Global markets are once again on edge as rising tensions of the war between the United States and Iran threaten one of the world’s most critical oil supply routes. With disruptions around the Strait of Hormuz pushing energy prices higher, fears of a prolonged shock are creeping in. Add to that a stagflation-like backdrop – sticky inflation, slowing growth, and a softening job market – and the mood across Wall Street is clearly cautious. Even high-flying tech stocks are feeling the pressure as rising costs and tighter financial conditions weigh on future growth bets.

According to investment firm Schroders, history offers a clear pattern; during past oil shocks, defensive and commodity-linked sectors have often outperformed, delivering steady gains while broader markets struggled. Sectors like consumer staples, in particular, tend to hold firm thanks to their essential, everyday demand. In contrast, growth-heavy sectors like tech are often under pressure.

That’s exactly why investors are now rotating toward reliable, dividend-paying names in the consumer staples space. Shares of companies like Bunge Global SA (BG) and Coca-Cola Company (KO) could be wise buys not just for their strong fundamentals, but also for their resilience in uncertain times.

So, if investors are looking to shield their portfolio from an oil-driven market shake-up, these top-rated consumer staples players deserve a closer look.

Consumer Staples Stock #1: Bunge Global

Bunge Global has been quietly powering the global food chain for over 200 years, connecting farmers to consumers across more than 50 countries. Headquartered in St. Louis, Missouri, with its registered office in Geneva, Switzerland, Bunge operates at the heart of agriculture by moving grains, processing oilseeds, and producing essential food and feed ingredients.

With a team of around 37,000 employees, the company focuses on making supply chains faster and more efficient while adapting to changing consumer needs. From farm to table, Bunge plays a steady, behind-the-scenes role in keeping the world fed. Its market capitalization currently stands at $24 billion.

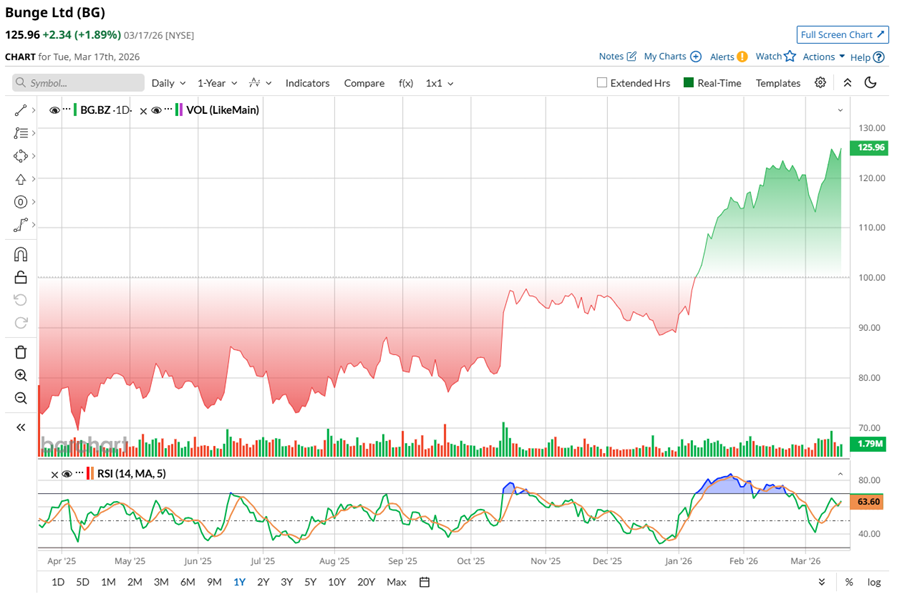

Shares of the agribusiness and food company have been on a strong run, with its stock recently touching a long-term high of $128.46 before easing slightly. Over the past year, shares have surged nearly 62.7%, comfortably outperforming not just the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 2.87% surge, but also the S&P 500 Index’s ($SPX), which gained around 15.8%.

