/Meta%20by%20creativeneko%20via%20Shutterstock.jpg)

Meta Platforms (META) is moving another step closer to building its AI future on its own technology. According to a recent Reuters report, the company plans to begin production of its custom AI chip named “Iris” beginning in September. The chip is expected to support Meta’s growing AI ambitions as it reportedly aims to double its computing capacity from seven gigawatts this year to 14 gigawatts next year. The company has partnered with Broadcom (AVGO) for its chip design, while Taiwan Semiconductor (TSM) is set to manufacture it. Despite the optimistic goals, the stock fell 3.5% in premarket trading. The decline came after Meta revealed it could spend as much as $145 billion on AI infrastructure this year to double its computing power. One reason for the negative reaction could be the confusion among market participants regarding the company's ambitions. Many have been left confused by the company's decision to sell access capacity while at the same time continuing to increase the same capacity.

The new chip is part of Meta’s in-house Meta Training and Inference Accelerator (MTIA) project. The company launched these MTIA chips in 2023 to gradually rely less on outside suppliers such as Nvidia (NVDA) and Advanced Micro Devices (AMD). The chip’s internal testing took roughly six weeks and did not reveal any major issues. At the same time, Meta has also been strengthening the rest of its AI supply chain, among other initiatives. The company has signed long-term agreements with Samsung for memory chips, Sandisk (SNDK) for flash storage, and Sumitomo Electric for fibre optic components.

About Meta Stock

Meta is a global technology company that operates across social media, artificial intelligence, and digital advertising across its platforms which include Facebook, Instagram, WhatsApp, Threads, and Messenger. Founded in 2004, the company is headquartered in Menlo Park, California and is led by co-founder and CEO Mark Zuckerberg.

