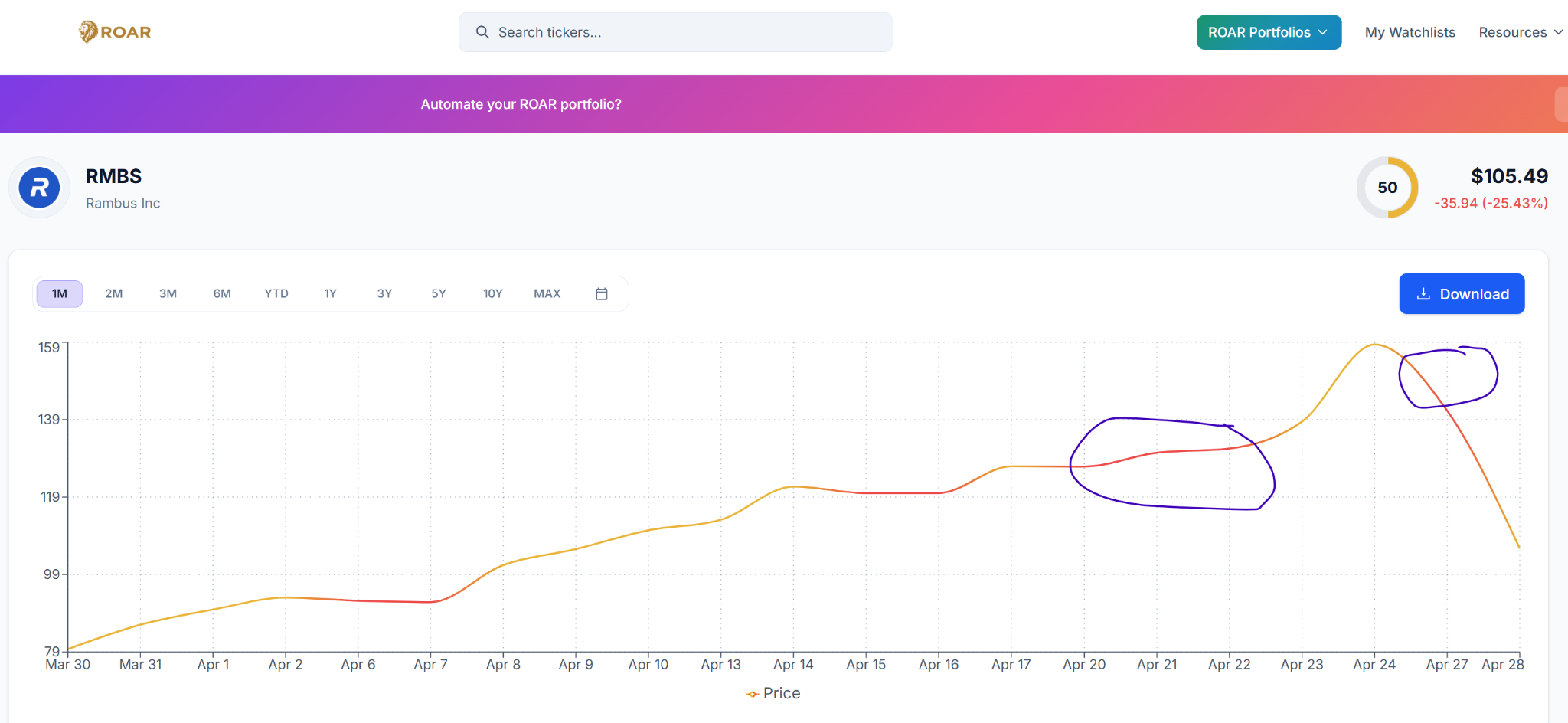

Rambus (RMBS) stock, as some veteran investors will recall, essentially retired during the dot-com bubble. The business kept going, but the stock, as you can see from this monthly price chart going back 30 years (left side, purple markings), went from obscure tech stock to a $120 titan.

Less than two years later, the stock changed hands for $4 a share. And yet, to the company’s credit, as the chart shows, it made it all the way back, and more, hitting an all-time high of about $160 on April 24. Yet RMBS traded for just $40 about 12 months ago.

But the volatility continues: RMBS stock lost one-fifth of its value in a single trading session, just a few days after setting new record highs.

What happened? And is this an isolated incident, or the “cockroach theory” (there’s never just one)?

RMBS has long been a favorite of the semiconductor pure-play crowd. In English, it is like a high-margin toll booth for memory. And “memory” of what happened to high-flying tech 25 years ago, is at the front of my mind. Not because Rambus’ Q1 2026 earnings report dropped the stock that much. But because I’ve seen this before, and I’m not so sure this is an isolated incident. Because once the market gets it in its mind that there’s a fire somewhere, the exit doors can’t handle the crowd running out.

RMBS stock might just be a violent warning sign for the entire technology sector. Because tech stocks have been getting by based on the idea that “good enough” can lift stock prices as I can only relate to one other period in my 40-year career: 1999-2000. Look up how that ended, or use the RMBS chart above to get an idea.