The momentum has only picked up in recent months, rising 54.63% over six months and 33.84% in the last three. Technically, the 14-day RSI near 55.61 suggests strength, though nearing overbought levels.

BG may look a bit expensive at first glance. The stock trades around 15.54 times forward adjusted earnings, slightly above industry averages, leaving limited room for mistakes. Yet, priced at just 0.26 times forward sales, it’s cheaper compared to peers. That contrast suggests investors are willing to pay up for its scale and earnings visibility, even if some caution is already priced in.

Additionally, Bunge strengthens its case through consistent shareholder returns. The company continues its quarterly dividend, recently paying $0.70 per share and extending a 24-year payout streak. Its forward annualized dividend stands at $2.80. With a yield of 2.22% and a modest 37.9% payout ratio, Bunge balances rewarding investors while retaining flexibility, supported by a diversified, scale-driven earnings engine.

Bunge delivered its fourth quarter and fiscal 2025 results on Feb. 4. The agribusiness giant surprised Wall Street with stronger-than-expected numbers, generating net sales of $23.76 billion, representing 75.5% year-over-year (YOY) growth. This is fueled by improved volumes across key segments like soybean and softseed processing, along with grain merchandising.

But beneath the headline growth, the picture had some layers. Adjusted EPS came in at $1.99 per share, down 6.6% annually, as rising costs trimmed the benefit of higher sales. Still, adjusted total EBIT jumped 40% YOY to $622 million, showing the company’s ability to scale efficiently.

A big part of this story is Bunge’s game-changing acquisition of Viterra in July 2025. Now two quarters into integration, the combined entity is already expanding its global footprint and diversifying across major crops, setting the stage for long-term growth. Nevertheless, the balance sheet reflects the cost of expansion. Cash levels declined, while long-term debt nearly doubled to $8.8 billion. Even so, Bunge remains focused on bringing the two businesses together smoothly and making its global network stronger and more efficient.

Looking ahead, management stays cautiously optimistic, guiding for 2026 earnings between $7.50 and $8.00 per share, signaling steady growth despite an uncertain global backdrop.

Meanwhile, analysts monitoring the company anticipate EPS for the year to be $8.10, up 7% YOY before rising by another 33.5% annually to $10.81 in fiscal 2027.