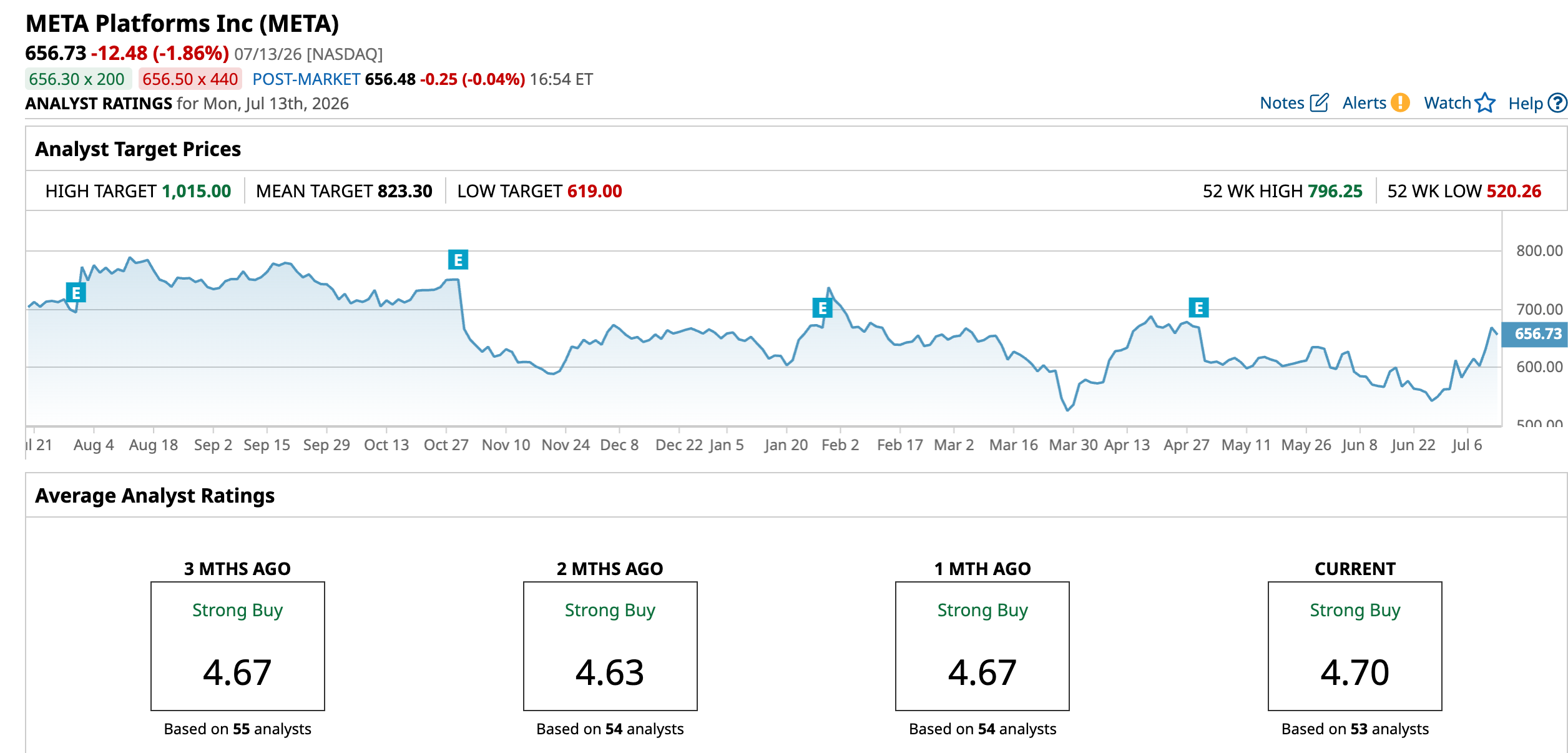

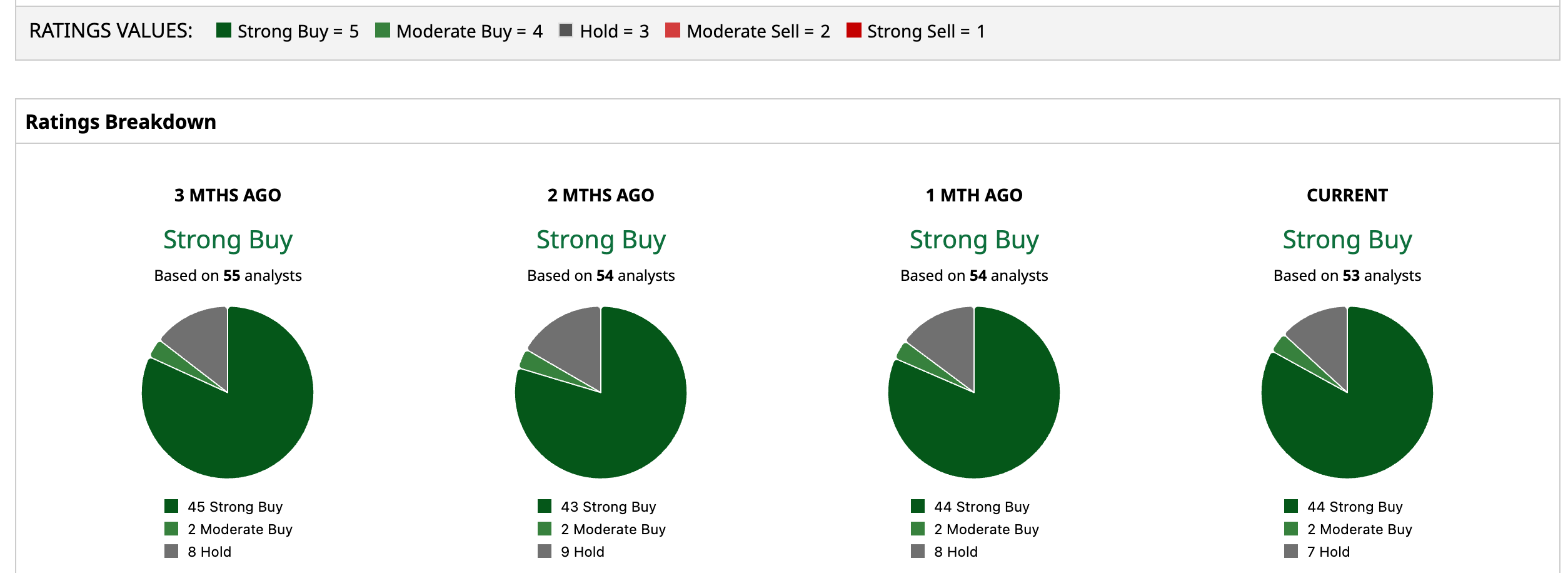

Year-to-date (YTD), Meta’s stock is down marginally, notably underperforming the S&P 500 Index’s ($SPX) 9.8% gain during the same period. The decline is largely driven by investor concern over Meta’s aggressive AI spending. The company raised its capital expenditure guidance for 2026 to as much as $145 billion, almost twice its 2025 expense. Unlike its competitors, Meta lacks a cloud business to offset this spending. However, in the last five days, the stock has recovered 9.47%. The positive shift came after reports that Meta is building a cloud business to monetize its AI data center investments.

Meta’s valuation looks attractive by most measures. The company is trading at a discount to its historical norms despite the business delivering strong revenue growth. The forward GAAP price-to-earnings ratio of 20.34 times sits 9% below the company’s 5-year average of 22.35 times. The forward price-to-sales ratio of 6.72 times is in line with its 5-year average. The EPS growth trajectory should further strengthen investor confidence, with consistent double-digit growth expected from 2026 through 2029. In terms of the capital structure, Meta holds $81.18 billion in cash against $86.77 billion in debt. The resulting net debt of $5.59 billion appears very manageable for a company with a $1.69 trillion market cap. The stock has fallen in 2026 due to concerns of heavy AI spending pressuring near-term free cash flow. Yet, the discounted valuation combined with the steady earnings growth expected suggests the sell-off may have been overdone.

Meta Posts Fastest Revenue Growth Since 2021 Amidst Spending Concerns