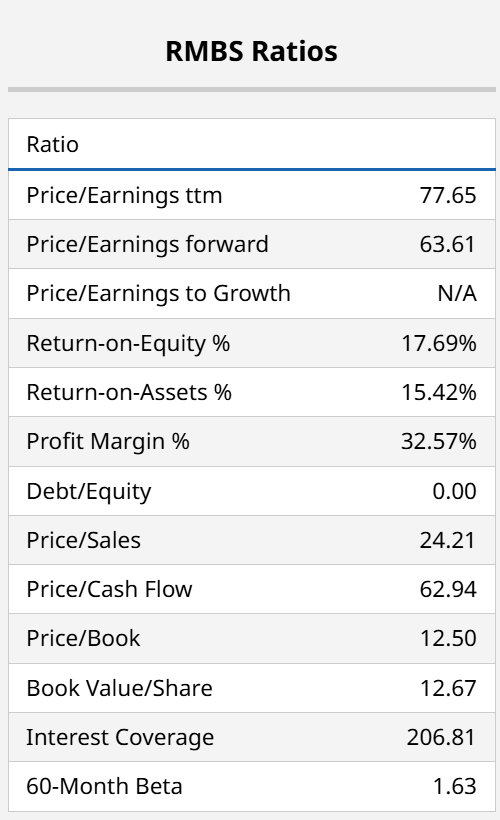

Rambus actually reported a modest beat on both the top and bottom lines ($0.63 EPS vs. $0.62 expected). In a normal year, that’s a win. But this isn’t a normal year as the stock was trading at 63x forward earnings. At some point in every market cycle, there comes a reckoning point. Maybe this is the start of it. That’s impossible to predict, but easy to plan for. And that’s my point.

Despite the EPS beat, certain revenue segments fell short of the whisper numbers. The market reacted to a $180 million print against a $190 million expectation, signaling that the insatiable demand for AI memory chips might be hitting a plateau.

Or that investors have projected too far forward. Which is what happens in every market cycle. Which is why “rammed by a bus” is my chosen summary of what just happened. The stock closed north of $140 one day, and trades near $105 the next. Will a stop order prevent that? NO. Will solid risk management, part of a broader portfolio plan, prevent that? It can.

RMBS is a proxy for the $650 billion AI capex bill that the industry is expected to foot in 2026. The stock’s crash highlights a growing fear: What if the hardware is being overbuilt?

For dip-buyers, this is a tough one to move on. That percentage price oscillator (PPO) indicator at bottom looks like the proverbial falling knife.

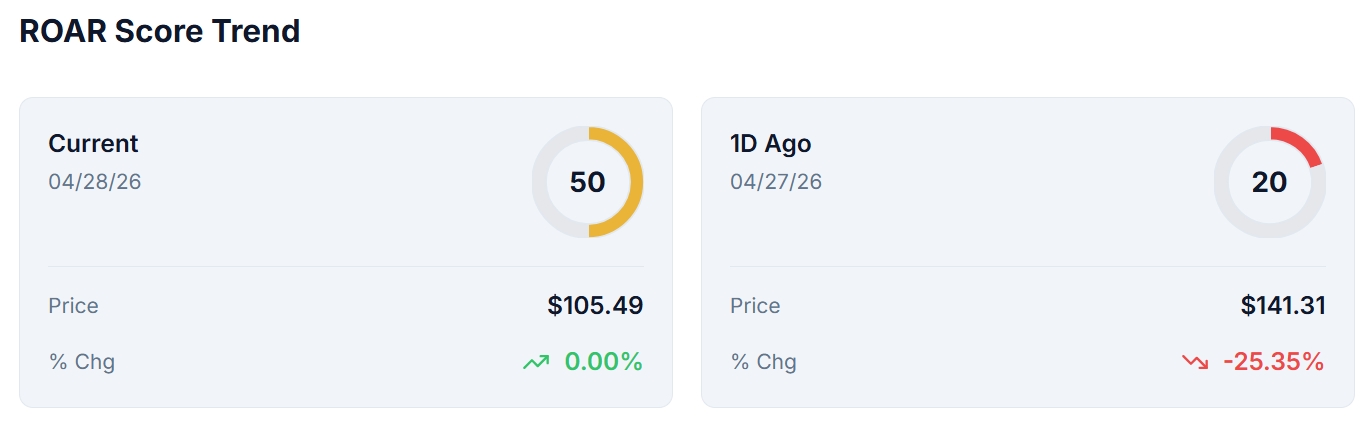

The ROAR Score expresses exactly what I’d hope it would. It is produced automatically each night for thousands of stocks and ETFs, based on my 40-plus years of pattern recognition experience and technical analysis.

RMBS was clearly signalling “too far, too fast” by flipping between the red (higher risk) zone and the yellow (neutral risk zone), with red starting to take over more recently. This is a time where I am looking much more for reasons not to chase stocks, as opposed to reasons to convince myself I’m missing out (FOMO). That’s why this analysis is a nice additional factor to consider.

While companies are buying the chips and the memory controllers, the end-user monetization of AI tools (like Copilot and Gemini) is still in the experimentation phase. If the big cloud spenders (Microsoft (MSFT), Amazon (AMZN), Google (GOOGL)) don’t show a clear profit path for this equipment, the “first movers” like Rambus are the first to be jettisoned.

I’m all about price. It tells the truth, and it is what we can spend. And this is an ideal time to note the following:

RMBS now trades around where it did in September 2025. And, where it did in March 2020. Get it?

As tech giants prioritize their own custom silicon (like Google’s TPUs or Amazon’s Trainium), third-party IP providers like Rambus face a shrinking available market for their highest-margin products. That means one possibility is a return to the “Mag-7 or bust” market. That’s where SPY (SPY) and QQQ (QQQ) do OK, but the average stock underneath doesn’t. That is what the past several years have been like.

The warning from RMBS’s stock price performance is clear: the 45% AI concentration in the S&P 500 Index ($SPX) has created a market that is hyper-sensitive to any sign of infrastructure fatigue. If the memory industry is starting to wobble, it suggests that the massive hardware supercycle of 2024-2025 is entering its hangover phase. Let’s see what the rest of the earnings season brings.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)