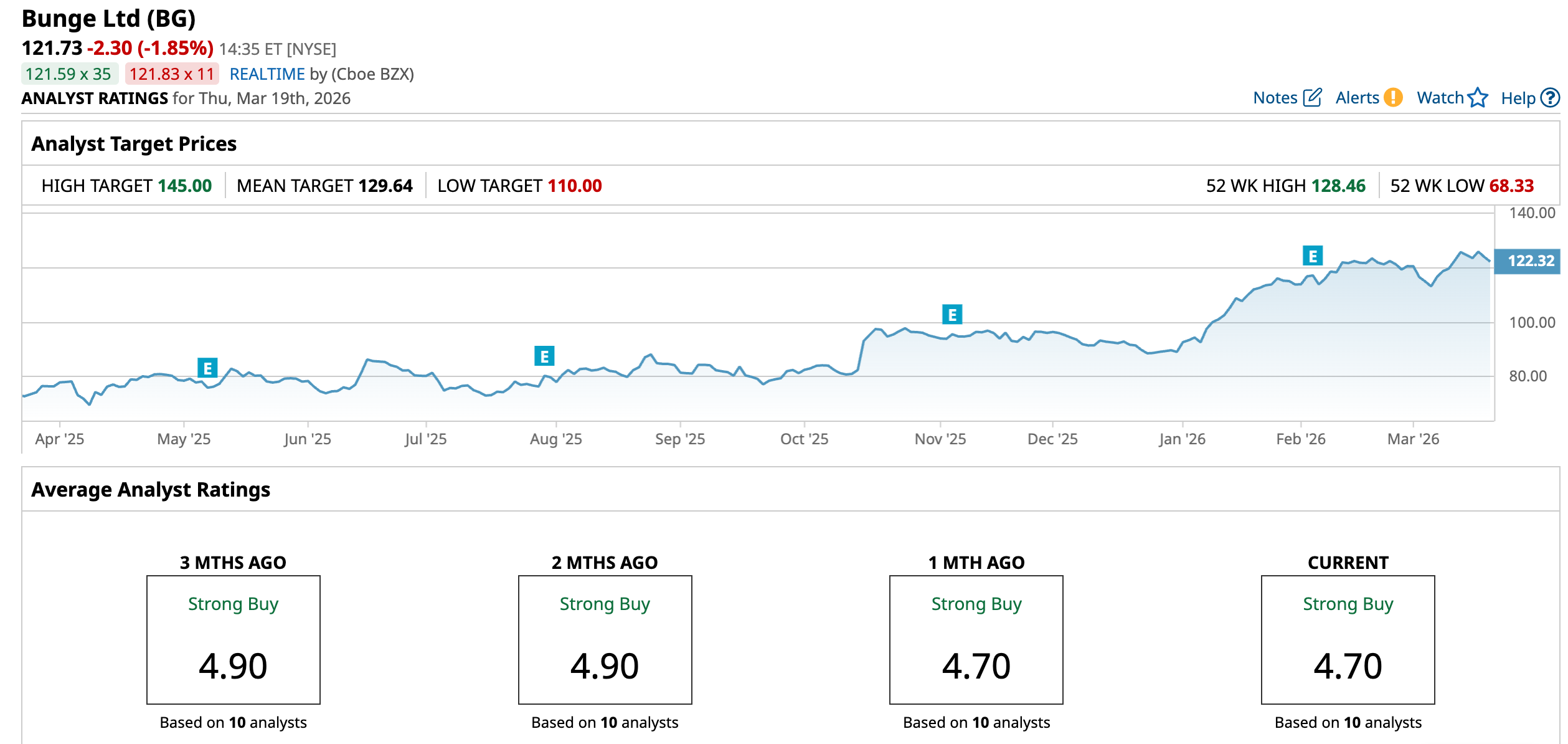

Wall Street’s confidence in Bunge comes down to consistency, earning the stock an overall consensus “Strong Buy” rating. Of the 10 analysts tracking the stock, eight back it with a “Strong Buy,” one has a “Moderate Buy,” and the remaining one sits on the sidelines with a “Hold" rating.

BG’s average target of $129.64 suggests an upside potential of 6.5% from the current price levels. The Street’s highest $145 price target hints the stock could rally as much as 19.1%.

Consumer Staples Stock #2: Coca-Cola

The Coca-Cola Company, founded in 1886 and headquartered in Atlanta, Georgia, is one of those brands that’s almost everywhere you look. From its iconic soft drinks to juices, coffee, tea, and energy drinks, Coca-Cola has built a massive global presence, serving around 2.2 billion drinks every single day across more than 200 countries.

It is not just about scale, though – it is about consistency and brand power. With a market cap of $326.99 billion, Coca-Cola has mastered the art of staying relevant, refreshing generations while steadily delivering value to investors over time.