Meta reported its first-quarter fiscal 2026 earnings on April 29. The firm beat the analyst consensus on both key metrics. Revenue of $56.31 billion beat the $55.45 billion consensus, marking a 33% growth year-over-year (YOY). This was the fastest growth for Meta since 2021. The adjusted EPS of $7.31 comfortably beat the $6.67 consensus. Advertising remained strong, with ad impressions increasing 19% and the average price per ad increasing 12%. The company’s family of apps' other revenue grew dramatically by 74%, primarily driven by WhatsApp paid revenue and subscriptions. CEO Mark Zuckerberg credited strong momentum across apps and Meta Superintelligence Labs for the milestone quarter.

For the second quarter, the guided revenue is $58 billion to $61 billion, roughly in line with analyst expectations. The company raised its full-year 2026 capital expenditure guidance to a range of $125 billion to $145 billion, up from $115 billion to $135 billion. CFO Susan Li stated that the revised guidance is due to higher component prices and additional data center costs. Addressing the heavy investment concerns, Zuckerberg said Meta has always focused on scale first. The company builds products that reach billions of users, then works on monetizing them later.

What Analysts Are Saying About Meta Stock

Wolfe Research analyst Shweta Khajuria maintained an “Outperform” rating for Meta with a price target of $800. The analyst believes that Meta’s potential cloud offering could increase the EPS by up to 20% for every gigawatt of capacity it monetizes. However, Khajuria expects Meta to further increase its capital spending due to this, estimating capex at $200 billion for 2027. Wells Fargo analyst Ken Gawrelski and Citi analyst Ronald Josey also have a bullish view for Meta, both maintaining a “Buy” rating for the firm.

Based on the 53 Wall Street analysts, Meta holds a “Strong Buy” rating with a mean price target of $823.30, indicating a 25.4% upside. The positive outlook comes after Meta achieved its fastest revenue growth for a quarter since 2021. Despite this, the stock’s recent decline makes it an especially attractive entry point for investors.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)