/AI%20(artificial%20intelligence)/AI%20microchip%20by%20DesignKingBD360%20via%20Shutterstock.jpg)

The artificial intelligence (AI) boom is transforming the tech industry, but it has also given birth to a major challenge. Advanced AI chips consume enormous amount of power and generate intense heat. Companies that provide the infrastructure needed to power and cool these systems efficiently are the saviors now. One such player is Vertiv Holdings (VRT), which makes the power and cooling systems that keep AI data centers running. As AI models become larger and more power-intensive, demand for these systems is exploding, which is why Vertiv stock has soared 130% so far this year, touching new highs of $377.77.

Here’s why Vertiv could eventually be the biggest winner in the next wave of AI.

AI’s Next Bottleneck Is Electricity, Not Chips

Manufacturing advanced chips for AI models is no longer the limiting factor in AI development. But, making sure these advanced AI models and giant data centers run smoothly without overheating is becoming increasingly important. The U.S. Energy Information Administration recently projected that U.S. electricity consumption will hit record highs in 2026 and 2027, with AI-driven data centers becoming one of the biggest contributors to rising demand.

This is why Vertiv is a critically important player. It manufactures products such as liquid cooling systems, backup power equipment, thermal management technology, and electrical infrastructure used inside massive AI server facilities. The demand for Vertiv’s products is evident from the massive growth in its earnings from $1.19 per share in 2023 to a projected $6.40 in 2026. This implies that Vertiv’s earnings have increased at a compounded annual growth rate of 75% over the last three years.

In the first quarter, net sales came in $2.65 billion, up 30% year-over-year, while organic revenue growth came in at 23%. Adjusted diluted EPS reached $1.17, up 83% year-over-year. During the Q1 earnings call, management stated that Vertiv’s “competitive advantages are compounding” as AI customers increasingly rely on providers that can deliver entire systems instead of individual products. The company is pushing to become a complete AI infrastructure solutions provider rather than simply a hardware supplier. It is offering integrated power, thermal, cooling, infrastructure, and services solutions for hyperscale AI deployments. To support this goal, it recently announced the acquisition of ThermoKey, which expands the company’s heat exchange and dry cooler capabilities. Additionally, the acquisition of BMarko Structures will push its ability to provide “manufactured and converged infrastructure solutions at scale.”

Cash generation also remained extremely strong in the quarter, with adjusted free cash flow up 147% YoY to $653 million. Vertiv ended the quarter with net leverage of just 0.2x, giving the company enormous financial flexibility to continue investing aggressively in AI infrastructure growth. The company is rapidly expanding its liquid cooling and fluid management capabilities, two areas that are becoming increasingly critical for AI data centers. Vertiv expects more growth in 2026, with earnings growth of 50% and revenue growth of 30%.

For the full year, analysts project Vertiv’s revenue to increase by 36% to $13.9 billion, accompanies by earnings growth of 55%. Additionally, revenue is expected to increase by 27% to $17.7 billion and earnings by 35% in 2027.

Why Vertiv Could Be a Long-Term AI Winner

While investors are concerned that increased AI infrastructure spending is putting pressure on AI companies' profit margins, Vertiv is benefiting from this high spending. Companies including Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOGL) (GOOG), and Meta Platforms (META) are investing billions of dollars in next-generation AI data centers. The more data centers these tech titans build, the higher the demand for Vertiv’s products and its profits could rise.

Trading at roughly 42x forward 2027 earnings, Vertiv stock is no longer cheap after its AI-driven rally. But investors might still be underestimating how large the AI infrastructure opportunity could become, and that Vertiv could be a clear winner over the next decade.

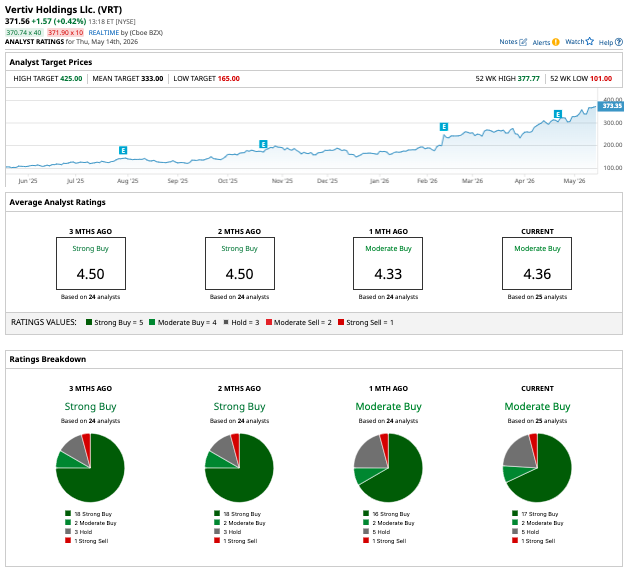

On Wall Street, Vertiv stock is an overall “Moderate Buy.” Of the 25 analysts covering the stock, 17 rate it as a "Strong Buy," two call it a "Moderate Buy," five recommend a “Hold,” and one has a “Strong Sell” rating. It has crossed its average price target of $333. However, its high price estimate of $425 indicates a possible 14% rally over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)