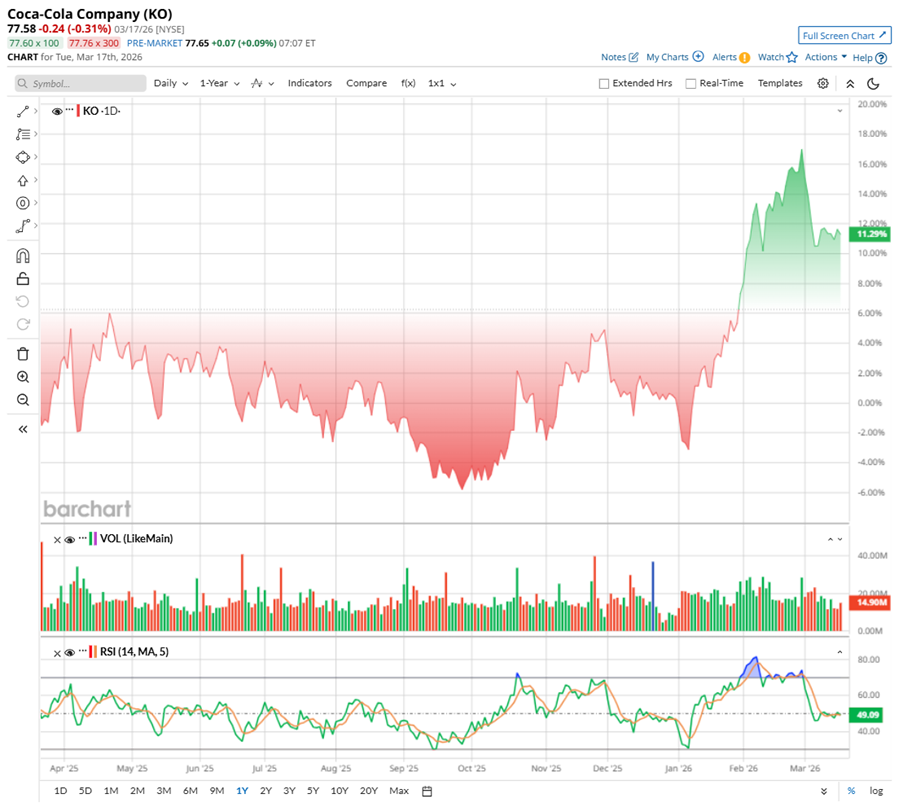

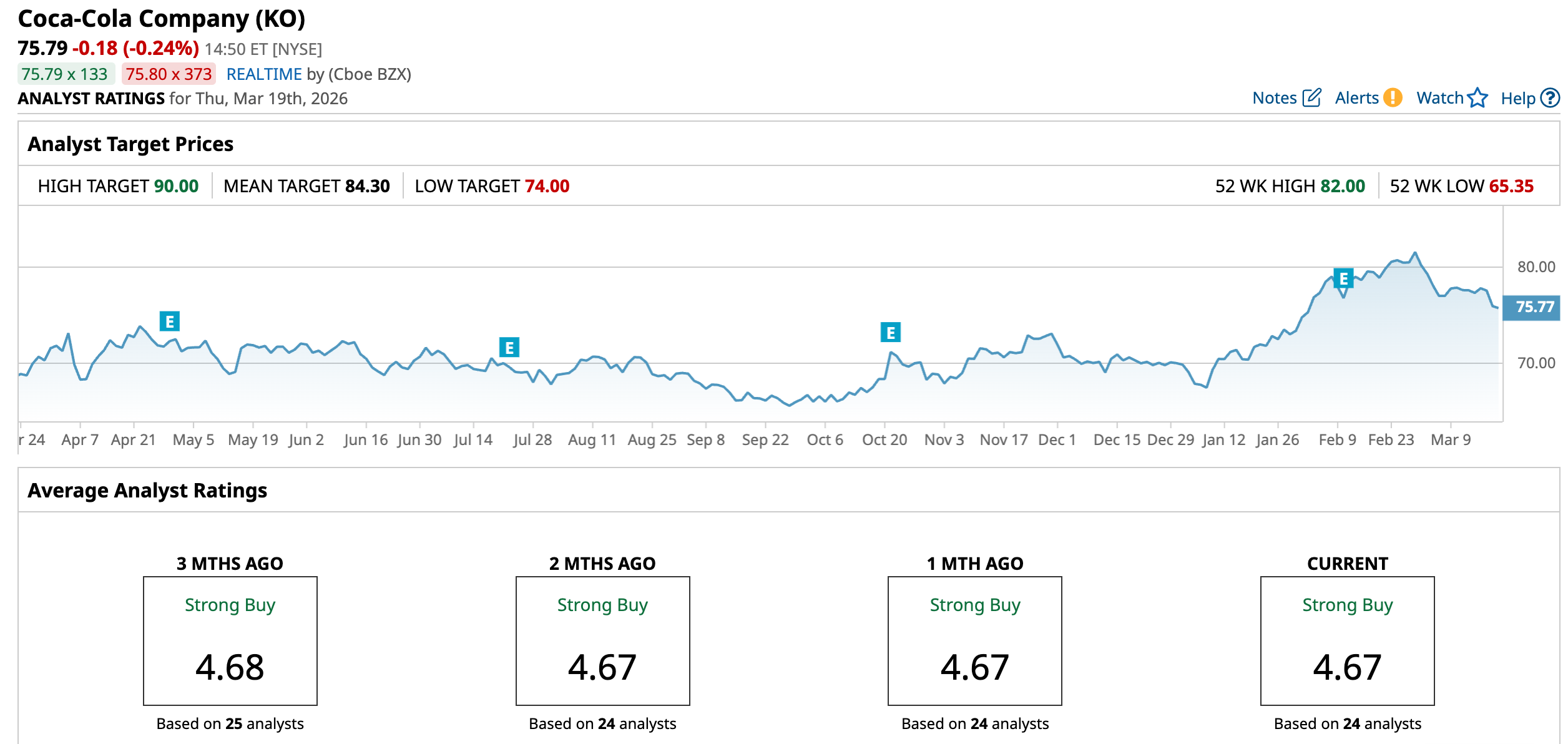

The beverage giant’s steady business strength is clearly reflected on the charts as well. KO stock has gained over 9.49% over the past 52 weeks, with 14.19% surge over just the last six months. Also, 2026 has started on a strong note, with shares rising 8.5% year-to-date (YTD), printing fresh highs 22 times this year, and even touching a high of $82 in February.

Recently, the pace has cooled, with the 14-day RSI easing from overbought levels to around 39.51 times, suggesting a more balanced setup after the strong run.

Valuation-wise, KO stock is trading at a premium, and that’s part of its appeal. The stock is priced at around 24.02 times forward adjusted earnings and 6.67 times forward sales, sitting above sector peers and its own historical averages. But investors are not just paying for growth, but paying for consistency and brand strength.

That premium starts to make sense when you look at its dividend story. The beverage giant has long been a favorite for income-focused investors, largely due to its dividend story. The company currently offers a forward annualized dividend of $2.12 per share, giving a forward yield of around 2.73%. This represents a steady stream of income in uncertain markets.

What really stands out, though, is its consistency. Coca-Cola has increased its dividend for 64 consecutive years, earning it the elite “Dividend King” status. With a payout ratio near 68%, the company balances rewarding shareholders while still keeping enough room to reinvest and grow.

Coca-Cola released its full-year and Q4 2025 earnings report before the market opened on Feb. 10, closing out the year with a steady, if slightly mixed, performance. And this is very much in line with its reputation as a resilient consumer giant. In Q4, the company’s non-GAAP EPS grew 6% YOY to $0.58, edging past expectations by a small margin, even as revenue came in just shy of forecasts. Still, sales grew 2.2% YOY to $11.8 billion, showing that demand remains intact.

Looking a little deeper, the core business tells a stronger story. Organic revenue rose 5%, driven by growth in pricing and concentrate sales. Unit case volumes inched up 1%, though foreign exchange remained a drag. Coca-Cola has been navigating this for a while now.

At the same time, the company continued to invest in its future, spending $2.1 billion on capital projects in 2025. And true to form, it kept rewarding shareholders, returning $8.8 billion through dividends while continuing share repurchases.

Further still, management highlighted that in the past 50 years, Coca-Cola’s annual volume has dipped just once – during the pandemic – underscoring the strength of its global demand. Looking ahead, the management estimates organic revenue growth of 4% to 5% in fiscal 2026, along with non-GAAP EPS growth between 7% and 8% and strong cash flows. In a volatile world, Coca-Cola continues to do what it does best: deliver steady, reliable growth.

