/C_H_%20Robinson%20Worldwide%2C%20Inc_%20website%20magnified-by%20Casimiro%20PT%20via%20Shutterstock.jpg)

With a market cap of $19.3 billion, C.H. Robinson Worldwide, Inc. (CHRW) is one of the world’s largest third-party logistics (3PL) providers, specializing in freight transportation, supply chain management, and logistics technology services. Founded in 1905 and headquartered in Eden Prairie, Minnesota, the company connects shippers with carriers across truckload, less-than-truckload (LTL), ocean, air, rail, and intermodal transportation networks.

Shares of CHRW have significantly outperformed the broader market over the past 52 weeks. CHRW stock has jumped 65.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 25.2%. However, shares of the company are up 1.8% on a YTD basis, trailing SPX’s 8.2% rise.

Focusing more closely, shares of the trucking company have outpaced the Industrial Select Sector SPDR Fund’s (XLI) 20.6% return over the past 52 weeks.

On May 4, shares of C.H. Robinson Worldwide fell 8.9% after Amazon.com, Inc. (AMZN) announced it was expanding its supply chain and logistics network to businesses outside its marketplace. Investors viewed the move as a major competitive threat, as Amazon’s transportation, fulfillment, and delivery capabilities could directly challenge established freight and logistics companies like C.H. Robinson.

For the fiscal year, ending in December 2026, analysts expect C.H. Robinson’s adjusted EPS to grow 19.7% year over year to $6.09. The company's earnings surprise history is promising. It topped the consensus estimates in the last four quarters.

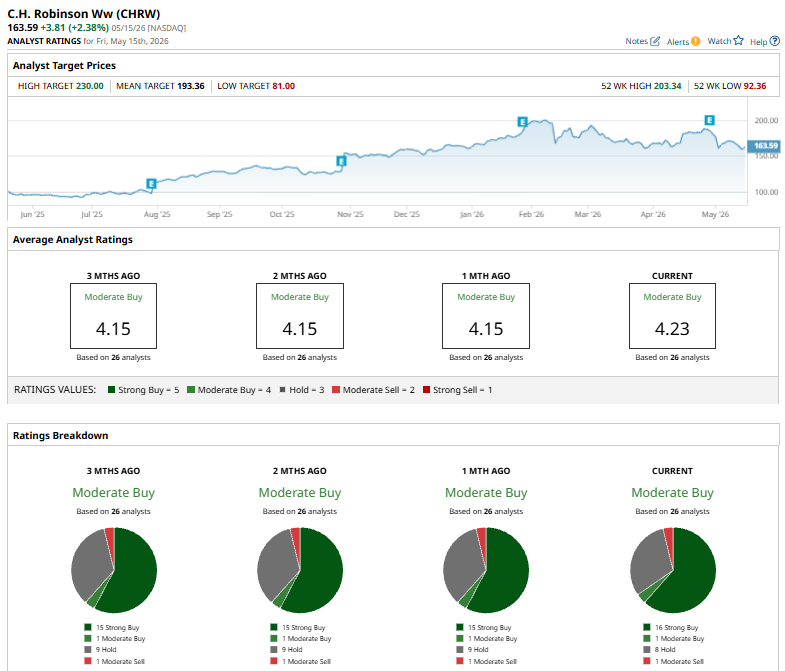

Among the 26 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 16 “Strong Buy” ratings, one “Moderate Buy,” eight “Holds,” and one “Moderate Sell.”

This consensus is bullish than a month ago, when the stock had 15 “Strong Buy” suggestions.

On May 15, Citi analyst Ariel Rosa upgraded C.H. Robinson Worldwide to “Buy” from “Neutral” while maintaining a $199 price target. The analyst noted that the stock had previously lagged peers due to concerns over margin pressure from rising truckload spot rates. However, stronger-than-expected first-quarter results and improving margins boosted confidence in the company’s outlook.

The mean price target of $193.36 implies a premium of 18.2% from the current market prices. The Street-high price target of $230 suggests a 40.6% potential upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Alibaba%20by%20testing%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)