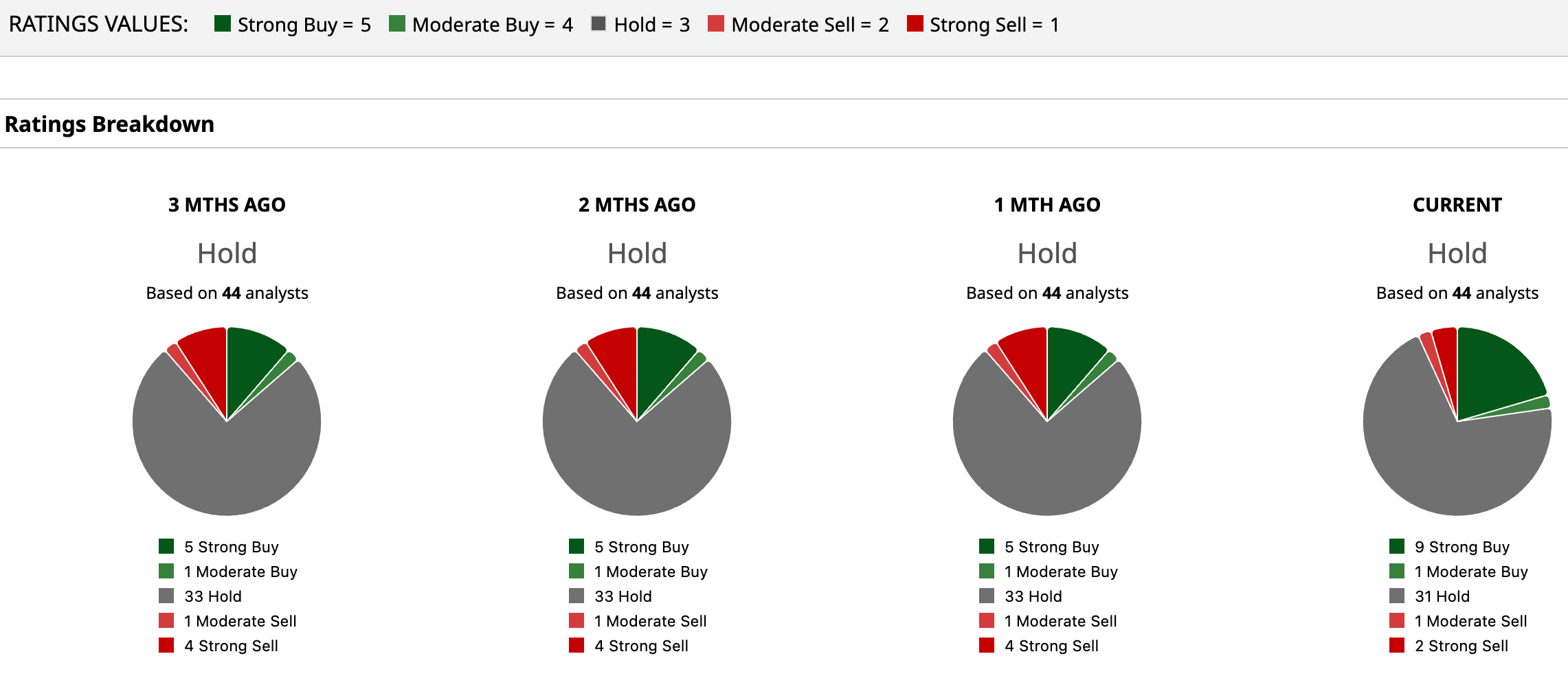

Despite Intel’s stunning turnaround and explosive stock rally, Wall Street still appears cautious about the company’s long-term recovery story. The stock currently carries a consensus “Hold” rating, reflecting growing confidence in Intel’s progress but lingering concerns about whether the momentum can be sustained. Among the 44 analysts covering the company, nine rate the stock a “Strong Buy” and one assigns a “Moderate Buy” rating.

However, the majority of 31 analysts remain neutral with “Hold” recommendations, while one analyst rates the stock “Moderate Sell” and two maintain “Strong Sell” ratings. Notably, Intel shares have already surged far beyond the average analyst price target of $82.70, while the Street-high target of $124 suggests the stock could still gain roughly 13.3% from current levels.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)

/Space/Rocket%20lift%20off%20by%20Alones%20via%20Shutterstock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)