Meanwhile, analysts expect Coca-Cola’s non-GAAP EPS to rise 7.67% YOY to $3.23 in fiscal 2026 and then surge by another 7.74% annually to $3.48 in the next fiscal year.

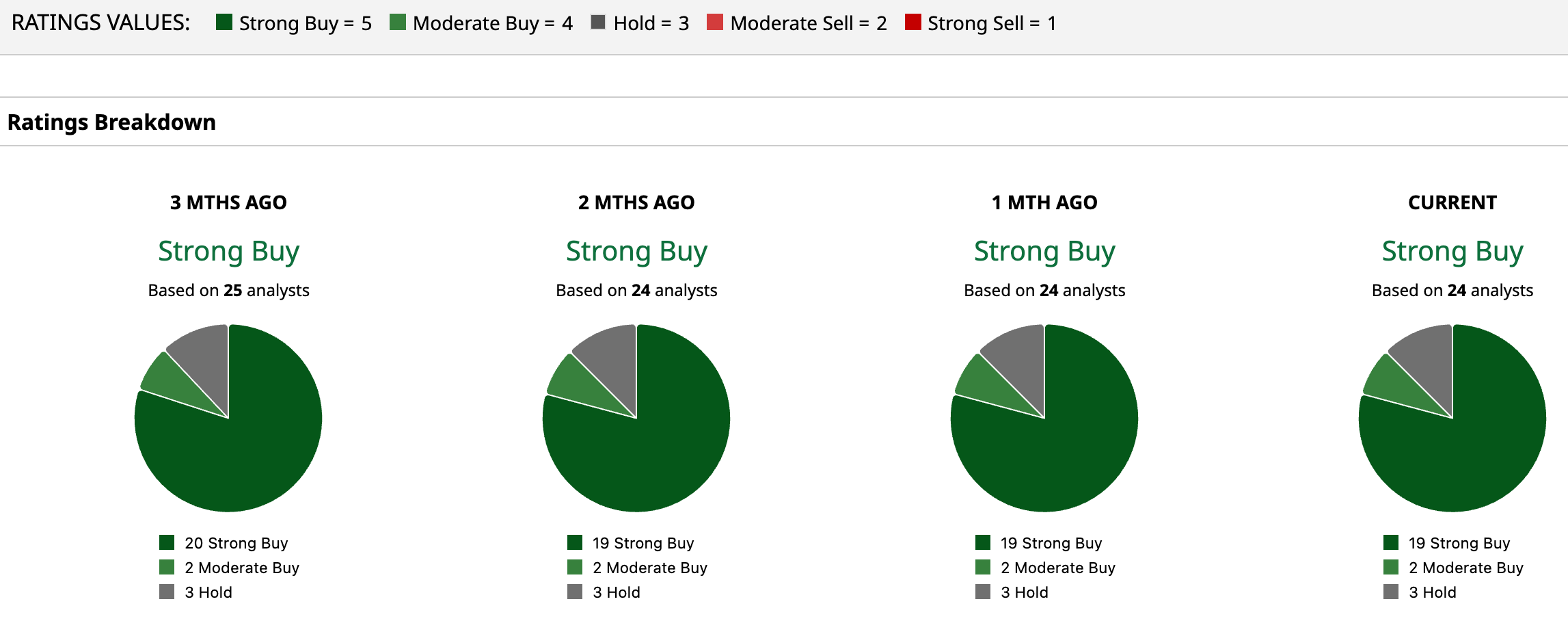

Overall, analysts are bullish about KO’s growth prospects, giving the stock a consensus rating of “Strong Buy.” Of the 24 analysts covering the stock, 19 advise a “Strong Buy,” while two suggest “Moderate Buy,” and the remaining three advise a “Hold.”

The average analyst price target for KO is $84.30, indicating potential upside of 11.23%. The Street-high target price of $90 suggests that the stock could rally as much as 18.75% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)